Share-linked structured products often offer higher rates of return but the risks compared to index-linked products make them riskier in terms of capital loss for client portfolios, warns Ian Lowes, managing director of Financial management and founder of StructuredProductReview.com

It has now been more than two years since a retail structured product matured with a loss to investors capital*. Unfortunately, there was always going to be a point in time where this fantastic run would come to an end and it looks as if that time is nearly upon us.

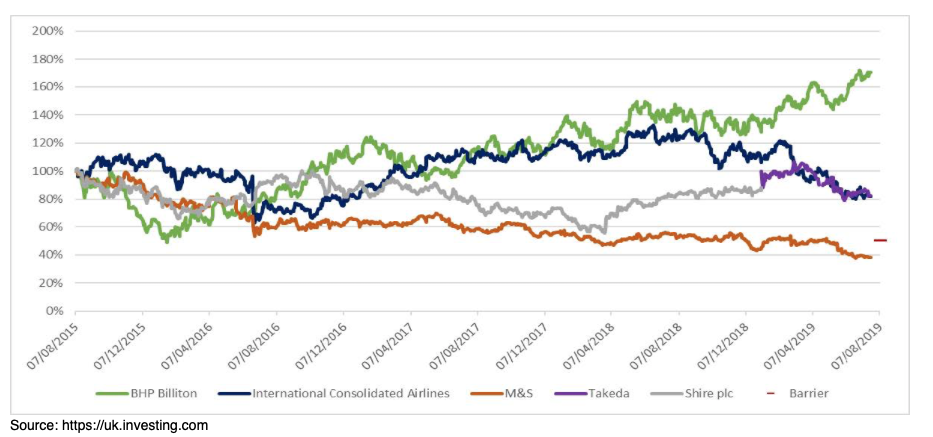

Four years ago, in June 2015, Meteor released the 4 Year FTSE 4 Monthly Income Plan August 2015. A product which offered investors a gross monthly income of 0.67% (8.04% per annum). The income has been paid monthly, through the term, irrespective of performance, but the return of capital is conditional upon all of the underlying shares to which the plan is linked not losing more than half their value over the four years.

The shares in question are BHP Billiton plc, Marks & Spencer plc, International Consolidated Airlines Group and Shire plc. (now Takeda Pharmaceutical).

The following graph charts the performance of the shares over the term of the plan:

This is a clear example of the risks involved in the more speculative investments that are share linked plans.

At the time of writing, whilst BHP Billiton has soared well above its initial level, International Consolidated Airlines and Takeda have struggled, however both are still comfortably above half their value recorded at the beginning of the plan.

M&S on the other hand has significantly underperformed with the share price sitting at around 38% of the initial level and as such, below the 50% protection barrier incorporated into the Meteor plan.

If the plan was maturing today, as opposed to the 7th August 2019, investors capital would be reduced by 1% for every 1% M&S share price was down meaning a loss to capital of over 61%.

The Meteor product was not one that we recommended to our clients under the Lowes ‘Preferred’ Plans*.

When the income that has been paid out over the term is accounted for, investors would see a loss of 29.5% ignoring the impact of any tax that may have been due on the income.

Looking at the rest of 2019, there are just 38 more capital at risk products that have their final maturity date this year, of these there are 31 in which capital is linked to the FTSE 100 and one which is linked to the performance of the FTSE 100 and S&P 500.

Whilst all of these currently look set to deliver positive returns, the remaining six plans are share-linked products that aren’t going to fair as well.

Two of the remaining share linked plans look set to return original capital at best, whilst the other four are perilously close to triggering losses at maturity of more than 50%. As is typical with such products the return of capital is dictated by the worst performing share and for these four investments, at time of writing those shares are BP, Rio Tinto, Vodafone, BAE Systems and Standard Chartered. Currently, BP, Rio Tinto and BAE Systems are all above their initial levels but Vodafone and Standard Chartered are between 39% and 49% down depending on the product.

The final index date for these four plans range from the 6th September 2019 until the 13th December 2019 and whilst all shares are currently above the all-important 50% barrier, it clearly wouldn’t take much to trigger a small fall, which would lead to a significant loss.

Share linked structured products of this nature have been rare over recent years with only two products released into the retail space since 2016 compared to 56 in 2014 alone.

The latest was launched in July. The latest offer, the Hilbert 3 Stock Defensive Autocall Issue 1, clearly shows the risk-reward trade-off for such investments compared to the more mainstream FTSE 100 linked structured products that have become the norm in the retail sector.

Currently a FTSE 100 linked ‘Kick-out’ product requiring the FTSE to be at, or above the initial level on an annual maturity observation date, might offer around 10% for each year held, whereas the Hilbert plan is offering a potential gain of more than twice as much with twice as many opportunities to trigger a successful maturity.

The plan is linked to the shares of Barclays Plc, Aviva Plc and Vodafone Group Plc. Whilst, again there is a 50% capital loss barrier, the parameters for a positive maturity allow for the shares to fall by as much as 40% by the end of the eight-year, maximum term and still trigger a very attractive gain.

Whilst this may sound attractive, as the fortunes of this investment are linked to the worst performing of three shares, in our view, it is a high risk, speculative investment that should only ever be considered for a small part of an investment portfolio, if at all.

Whilst it has been an amazing period for UK structured products over recent years, the Meteor 4 Year FTSE 4 Monthly Income Plan August 2015 is a stark reminder that the acceptance of risk doesn’t always pay off.

The high potential returns of share-linked plans may seem incredibly attractive, however it must be kept in mind that the typical higher returns on offer associated with these types of plans are a function of the increased potential that they may mature with no gain or large losses.

*Source: Data collected by StructuredProductReview.com

* Lowes ‘Preferred’ Plans draw on Lowes Financial Management’s specialist knowledge and 20+ years experience of researching and recommending structured products to its clients.

Lowes recently published a 10-Year report on Structured Products, analysing the market since the Financial Crisis, which can be accessed here.