The EdenTree Green Future Fund might be two years young, but the strategy behind it marks its 20th anniversary this year. Co-managers Charlie Thomas (CIO) and Tom Fitzgerald reflect on the how the long game has informed the portfolio so far and discuss what they aim to the strategy as it continues to bloom.

Charlie Thomas, Eden Tree

Thomas-Fitzgerald, Eden Tree

As in life, two years is not a long time in investing, especially for an investment you plan to hold for five or more years. Short-term sentiment and cyclical factors can often mask the inherent strengths of an underlying investment thesis. Successful investing requires patience.

While the Green Future Fund is technically in its infancy, the strategy behind it reached its 20th year in 2023. In an investment context, this is a mature strategy, having been developed through our respective investment careers, with Charlie forging the strategy in 2003, and Tom infusing the strategy with 10 years of global sustainable investing at EdenTree with particular strength in the disruptive innovation that is underpinning the transition. As co-managers, we seek to build consensus through a process that challenges each other’s assumptions and draws on the expertise of EdenTree’s wider sustainable investment desk.

The headline message from the Fund’s first two years is that it has performed robustly against close peers and has only marginally underperformed the broad-based IA Global peer group. Indeed, it has performed as you might expect given the market backdrop.

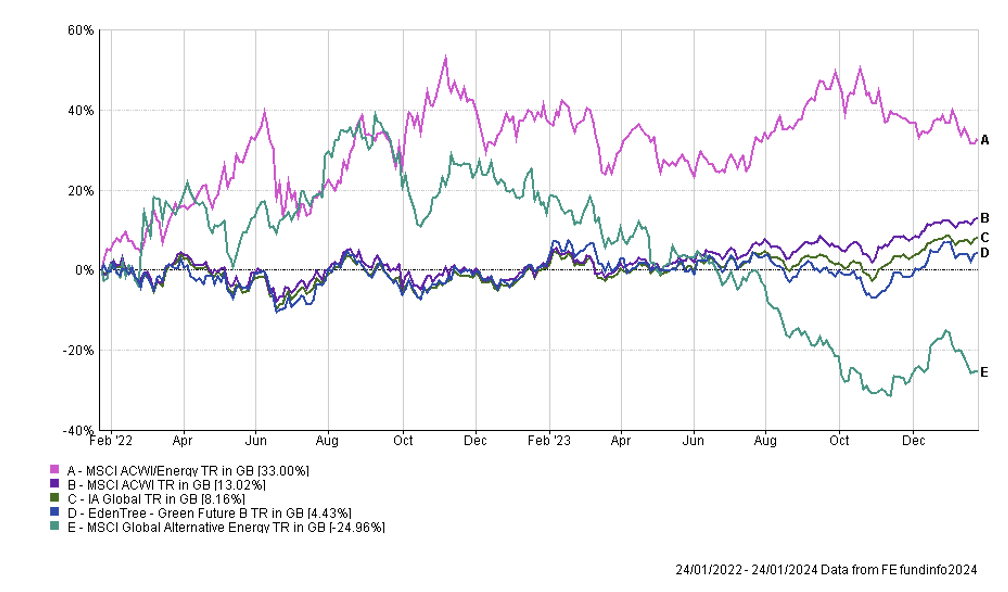

Figure 1: A performance profile that defies myths about green investing

Source: FE, net, bid-bid, GBP

That might seem a bold claim for a fund that produced a cumulative return of 4.4% in its first two years compared to 8.2% for the IA Global peer group and 13.0% for the MSCI ACWI index . However, core headwinds to relative performance against mainstream indices and index-focused funds have been largely a result of macro factors rather than stock selection or portfolio positioning decisions.

Given the strategy’s lifecycle focus on businesses with potential to grow and mature, it should not be a surprise that the Fund’s resulting small and mid-cap bias impeded relative returns, as it did for many funds with that orientation. Risk appetite for these market segments was crimped by the steepest tightened cycle in the Federal Reserve’s history, with knock-on effects for US regional banks changed, with the collapse of Silicon Valley Bank particularly denting risk appetite for smaller companies. Indeed, the Fund is well placed to benefit from both improved sentiment towards small and mid-cap stocks, as interest rates edge lower, as well as the potential longer-term tailwind of the small-cap premium.

Second, the period saw a vast chasm between the performance (and contribution) of the traditional energy sector to the market cap indices, on the one hand, and Fund’s investment in the alternative energy sector, on the other [see Figure 1]. This was driven by a combination of rising interest rates, Russia’s abhorrent invasion of Ukraine and a general market retreat from ESG-related stocks.

Third, the Fund has no exposure to the Magnificent Seven, and tends to be structurally underweight the US (holding 49.4% of AUM versus 63.7% for the index at the end of the period) given the breadth of opportunities elsewhere. For this strategy, as will many global strategies, it is difficult to justify the concentration risk associated with a benchmark weighting in the US.

The risk characteristics of the Fund are more closely aligned with the mainstream market than people might generally expect, highlighting careful management of factor risk (e.g. associated with companies sizes, valuations and underlying economic exposures) and the strength of the proposition’s stock-picking and thematic characteristics.

Competitive returns from the transition to a greener economy

The Fund was launched in a year that was to become dominated by war (with associated impacts on commodity prices and inflation), rising interest rates and weakening sentiment towards ESG. Those early months were a time to be cautious, yet opportunistic. We sought to make tactical use of the mispricing we witnessed in some areas of the market. This is a Fund for patient capital, and we are patient investors.

Read the full article HERE: EdenTree Green Future 2 Year.

Find out more HERE.