For this month’s three-year track record article, Fund Calibre research director Juliet Schooling Latter looks at the TB Evenlode Global Equity fund, which has a high conviction portfolio.

“Managing a portfolio is like flying a plane through the night skies – you have limited visibility, but you know you’ll be alright if you carry certain North Stars in your mind.”

When it comes to the TB Evenlode Global Equity fund, co-manager James Knoedler says these North Stars come in the form of companies which have clear competitive advantages and are willing to spend money to protect these advantages.

Launched in July 2020, the fund is a high conviction portfolio which focuses exclusively on ‘quality’, cash-generative companies. The fund, which James manages alongside Chris Elliot, was initially seeded with their own money, before being made widely available to investors in May 2021.

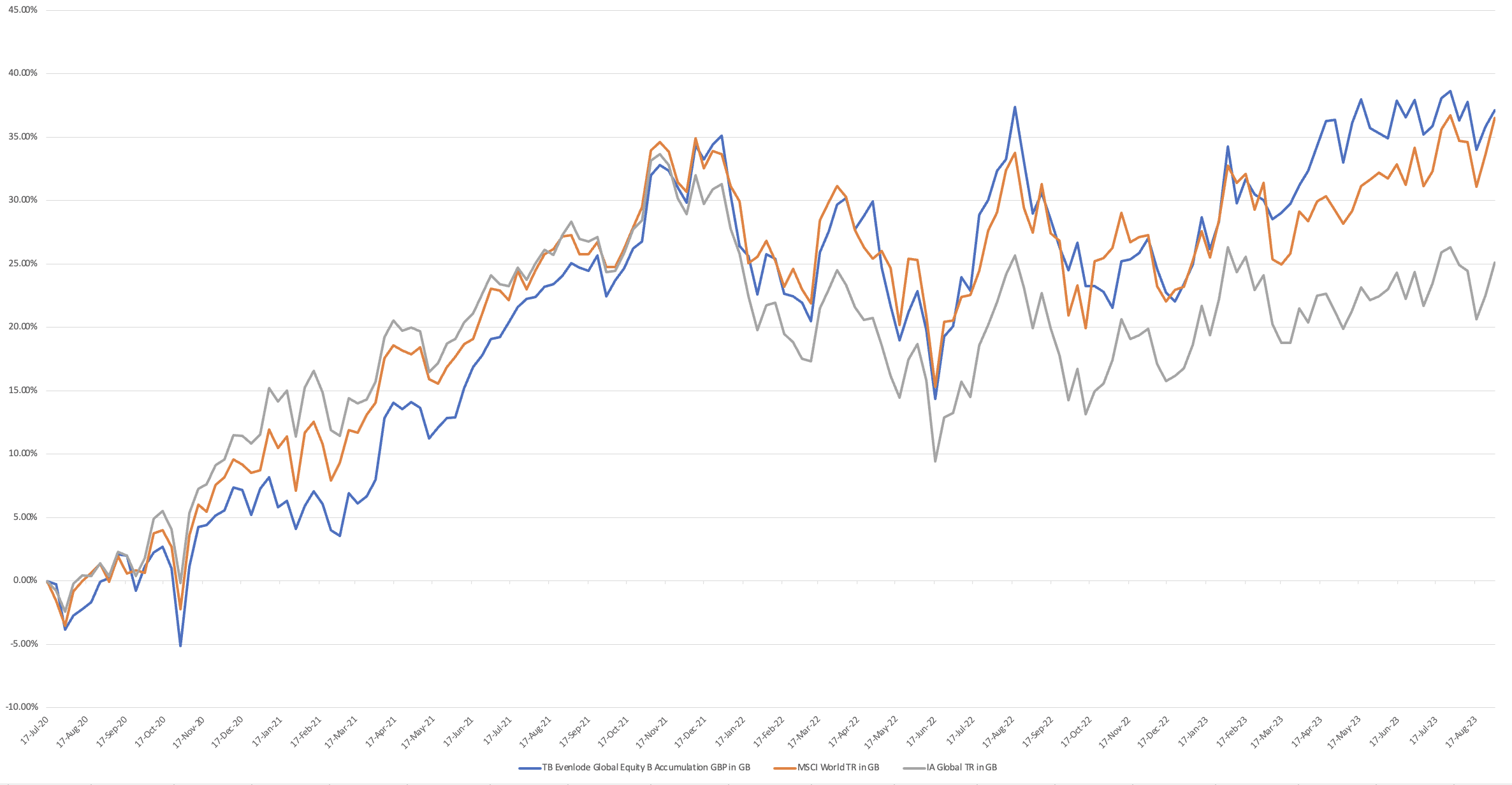

Quality companies are expected to be durable, offering products and services which are often needed in any market environment. This fund’s underlying holdings have demonstrated this in what has been an incredibly challenging three years, with the likes of Covid, war and inflation all impacting on markets. Since launch, the fund has comfortably outperformed its peers in the Investment Association Global Sector.

“Our expectation is, and our experience has been, that the superior compounding of the companies we own will overwhelm an opportune entry point. We look for quality first, but then I would say the valuation (of a company) is more important than growth. We’re happy to own companies with mid-single digit returns – provided there’s a sustainable growth runway. I’m not sure the majority of our peers would do the same,” said James.

The managers use a proprietary research and portfolio management software system, “Eddie”, which helps the team identify compelling valuation opportunities, which the managers will discuss in their weekly investment team meetings.

In essence, Evenlode’s investment approach revolves around identifying market-leading companies with high cashflow returns on capital, manageable business risks, and limited financial leverage. The aim is to generate returns through the growth of fundamental value over time, driven by the favourable economics of the underlying business and organic compounding of free cash flow. The result is an investable universe of around 80 stocks.

Bottom-up and ‘bull-bear’

Although bottom-up, Chris says the team cannot ignore thematic moves, as they spend a lot of time thinking about risk management and what could impact the competitive advantage a company has. He cites the strides made in generative Artificial Intelligence (AI) as an example, and what effect it could have on the likes of Alphabet/Google (a 5 per cent holding in the fund)*.

He says: “We had to ask questions like would Alphabet have to spend more money to make searches compliant with AI? We did lots of research, like speaking to ex-employees and a deeper dive into what generative AI does well today. We found it was still very early on in the cycle, and there were still things which need to be addressed. So we don’t see this as a threat to Alphabet in the next 5-10 years.”

