Markets now appear to be expecting no landing, with equity markets seeming to have turned a corner from some of the negativity of last year – but is this optimism overstated? As we enter the second quarter of 2024, Fidelity Multi Asset Open range portfolio managers Chris Forgan and Caroline Shaw explain why they believe a cautious and flexible approach to asset allocation is prudent to navigate what comes next.

What a difference a year makes

Compared to our peers, the Fidelity Multi Asset Open range has been defensively positioned for some time. Our reasoning has been based on a number of factors. Primarily, we were concerned that markets had not fully adjusted to the reality of the significantly tighter monetary policy that was required to combat the inflation upswing. Last year in the US, lending standards tightened, demand for credit fell, credit card delinquencies rose, and mortgage rates jumped. Core inflation remained elevated, and the US yield curve inverted, often a precursor to a recession.

However, equity markets shrugged off these challenges. Economic growth, at least in the US, remained robust despite much higher interest rates. Equity markets rallied in 2023 and have continued in the same vein in 2024 so far, recently making new all-time highs.

The market consensus has swung from pessimism early last year to increasingly expecting a Goldilocks outcome this year, where inflation and interest rates gradually fall, and growth remains strong. Equity markets appear to suggest that all is well with the world. But are they correct?

Improving picture warrants some action

It is true that a number of indicators have improved over the past six months. In particular, US growth has remained remarkably and unexpectedly strong, aided by the continued strength of the labour market. Meanwhile, both headline and core inflation in major developed markets have fallen significantly, helped by loosening global supply chains and wage pressures, as well labour market dynamics. Retail sales in the US have also been resilient over the period. Finally, financial conditions have eased to become more supportive of growth.

Managing risk is an integral element of portfolio management and, to reflect this improved data, we have reduced (but not abandoned) the defensiveness of our portfolio. We recently introduced a long position in the S&P 500 index to gain greater exposure to those beneficiaries of US economic resilience. Within US equities, we have rotated some exposure from the more defensive utilities sector into the iShares Edge S&P 500 Minimum Volatility UCITS ETF and the BlackRock Global Unconstrained Equity fund. US utilities have rallied recently, but we believe the sector could face some future challenges as market consensus becomes more optimistic. The iShares Edge S&P 500 Minimum Volatility UCITS ETF allows us to retain defensive characteristics but in a more diversified manner than that of the US utilities sector.

But under the surface the outlook is not all rosy

However, as is often the case in periods of optimism (or pessimism for that matter), investors appear to have embraced a binary view of the macroeconomic landscape. In this binary world, ‘improving’ has been replaced with ‘good’. The outlook is certainly better than it was, but things are not as rosy as all-time-high equity markets would lead you to believe for a number of reasons.

First, many major markets are performing poorly. The US stands alone as a major economy that is still posting solid growth.

Germany and the UK are either in or close to recessions, while China remains stuck in second gear with little immediate prospect of a turnaround. Second, global manufacturing remains weak, as evidenced by ISM surveys. Third, the inversion of the US yield curve is becoming less extreme, but it is still present, and recessions have typically occurred as the curve dis-inverts. Fourth, lending and credit standards are still tight, much tighter than they have been for most of the previous 15 years. This is particularly harmful for small businesses, which are more likely to be financing at higher rates than larger firms. Fifth, the excess savings built up during the pandemic that have powered the global economy in the years since have largely been depleted.

