Customers who choose annuities with a level income will be better financially than those who opt for escalating annuities, new research from Canada Life has shown.

The retirement specialist found that the annuity payback period when choosing an index linked annuity is around 22 years, compared to a level starting income. This means most customers will be better off choosing the higher starting income rather than an escalating annuity where the starting income is lower but increases over time in line with inflation or a fixed percentage.

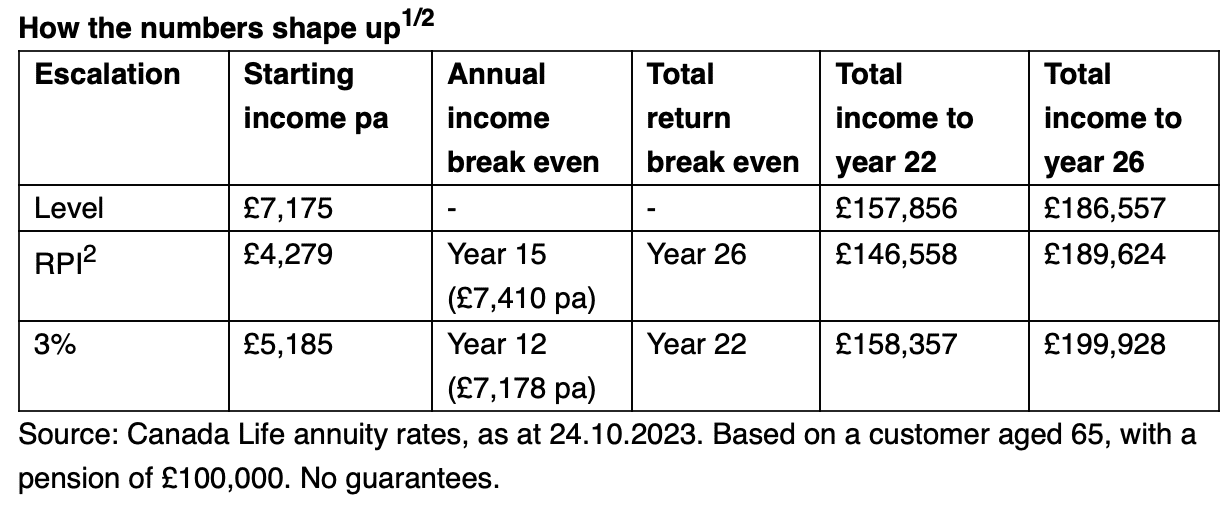

Canada Life’s data showed that someone aged 65 buying an annuity with a 3% fixed annual increase would be aged 87 before their total income beat the level income. For RPI-linked annuities, the age rises to 91.

As an example, someone aged 65 with a pension of £100,000 would receive a starting income of £7,175 with a level income, reaching £157,856 by age 87 and £186,557 by age 91. In comparison, a RPI-linked annuity would offer a starting income of £4,279 and not break even until year 15 with an income of £7,410, reaching £146,558 by age 87 and £189,624 by age 91.

Nick Flynn, retirement income director at Canada Life, said: “Annuities are the only 100% secure and risk-free way of generating a retirement income that lasts as long as you do. However, inflation has the power to erode your buying power over time, which is why annuity providers offer the ability to inflation proof or index link your income, so that your income can increase in line with your bills.

“While it’s easy to get lost in the myriad of options available on annuities, one thing appears to be a sure-fire bet. For most people, when you’ve made the decision to buy an annuity, choosing the certainty of a level income is likely to be the best economic decision they will make.”

Flynn said for those concerned about inflation, often a blend of annuities and income drawdown can deliver an optimum retirement income.

Source 1: Canada Life benchmark annuity rates over time, aged 65, £100,000 purchase price, no health or lifestyle factors, level, RPI linked and 3% escalation. Rates as at 24.10.2023.

Source 2: Canada Life has assumed an average RPI rate of 4% over the period as illustrative only, and makes no economic forecasts of the actual rate of RPI. RPI could average higher than, or lower than, 4%. If RPI averages higher than 4%, then the ‘total return break even’ point timeframe will reduce compared to a level starting income.