Juliet Schooling Latter, research director at FundCalibre, continues her look at funds and/or mangers with a three-year anniversary, focussing this month on the US and the GQG Partners US Equity fund.

Accounting for roughly 60%* of the global stock market, it makes sense the US is the most efficient market in the world, particularly when it comes to the behemoths at the top end.

Overall, there are 11,882 ratings on stocks in the S&P 500** – doing some basic maths, this tells me there is an average of almost 24 analysts (23.7) covering each stock. Outperformance is not impossible, but doing so consistently is very difficult.

The past few years have made this even more so. The market has been dominated by a narrow set of stocks, be it the FAANGs, the Magnificent Seven and, more recently, the Fab 4 (Nvidia, Amazon, Meta and Microsoft).

Style biases have been tough to overcome – growth and value have had their moments in the past three years. To really outperform you need a unique selling point to stand out from the crowd and the performance of this week’s fund suggests it has exactly that.

GQG Partners U.S. Equity strategy is an unconstrained, concentrated portfolio of high-quality large and mega-cap US companies with durable earnings. Their focus is on forward-looking quality, rather than companies that have done well historically. This view of quality allows them to strip away labels like value and growth in favour of long-term compounding.

The fund is managed by a quartet of managers, who are supported by 12 research analysts – the team also manage global and emerging market strategies at GQG. One of the management quartet is Rajiv Jain, who founded the firm in 2016, and is both chairman and chief executive officer. He has over 25-years’ experience in the industry and is joined by fellow managers Brian Kersmanc, Sudarshan Murthy and Sid Jain.

The investment process starts with a quantitative scoring and ranking system to identify potential investments from a universe of listed and actively-traded global equities. While this system cannot fully capture forward-looking quality, it employs common metrics such as stable financials, profitability, efficiency, and economic moats to evaluate companies. The research ranks companies on an aggregate quality score of 1-10.

The investment team will also use their cumulative historical knowledge as one of their primary sources of investment ideas. The next stage sees a fundamental analysis of a company. The research focuses on understanding the business’s ecosystem, evaluating key drivers of success, barriers to entry, sustainability, management effectiveness, regulatory environment, and end-consumer behaviour. The final portfolio is extremely concentrated at 15-40 stocks, targeting companies which can deliver growth over 3-5 years.

Investigative journalists and vicious sellers

One of the key standouts from their peers is the four-strong team of investigative journalists at GQG. They do not speak to the sales side and sit separately from the rest of the team. The goal is to eliminate any biases and help the managers make decisions by focusing on different parts of a business’s ecosystem. When looking at certain stocks or themes, this team will converse with the likes of regulators, ex-employees and politicians to gain further insights.

A good example of their benefits came at the back end of 2021, when the fund was heavily exposed to technology. The team found, through their work with recruiters, that one of the biggest tech/semiconductor providers was pulling its internal recruitment team. This was an important element in the team, cutting their exposure amid concerns stocks were at peak margins at this point in the cycle. The team subsequently invested in energy stocks where they saw earnings coming through.

Another difference for this quality strategy is the team are not afraid to be “vicious sellers”. With turnover ranging from 60-100% a year – which is high for a quality strategy. The team are “quick to sell, slow to buy” – liquidity and the ability to sell is key to the team and allows them to change style quickly.

This has happened on numerous occasions. For example, in early 2023 amid the Silicon Valley Banking crisis, the firm sold a top 10 position in Charles Schwab after it fell 20% in a day; avoiding a further 20% loss. The view is sell first, ask questions later, as they can always buy a stock back.

On a defensive footing

While the US elections may take up a number of column inches, the result is not top of mind for the team. The focus is on bottom-up with macro awareness. They will wait to see who wins, where they lean and the impact this has on the earnings trajectory of companies.

The fund is currently on a defensive footing – with the team targeting certainty at sensible valuations. They have cut their information technology exposure from roughly 50% at the start of the year to 17%***. Cuts to software names earlier in the year – due to concerns over disruption caused by AI – were supplemented by recent cuts in July due to high multiples in the sector.

By contrast, they have added to positions in utilities, consumer staples and healthcare. Boring areas are offering growth in the team’s view – utilities include the likes of data centres, while unloved telecoms look attractive from a valuation perspective.

What the team want is a level of certainty which comes from a mix of yield (which helps form part of the total return) and clarity of earnings growth within a five-year view. The fund is currently balanced from a style perspective and is cheaper than the wider market – it has a 24x P/E (vs.26x for the S&P) and has a dividend yield of 1.6% (vs. 1.3% for the S&P)***.

