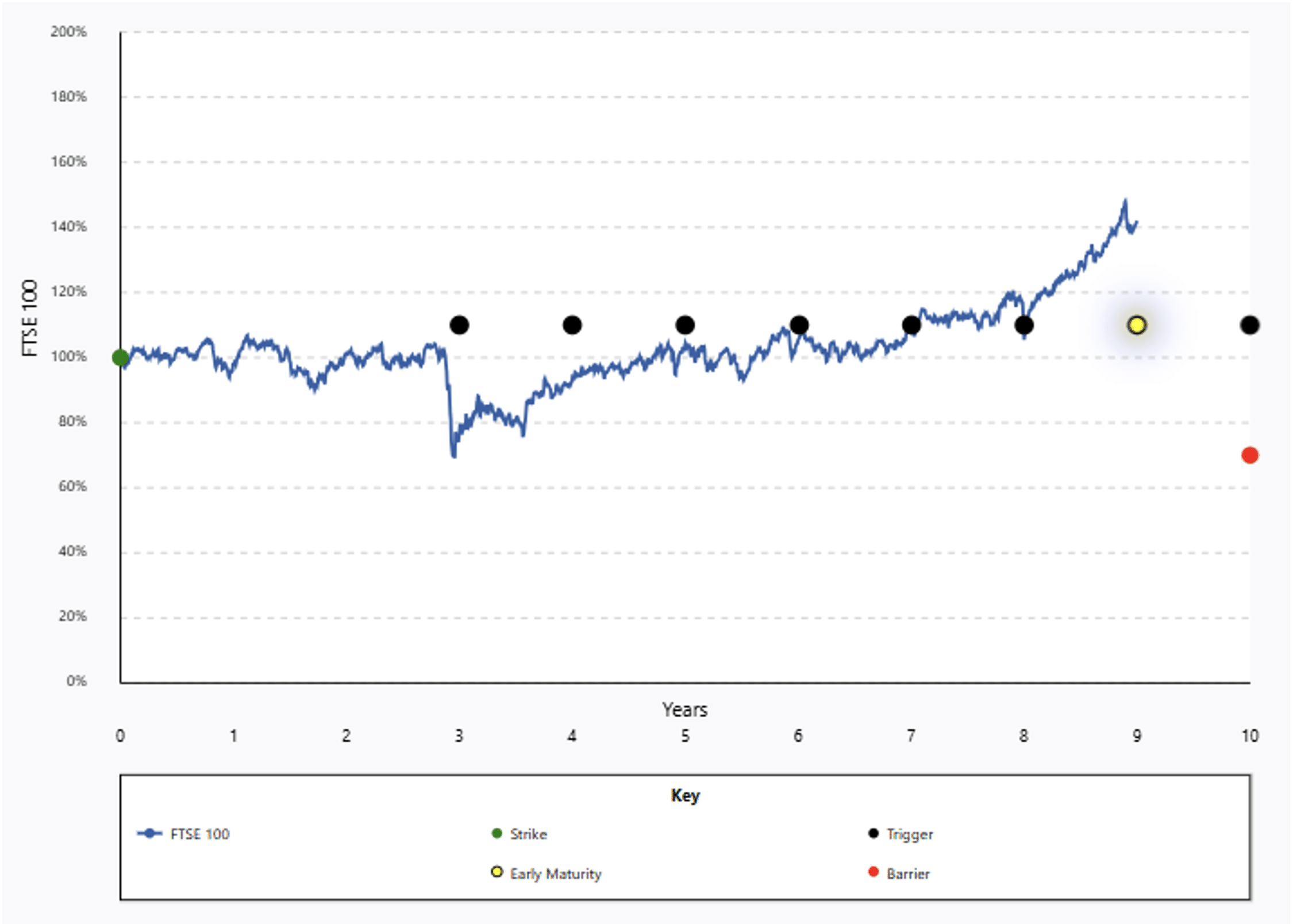

The longest running retail autocall matured on 7 April 2026, giving investors a 105.75% gain on their capital over 9 years, 11.75% per annum, despite turbulence in the markets over that time.

The April 2017 10:10 Plan, Option 3, the highest paying option offered by the Plan, gave investors a simple coupon of 11.75% for each year the Plan remained in force.

This Option of the Plan was set to mature on the first anniversary (from the third onwards) on which the FTSE closed above 8,084 points – 10% above the FTSE’s level when the Plan started, which was 7,349.47. The Plan had up to ten years to achieve that hurdle.

Traditionally, structured products offered 5-6 year maturity dates. Having the 10 year time frame means products have longer to deliver for investors, says Ian Lowes, co-founder of Autocalls UK, a collaboration between Lowes and IDAD Ltd.

Lowes explains the timeline for the April 2017 Plan and how it affected investor returns: “For the first 34 months the FTSE was relatively benign, and two months before the first potential maturity date it was only 117 points above where it had started. Then came the pandemic driven market crash, which briefly pushed the FTSE below 5,000. An April 2020 maturity became highly unlikely – however, with a gain of 11.75% accruing each year, a delayed maturity was far from a bad outcome.

“It took a further four years for the index to push confidently above 8,000. A 2025 maturity began to look probable, but the temporary trade‑driven market disruption in April that year caused another postponement – adding yet another 11.75% to the potential return.

“Early surrender outside of a triggered maturity was possible throughout the term and by way of an example, doing so in early December 2025 would have realised a gain of over 96%. Investors who let the Plan mature naturally ultimately benefited from a gain of 105.75% when maturity was triggered on the ninth anniversary.

“I have long subscribed to the firmly held – and I believe well‑proven – view that you simply cannot time the markets. None of us truly knows what will happen tomorrow, next month, or next year. This is one of the key reasons why I so strongly stand by the strategy that The 10:10 Plan represents. And the latest maturity provides one of the clearest illustrations of why.”

The Plan’s Option 1, a stepdown option maturing if the FTSE was at 90% of the initial level, matured on its fourth anniversary with a 28% gain, and the Second option, which required the FTSE to be at or above 7,349.47 on the third anniversary, matured on its fifth anniversary with a gain of 45%.

The April 2017 10:10 Plan’s protection barrier, the level below which the FTSE had to fall before investors lost capital, was 70% of the initial level.

The returns on structured products are net of all fees other than intermediary fees.

Lowes says: “Markets will always surprise us, but well-designed investment structures should not. The 10:10 Plan delivered because it was built to. Attempting to time markets isn’t possible, with long duration autocalls it isn’t necessary.”

The 10:10 Plan – April 2017 Option 3

10:10 April 2007 – Option 3 Timeline at a Glance

- Apr 2017 – Plan strikes at 7,349.47

- Jan 2020 – FTSE only +117 points since inception

- Mar 2020 – Covid crash briefly pushes FTSE below 5,000

- 2021–2023 – Recovery period; FTSE moves towards record highs

- Feb 2023 – FTSE exceeds 8,000 for the first time

- Apr 2025 – Trade‑related market wobble delays maturity

- Apr 2026 – Maturity with total return of 105.75%

Lowes says the latest 10:10 Plan, May 2026 Issue, with Goldman Sachs as counterparty, has three options, all of which will mature on the first anniversary, from year three, when maturity conditions are met:

Option 1: Step Down 102.5% to 82.5% – potential return 8.25% per year

Option 2: Level @100% – potential return 10% per year

Option 3: Hurdle@ 105% – potential return 11% per year

Maximum term 10 years – 70% capital protection barrier on final date if not matured earlier.