In this month’s three-year track record, Juliet Schooling Latter, research director, FundCalibre looks at the Schroder British Opportunities Trust.

With its differentiated approach of investing in both private and public equities, the Schroder British Opportunities Trust (SBO) was one of the few products launched in response to the Covid-19 pandemic – as it sought to back a number of exciting opportunities in the UK small and mid-cap market.

Investing in roughly 30-50 holdings, SBO targets two specific businesses, these are ‘high growth’ firms which are set to benefit from the rapid change in corporate and consumer behaviour; and ‘mispriced growth’ companies which offer products and services with long-term structural growth drivers.

The private element offers an extra string to the trust’s bow by widening out the investable universe. With more than £10bn in assets under management, Schroders Capital has been investing successfully in private companies for more than 25 years.

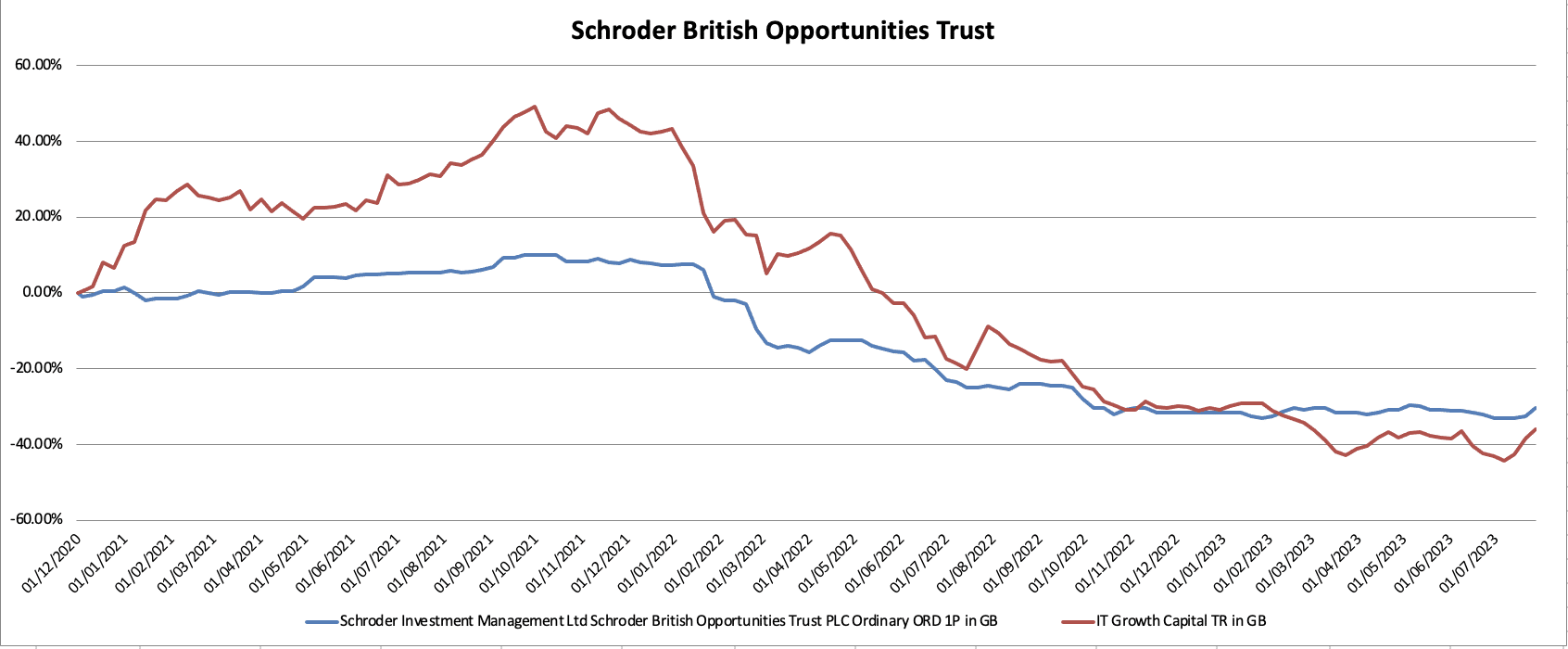

SBO has a four-strong team at the helm, with Rory Bateman and Uzo Ekwue running the publicly listed side, while Tim Creed and Pav Sriharan target the private sector. In a nutshell, it is quite a unique proposition, but it has had the misfortune of being in the eye of the storm surrounding UK equities for much of its life. Although the trust’s net assets have held up well at £76.8m, poor sentiment has hit hard, plunging the trust to a 33 per cent discount (the market cap of the trust is currently £51.3m)*.

Uzo Ekwue says the trust’s share price was resilient from launch in December 2020 until the start of 2022**. This is in line with interest rate hikes in the US, the downturn in tech and the shift from growth to value. The trust was also trading at a slight premium until the outbreak of war in Ukraine early last year.

In addition to poor sentiment towards UK equities in general, the exposure to UK small caps and the significant discount investors are putting on private equity as an asset class has also hit hard.

Timing has not helped to some degree – at launch the trust targeted an equal split (50/50) between public and private assets. This has now switched, with shareholder approval given last year to raise the private portion, which now accounts for 65 per cent of the trust.

The trust now invests in some 26 public companies, with nine private equity holdings. Pav Sriharan says eight of the nine private companies are currently meeting or exceeding their base expectations – yet this is not being reflected by the market. In fact, the group says there is a 55 per cent discount on the private equity investments alone**.

The team believes this is a mispricing opportunity, as it does not reflect the strength of these private companies. Examples include Mintec, a UK provider of food commodity prices. Pav says: “Mintec has had a significant increase in valuation over the past quarter. It’s not only beating expectations organically, but it has also acquired a competitor in the US, which is transformational given the size of the company going forward.”

