Paras Anand, chief investment officer, Asia Pacific, discusses how an increasing number of Chinese firms are shifting their focus away from a US listing in favour of domestic stockmarkets. He examines what’s driving this sea change and the implications for both Chinese companies and international investors.

For a generation of Chinese tech entrepreneurs, ringing the opening bell on the Nasdaq or New York Stock Exchange was the ultimate sign of success. From the late 1990s and the dawn of China’s online economy, the country’s most innovative start-ups beat a path to US initial public offerings (IPOs), attracted by richer valuations and a smoother listing process than they could usually find at home.

Nowadays, however, some of China’s leading tech and internet firms are opting to stay closer to home, either by relocating their primary listings away from the US or adding a secondary listing in Hong Kong or Shanghai exchanges.

More to follow

We think more companies are likely to follow in the footsteps of e-commerce giant Alibaba Group, which brought the world’s second-biggest listing of 2019 to Hong Kong when it raised US$13bn in a secondary offering. Alibaba had bypassed Hong Kong in favour of New York for its blockbuster 2014 IPO, the world’s second biggest on record at US$25bn, but more recent regulatory changes in Hong Kong made the internet company reconsider. At the same time, US-listed Chinese firms such as China Biologic Products and Bitauto announced plans to go private in a widening trend of delisting.

The epic migration of Chinese listings looks set to accelerate in the next few years as market reforms in Hong Kong and Shanghai are lowering listing and financing hurdles for tech firms. The gravitational pull has also shifted: China’s economy today is 10 times bigger than it was in 1990s, while the rise of Asian capital markets provides global investors with access to great investment opportunities outside the US.

Hong Kong also now offers the additional benefit of mutual market access between mainland China and the outside world – through the Stock Connect programme. This has been very successful in boosting capital flows between the exchanges and is expected to gather further momentum as domestic Chinese A-shares are gradually added to major international indices.

It’s all relative

For Chinese firms in the US, rising scrutiny has made overseas listings less attractive on a relative basis in recent years, while trade frictions between the two countries amplify their macro risks. Fraud allegations against Chinese companies such as Luckin Coffee have prompted US regulators to publicly warn of the risks related to investing in Chinese stocks.

More recently, the Trump administration has been pressurising some US government pension funds to pull out of indices that include Chinese shares, while proposed new legislation in Congress could lead to the delisting of foreign companies – predominantly Chinese ones – that don’t comply with US auditing regulations.

While the bill still needs to be passed into law and some sort of agreement between the two countries could still be reached, the likely outcome is that many Chinese companies on US exchanges will seek listings in China. As at August 2020, there were well over 200 Chinese ADRs listed in the US, totalling around US$1tn in market cap. The transfer of some of this paper to Chinese exchanges promises to further deepen liquidity in China’s equity markets.

Hometown push

Hong Kong has recently taken bold steps to allow unprofitable companies and those with dual-class share structures to go public. This has cleared roadblocks for many technology firms that previously could only head for the US. As listing conditions continue to improve, it is likely that private tech firms planning to go public will increasingly prefer to stay in Greater China.

It’s not just internet stocks being lured to Hong Kong. Healthcare IPOs have boomed in the city following the introduction of new rules in 2018, relaxing restrictions on pre-profit and even pre-revenue biotech companies seeking listings. Companies like Innovent Biologics and Cansino Biologics have also successfully raised capital. With new deals flourishing, the Hong Kong stock exchange was the world’s number one bourse by IPO value in both 2018 and 2019.

At the same time, the authorities in mainland China have been highly active in liberalising their markets, particularly in the past five years. Besides the Stock Connect programme, other initiatives include removing quota limits for qualified foreign institutional investors and relaxing equity financing rules for A-share companies.

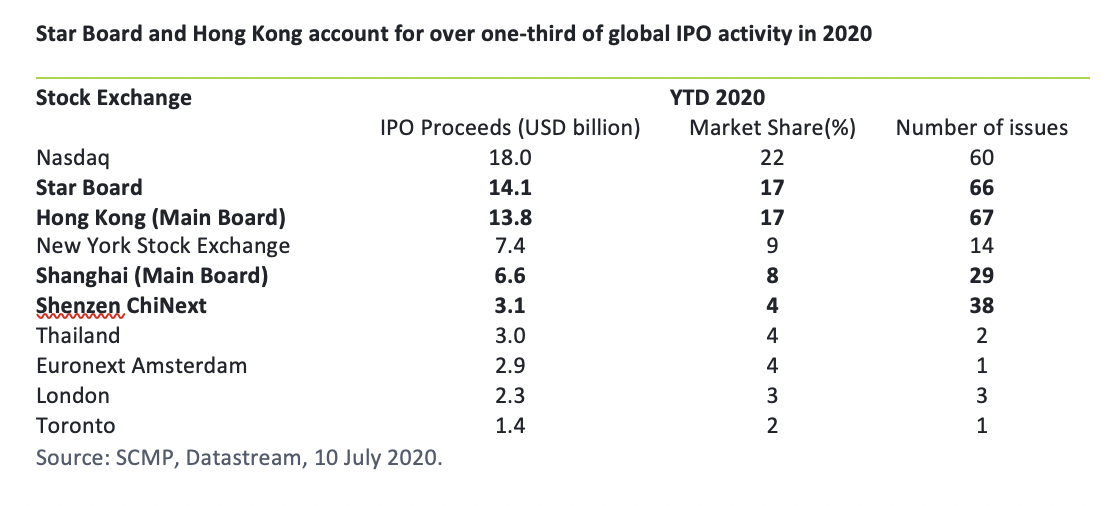

Regulators also recently launched a new venue known as the Star Board for tech start-ups, with relaxed profit requirements and trading curbs. The new board opened last year in July and while still at an early stage with just over 150 companies listed, it is already attracting high-profile names. For example, Chipmaker SMIC debuted on the exchange in July 2020, while the even larger fintech giant ANT Group recently announced it has begun proceedings for a listing.

Following the fanfare around Star Board’s launch, regulators are preparing to adopt an IPO registration system for Shenzhen’s ChiNext board, an older venue for Chinese tech stocks. If successful, the listing reform could bring a new wave of tech IPOs to Shenzhen.

Challenges remain

A key challenge facing the relisting of many Chinese firms is their so-called VIE or variable-interest entity ownership structure, which was designed decades ago to bypass China’s ban on direct foreign ownership in sectors like technology and education. The structure allows overseas listed vehicles to maintain some control over profit flows and business operations in China through contractual arrangements.

Unwinding VIEs can be slow and costly, but there are signs that listing rules may be easing. China is starting to allow some VIE listings on the Star Board. Red chips – companies incorporated overseas and controlled by Chinese government entities – can now sell shares on the venue even if they have a VIE structure.

Summary

When a door closes, a window opens. We think the great journey West is coming to an end for most Chinese tech firms, whose homeward shift has most likely passed the point of no return. Backed by a vibrant economy, Chinese capital markets have grown tremendously over the last three decades, offering strong liquidity and a solid investor base for companies seeking to list. The returning tech industry leaders, in turn, will add to the diversity and depth of greater China’s markets, as well as their internationalisation. This gives investors a greater mix of options and channels by which they can tap China’s long-term growth story.

You can learn more about Fidelity’s Asia expertise and investment strategies HERE.