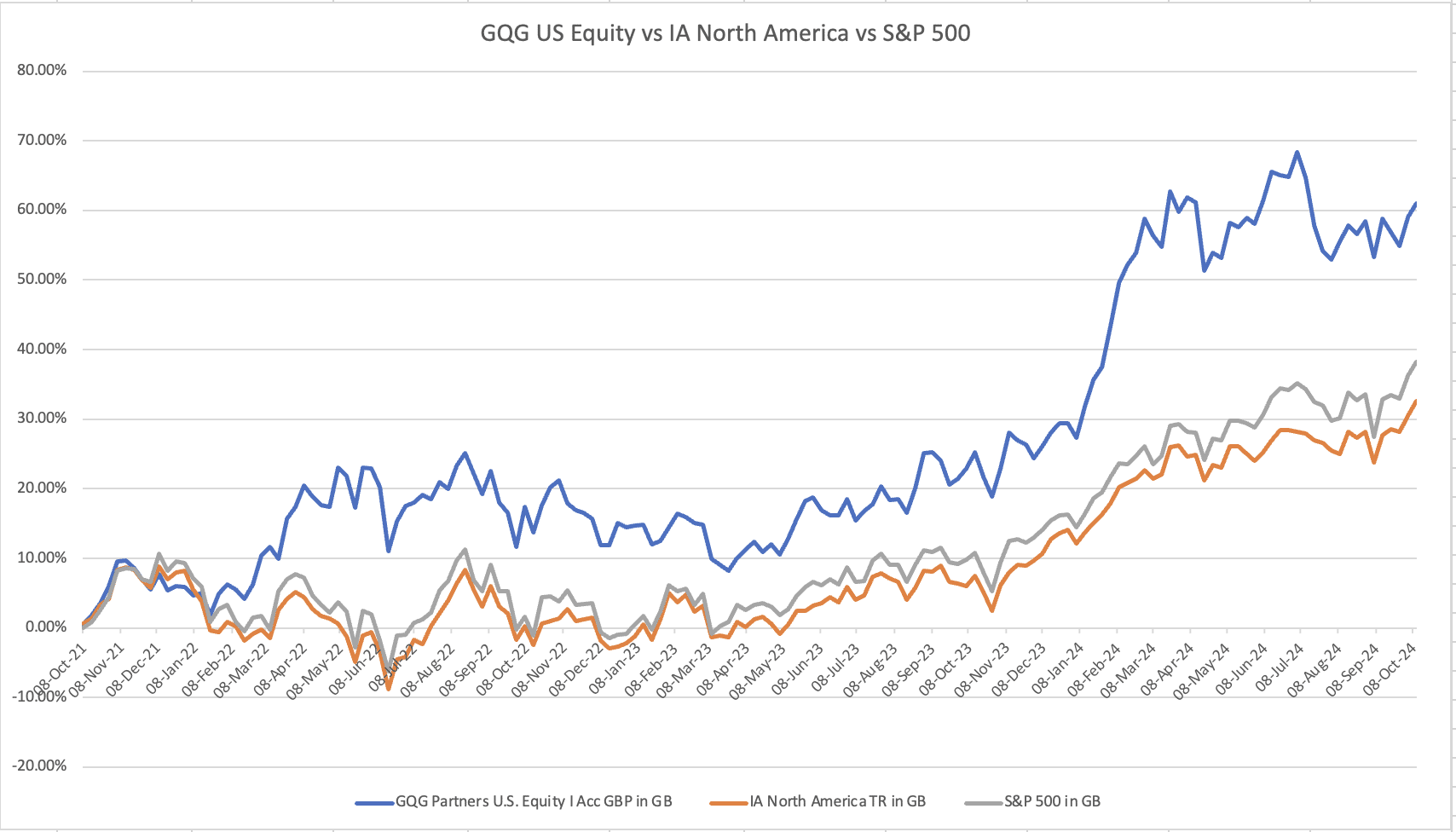

This fund looks to deliver a smooth journey to investors by avoiding heavy drawdowns. With a rolling 5-year beta of 0.8 and rolling alpha of 3-4% above the S&P 500***, it has delivered thus far. Although the fund is still relatively young, the combination of being style-agnostic, quick sellers with management on the ground in the US has proved fruitful, as has the extra facet offered by the investigative journalists. We see no reason why this success cannot continue.

*Source: Statista, January 2023

**Source: FactSet, 20 September 2024

***Source: fund factsheet, 31 August 2024

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. Juliet’s views are her own and do not constitute financial advice.

Main image: nasa-1lfI7wkGWZ4-unsplash