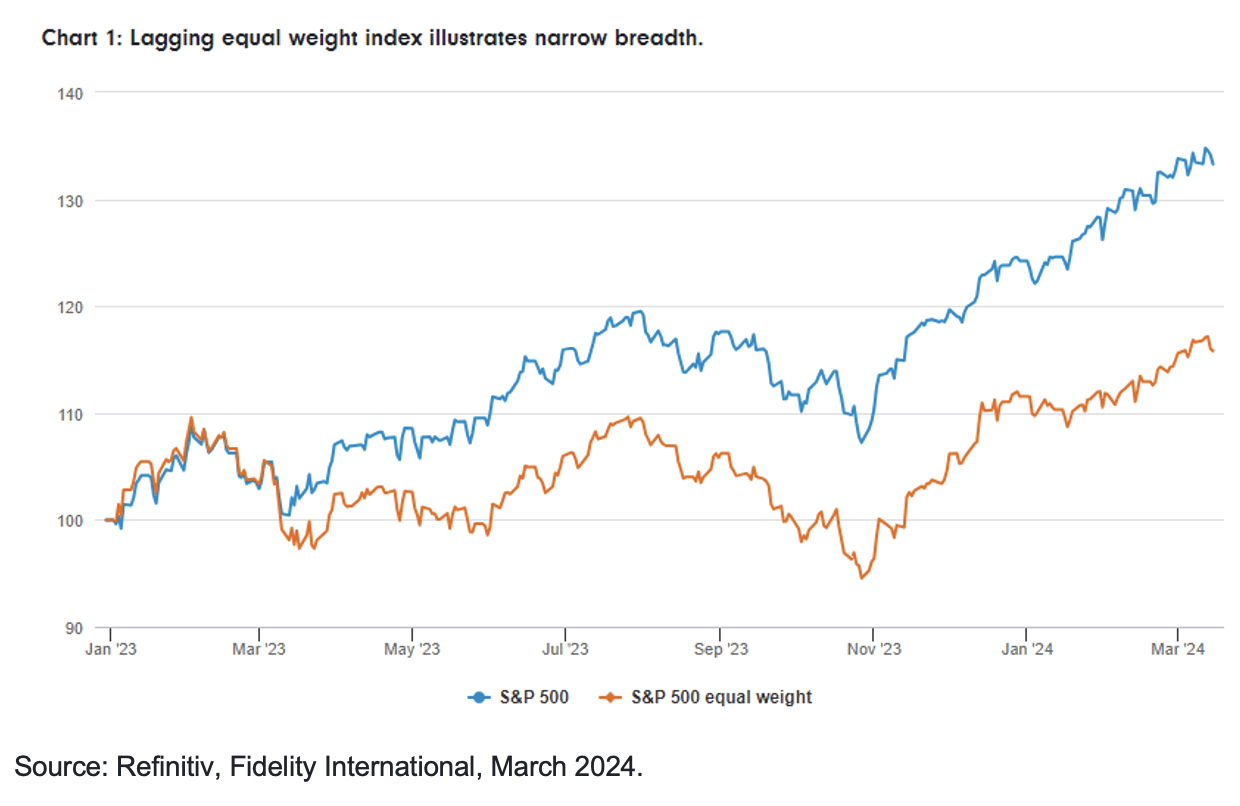

Finally, market breadth has been remarkably narrow recently. The majority of the gain in the S&P 500 in 2023 was driven by the largest stocks, particularly the ‘Magnificent Seven’, a group that includes Apple, Microsoft, Amazon.com, Nvidia, Meta Platforms, Tesla, and Alphabet. The narrow breadth of the US markets can be illustrated with the following chart that compare the returns of the S&P 500 index with the S&P 500 Equal Weighted index.

Investors should not get carried away by the headline performance of global equity markets. Looking beneath the surface, it is largely driven by only a handful of US companies to date, which does not inspire confidence in the narrative that there has been a wholesale improvement in the economic outlook.

Retaining preference for defensiveness

So, the outlook is potentially not as bright as markets would have you believe. Things have improved, but it’s possible investors have become overly optimistic. We still think a relatively defensive stance is warranted given the economic backdrop. Several of our positions aim to capture the upside potential of US equities but those positions are augmented by others that should offer more protection if the market were to get overextended and experience a pull back – this includes the Fidelity Global Dividend Fund, and the iShares Edge S&P 500 Minimum Volatility ETF. We also have exposure to the gold price through both the physical commodity and gold mining equities, which is a traditional hedge for risk-off market environments and should find some support from falling interest rates and any escalation in geopolitical tensions.

Conclusion

The Fidelity Multi Asset Open range benefits from its flexibility and diversification, using a broad range of asset classes. We would continue to monitor our positioning and add to risk assets if we saw a sustained improvement in the economic outlook.

Important information

This information is for investment professionals only and should not be relied upon by private investors. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. Fidelity’s Multi Asset funds use financial derivative instruments for investment purposes, which may expose the fund to a higher degree of risk and can cause investments to experience larger than average price fluctuations. Changes in currency exchange rates may affect the value of an investment in overseas markets. Investments in emerging markets can also be more volatile than other more developed markets. The value of bonds is influenced by movements in interest rates and bond yields. If interest rates and so bond yields rise, bond prices tend to fall, and vice versa. The price of bonds with a longer lifetime until maturity is generally more sensitive to interest rate movements than those with a shorter lifetime to maturity. The risk of default is based on the issuers ability to make interest payments and to repay the loan at maturity. Default risk may therefore vary between government issuers as well as between different corporate issuers. Due to the greater possibility of default, an investment in a corporate bond is generally less secure than an investment in government bonds. Reference in this document to specific securities should not be interpreted as a recommendation to buy or sell these securities, but is included for the purposes of illustration only. Issued by FIL Pensions Management, authorised and regulated by the Financial Conduct Authority and Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited.