The M&G Wealth technical team answer some of the questions they regularly relieve regarding what triggers a chargeable event on a bond, and to calculate any gain arising?

Q: What is a chargeable event?

A: A ‘chargeable event’ happens when certain events occur or money is taken out of a bond. Details are available here.

A calculation is done to see if a chargeable event gain arises.

Q: What are the tax consequences of a chargeable event gain on a bond?

A: If there is a chargeable event gain then there may be Income Tax due.

Q: What events cause a chargeable event gain?

A: Types of ‘event’ causing a chargeable event gain include:

- Death of the life assured (or last to die of lives assured) where benefits are payable.

- Assignment (full or in part) for money or money’s worth.

- Maturity of the policy.

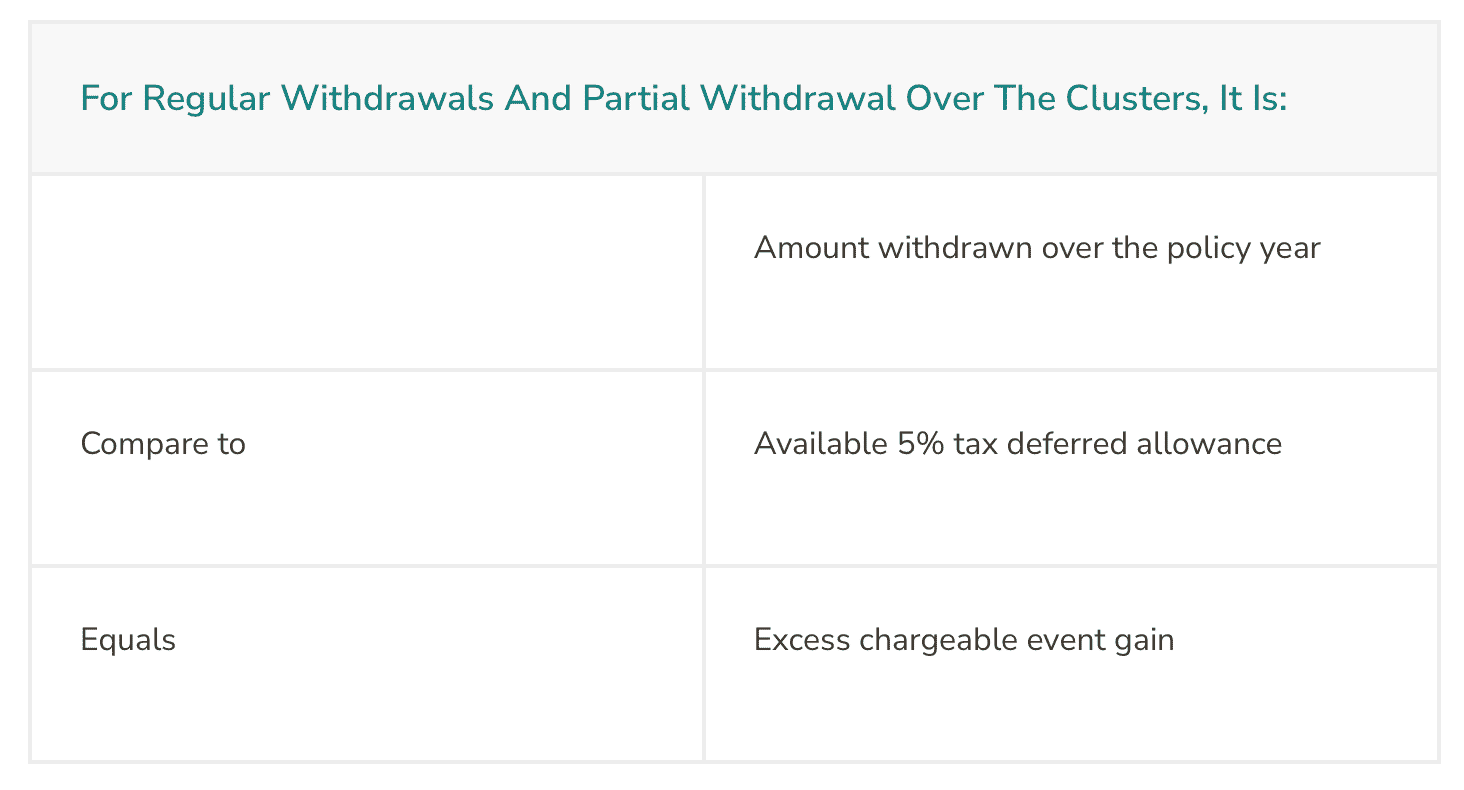

- Partial or regular withdrawals across a whole bond, in excess of the 5% tax deferred allowance.

- Surrender of the bond, whether in full or surrender of segments.

Q: How do you know if a chargeable event gain has arisen?

A: Firstly you need to determine the circumstances causing the chargeable event. The type of event will determine the type of chargeable event gain calculation required and, indeed, when the chargeable event gain takes place. There are generally two types of chargeable event gain calculation:

- Final chargeable event gain.

- Excess chargeable event gain.

Q: What’s the difference between a final gain and an excess gain?

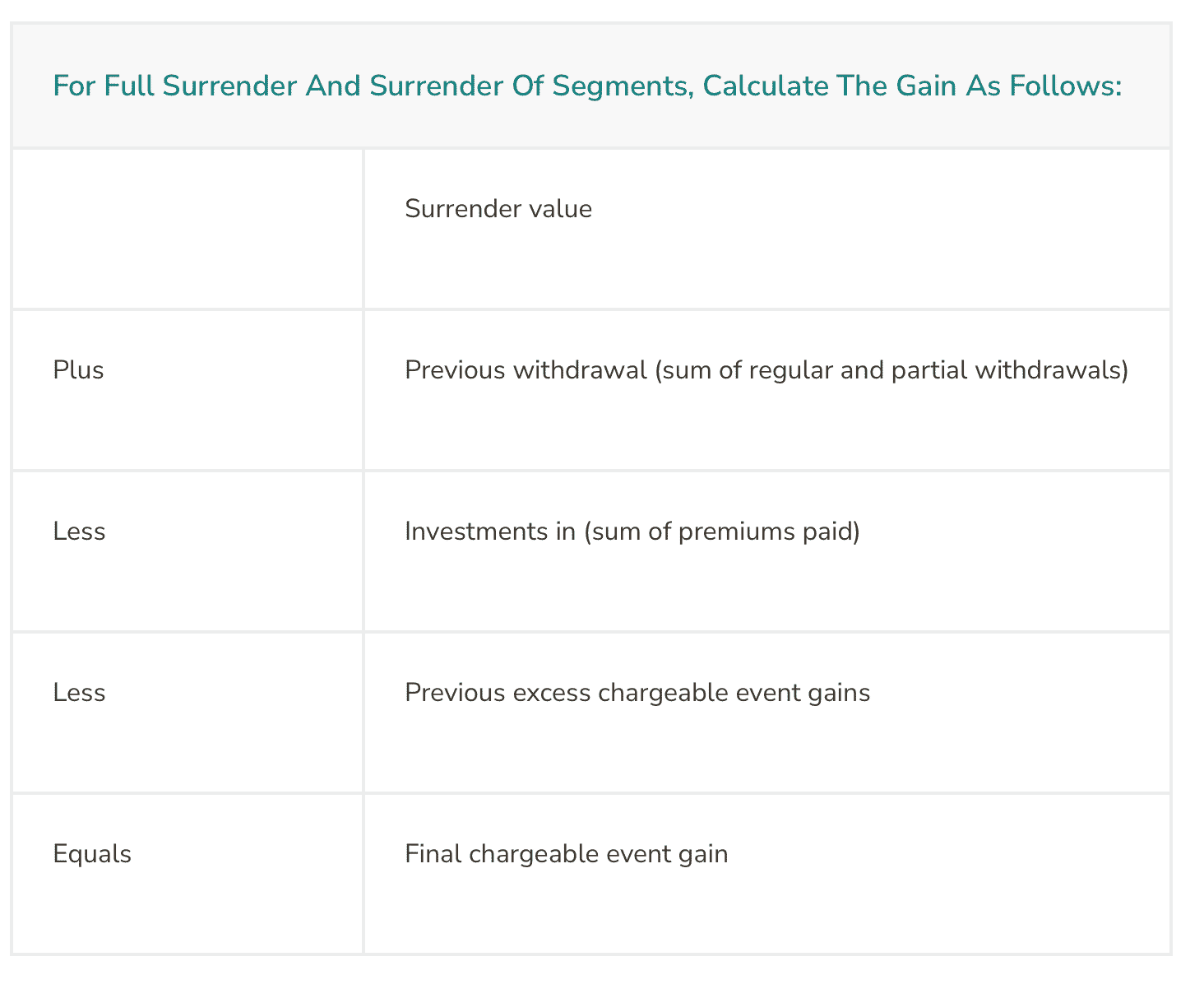

A: A final chargeable event, as the name suggests, takes place when the bond, or segments of the bond, end. Events such as surrender in full or segments, death of the life assured giving rise to benefits and maturity are all final chargeable events.

An excess chargeable event happens when withdrawals are made above a certain limit, but the bond continues with all the segments intact. Part assignments for money or monies worth, and regular or partial withdrawals in excess of the 5% tax deferred allowance are excess chargeable events.

Q: Why is the excess gain so high when the bond might not made any profit?

A: Chargeable event legislation states that where withdrawals in the policy year exceed cumulative 5% allowances then a chargeable event gain will arise. It is important to remember that this ‘mechanical’ calculation bears no correlation to the economic performance of the bond.

Q: When is a gain calculation done?

A: A final chargeable event gain is calculated immediately.

An excess chargeable event gain calculation is done at the end of the policy year.

Q: Is the chargeable event gain calculation the same for a final and excess gain?

A: No, there are specific formulas for each type

What is the formula for a final gain?

If you are dealing with a surrender of segments, you need to remember to proportion the figures to the number of segments being encashed.

What is the formula for an excess gain?