While turnover is low – the implied holding period is 6-8 years – the team has sold the likes of LVMH, and partial allocations to Hermes and Microsoft when valuations became challenged.

To keep the valuation discipline at the forefront of the process the team employ ‘bull-bear’ meetings on every company holding every six months. To tackle confirmation bias, no team member who is a supporter of a specific holding, gets the bull position.

A good example of the benefit of this strategy was the decision to sell Intel, which was initially held across all three Evenlode strategies.

James says the team had data showing Intel was losing some market share to its big rival (AMD) in x86 chips (the type of processor used in most computer and server hardware). The team paid for access to people who were professional buyers of x86 chips, as well as former company employees to garner a greater insight as to whether a meaningful change was taking place.

“The bigger picture was the PC market was stagnant so the opportunities in this market come through data centres. The problem is three companies now dominate the data centre market (Microsoft, Google and Amazon). All these companies are technologically sophisticated and can develop all their own software and hardware. So it looked and felt like it was time to sell Intel – which has proved the right decision thus far,” he adds.

Resilient to rate hikes

The best endorsement of the portfolio’s resiliency has been its performance in a rate hiking environment. James says the assumption throughout the 2010s has been that quality growth would get smashed in this scenario, but this has not occurred. He says many of the holdings have actually been rate insensitive and can operate in numerous environments.

Examples of current stocks the team are bullish on include data analytics and consumer credit reporting company Experian, and Jack Henry, a provider of software into the US banking sector.

Chris says although the latter is a business which has sold off this year – due to the Silicon Valley banking crisis in the US – it has not impacted the strides they are making as a firm. He says: “Banking firms are now being pressurised into improving the technology they have, specifically with regards to recognising the assets they have versus liabilities. Jack Henry has a long runway for growth and can take market share from others who have not been as focused on the core banking platforms.”

We feel this fund is well positioned given it is driven by a clear and proven investment process, used by the team across numerous strategies. It has proven resilient in recent times and is a strong consideration as a core holding in a very competitive sector.

*Source: fund factsheet, 31 July 2023

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. Juliet’s views are her own and do not constitute financial advice.

TB Evenlode Global Equity July 2020- August 2023