Amid increased uncertainty over the future path of policy rates, the role of money market strategies has come back into focus. With rates expected to ease only modestly from elevated levels, investors are increasingly focused on preserving income, liquidity and capital stability without taking too duration risk.

In this environment, Portfolio Managers Tim Foster and Izzi Halewood at Fidelity International, highlight why money market strategies still offer an attractive solution for investors looking to navigate a higher-rate world.

Over the past year, it has become increasingly clear that the global economy is not returning to the pre-Covid environment of near-zero interest rates.

The inflation shock of recent years has reset monetary policy, lifting estimates of neutral rates across developed markets.

While central banks have begun to ease at the margin, policy remains tight and well above the norms that prevailed for much of the previous decade.

In the United States, the Federal Reserve is widely expected to deliver further rate cuts, but the scope appears limited, with one to two cuts the most likely outcome for this year.

The case for more aggressive easing remains unconvincing. Economic growth has proved resilient, fiscal support remains material and business surveys continue to point to underlying momentum.

Labour market conditions are softening only gradually, reducing the urgency for a decisive policy shift. While political considerations may encourage limited easing, the data does not support a rapid return to accommodative policy.

Current market pricing broadly reflects this view, with expectations centred on limited further easing rather than a full cutting cycle.

In Europe, the outlook is more settled. The European Central Bank appears inclined to hold rates for an extended period, reflecting its institutional emphasis on inflation control and credibility.

The bigger risk appears to be weaker inflation dynamics over time, rather than renewed overheating. Even so, any policy response is likely to be cautious and incremental.

Meanwhile, the Bank of England sits between these two approaches. UK growth could strengthen this year, while easing wage pressures and cuts to household energy bills provide scope for a limited number of additional cuts.

Taken together, this backdrop points to modest easing from a high starting point, rather than a return to a low rate regime.

Policy rates may drift lower, but a sharp or sustained reduction now looks unlikely, although uncertainty around growth, inflation and policy reactions remains high.

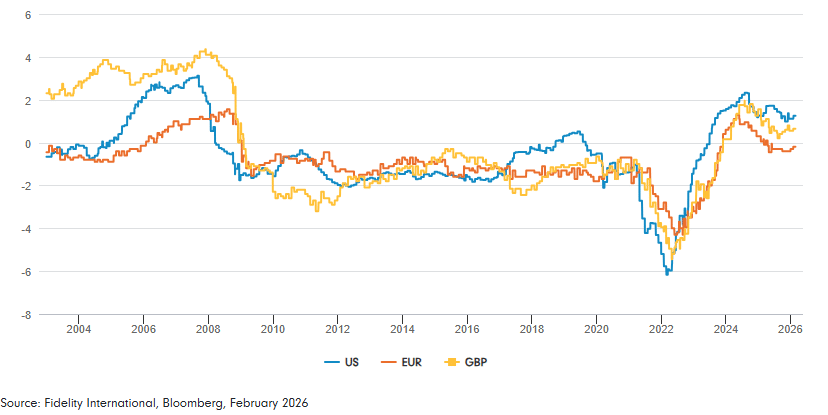

Real policy rates remain well above post-2010 levels:

Portfolio Implications

This backdrop has clear implications for portfolio construction. Given resilient growth and elevated policy rates, the risk-reward profile of longer-duration assets has become less attractive.

Heavy sovereign issuance, particularly across developed markets, has structurally altered bond market dynamics, weakening the traditional defensive role of long-dated government bonds.

As a result, the focus has shifted away from capital gains driven by falling yields, towards income, liquidity and flexibility.

For money market investors, this means maintaining discipline, rather than wholesale repositioning. Our approach remains centred on short duration and high-quality exposure, supported by selective and measured adjustments.

Within a cash context, we have scope to extend the strategy’s average maturity modestly – which is typically up to 60 days – to capture incremental yield where the risk-reward is attractive.

This reflects expectations of limited further easing, rather than a full cutting cycle. Crucially, such positioning remains firmly within a money market framework and does not compromise liquidity.

Overall, the emphasis remains on resilience. Portfolio construction is designed to perform across a range of outcomes, including scenarios where rates remain higher for longer or where volatility in risk assets resurfaces.

Money market strategies remain an attractive solution

In a higher neutral-rate world, they are playing a more strategic role as core building blocks within portfolios. Investors can earn a meaningful yield while preserving capital and maintaining daily liquidity.

Money market strategies can act as stabilisers at a time when policy uncertainty, geopolitical risk and the potential for risk-asset volatility remain elevated.

Periods of market stress often create sudden liquidity needs, and in those moments access to capital matters as much as return.

Money market strategies provide that flexibility, allowing investors to redeploy capital efficiently as opportunities emerge.

Overall, the case for money market strategies remains compelling for investors seeking income, liquidity and resilience amid uncertain rate paths.

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. The writer’s views are their own and do not constitute financial advice.

This information should not be relied upon by retail clients or investment professionals. Reference to any particular investment does not constitute a recommendation to buy or sell the investment.

Main image: background, colourful, luke-chesser-IGtutkXikuc-unsplash