In this month’s three-year track record Juliet Schooling Latter, research director, FundCalibre, talks to the managers of the Schroder Asian Alpha Plusfund.

There have been plenty of headwinds for Asian equities in the past three years as the impact of more virulent strains of Covid; the ongoing uncertainty surrounding China (namely its moves toward common prosperity and the slowdown in its growth engine); and the upward trajectory of global/US interest rates have all put pressure on the market.

However, there is now an argument that there is more opportunity across the region. Covid is largely in the rear-view mirror; China (although still facing significant challenges) is now over 40 per cent cheaper than it was back in 2021*; and it looks like we’ve reached peak rates – with cuts forecast in the not too distant future.

We may well be at a point where the dispersion across the market – in terms of sub-regions, countries and sectors – could be stark, creating opportunities for active managers. Asia also has a number of long-term tailwinds in its favour – urbanisation, rising incomes and the growth of the middle class for those that need a reminder.

This week’s fund managers believe that Asian markets are a stock-pickers paradise. The Schroder Asian Alpha Plus fund is a best ideas portfolio of 50 to 70 stocks, with manager Richard Sennitt using the large research team at his disposal for local market insight, quantitative screening and risk management.

Richard took over this fund from long-standing manager Matthew Dobbs in March 2021, having worked alongside him for many years. Richard has worked on Asian and emerging market equities for three decades, and also runs a series of other funds in the region – including the Schroder Asian Income, Income Maximiser and Oriental Income trust. He is joined on the portfolio by co-manager Abbas Barkhordar.

With a universe of some 5,000 stocks to choose from, the ethos behind the fund is that markets are inefficient and that it is easiest to capture the inefficiencies at the stock level, where in-depth proprietary research can provide considerable information advantage. Richard believes long-term returns are driven by valuation considerations, but is willing to exploit other opportunities if the investment case is strong enough. Ideas are sourced from Schroders’ huge regional analyst team, brokers and the managers themselves.

Each stock is then assessed, with the Schroders team forming an opinion on the value of the business based on fundamental research that looks at sustainability of returns, reinvestment opportunities, management and earnings. Valuation is important and the managers will look for a catalyst that could see the business’s fortunes improve.

While bottom-up stock selection will always be the primary driver of country allocation, there will be occasions where the manager seeks to overlay a specific country exposure given a relative view on the economic or market background.

The opposite can also be true. For example, Richard was strong in his belief that when China re-opened in late 2022, a lot of the share price momentum had already been priced in. The portfolio currently has 15.5 per cent in China, half that of the MSCI AC Asia Index**. Concerns over the lack of a bigger stimulus plan coming through have meant areas of concern, like the troubled property sector, remain in the spotlight.

Instead the team believe there are greater opportunities in the likes of Hong Kong, India and Taiwan. Hong Kong’s currency board imports interest rate policy from the US Federal Reserve, which has been a headwind. However, with rates set to fall, the hope is this will be more positive for growth in the future.

Richard says: “Valuations versus history are cheap and lots of our exposure is to areas like financials (such as insurance) which has low penetration across Hong Kong and China and has a good, long-term growth story. We also like some external-facing stocks, such as the industrials.”

The overweight to India is positioned more toward large-cap names, with Richard and Abbas having recently taken some money out of the small and mid-cap space as they feel it is fairly valued.

Almost 60 per cent of the portfolio is currently held in financials and information technology stocks**. Commenting on the latter, Richard cites a number of tailwinds, such as the cutbacks in some of the semi-conductor stocks in Korea and Taiwan, which was starting to have an impact on inventories (production cuts). He also says a number of names in both countries have benefitted from the growing interest in Artificial Intelligence.

The team are now seeing that aforementioned dispersion in markets, citing countries like Singapore, Philippines and Indonesia as those with companies “at more attractive levels than we’ve seen in the past”.

Turnover in the portfolio has been relatively low, although this could increase in a rate-cutting environment. That said, fast rate cuts will not impact the valuation focus on a stock-by-stock basis. Richard cites banks as an example, saying that although rate cuts would not be great, much of the expectation has already been priced in.

With an experienced management team – backed by a high quality team of analysts – we believe the fund has the ability to remain a core holding for those wanting active exposure in Asia.

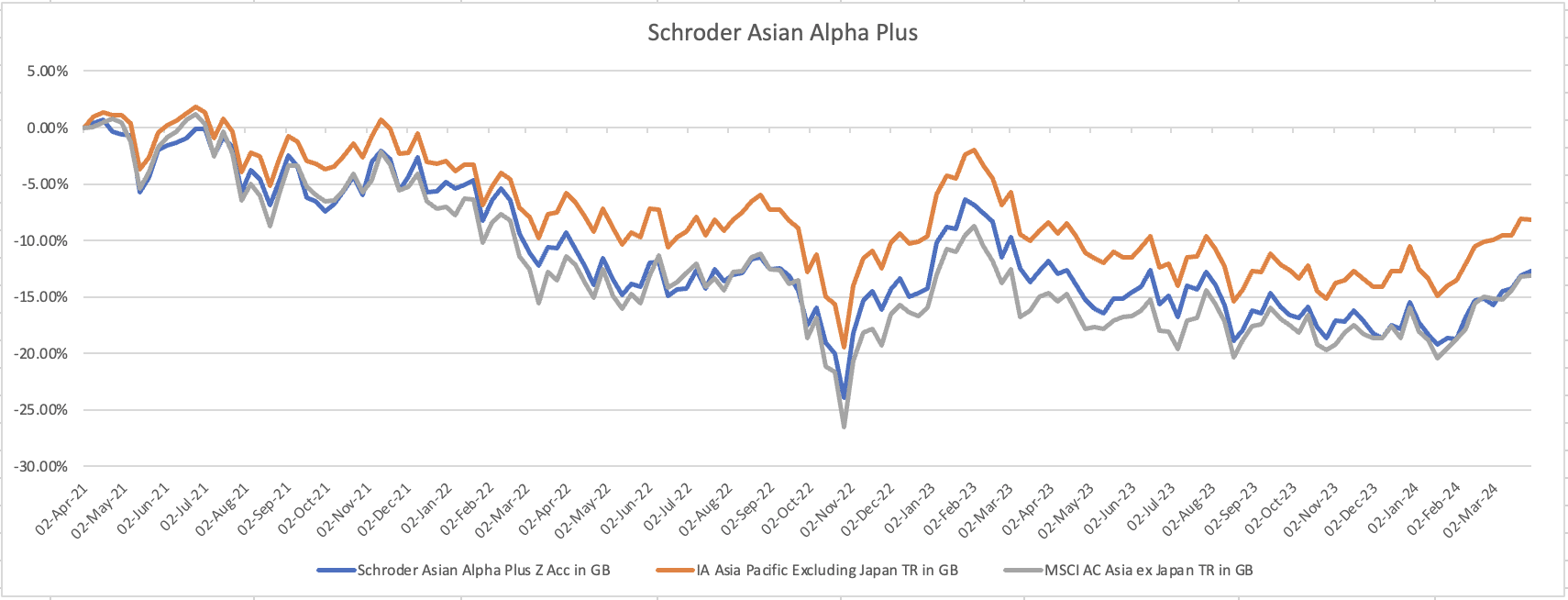

*Source: FE Analytics, total returns in sterling, 5 April 2021 to 5 April 2024

**Source: fund factsheet, 29 February 2024

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. Juliet’s views are her own and do not constitute financial advice.

Main image: ruslan-bardash-WMSvsWzhM0g-unsplash