Other examples include specialist insurance provider CFC and global mobile parking payment business EasyPark.

Although it is too early in the life of the trust to look at exit routes for these private holdings, the team did benefit from the merger of Waterlogic – a global designer, manufacturer, distributor, and service provider of drinking water dispensers – into Culligan International. The trust retained a minority share in the business but also received a £2.4m distribution.

As for the public side, Uze says the market is in a “beat and raise phase” – essentially where companies are expected to beat expectations and raise earnings per share guidance. She says these types of companies are being rewarded, with the market favouring anything with a growth story in it.

A recent addition on the public side has been Bytes Technology, this is a value-added reseller focusing on products made by technology manufacturers/vendors to private and public sector organisations.

The trust has also seen bids on three public holdings with Ideagen and Euromoney both being acquired by private equity businesses, while listed healthcare software developer EMIS Group was taken over.

With £8m sitting in cash, the managers are aware of the challenging market environment at present, but also believe there are plenty of attractive valuations to be taken advantage of.

Returns look attractive even at these valuations

Pav says the trust is materially mis-priced when you do the maths. Adding that even if the fixed life of the portfolio did end in 2028 (it has the scope to go beyond this cycle) and was liquidated on today’s NAV (discount of 33 per cent) investors would still get around an 8.5 per cent annualised return**.

He says: “We don’t believe that is right, given the implied discount on the private equity investments is significant. We’ve seen strong contractions in the market and good growth coming through the businesses we hold. It is an attractive entry point.”

This trust has faced a number of significant headwinds in its short lifetime, and there may well be more to come. However, the underlying businesses tell a completely different story, indicating this could be a great opportunity to tap into UK PLC at such a significant discount. The mix of the private equity allocation focusing on growth capital and small/mid-market buyout areas, coupled with the significant depth of research in listed and private equities makes this an attractive option. Any catalyst for change, coupled with improved education, could see UK equities re-rate quickly from these depressed levels.

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. Juliet’s views are her own and do not constitute financial advice.

*Source: Association of Investment Companies, 1 August 2023

**Source: Schroders British Opportunities Trust – Annual Report 2023