Fixed income Investment Director Ben Deane, Fidelity International, examines the sector and argues why passive strategies are structurally disadvantaged, creating inefficiencies that skilled active managers can exploit to deliver stronger, more consistent risk-adjusted returns.

High-quality short dated investment grade credit is increasingly being favoured by a broad range of investors, from individuals and wealth managers to pension schemes and corporate treasurers, for several reasons.

Firstly, credit spreads remain tight across many parts of the market, which in our view supports a more cautious approach to credit risk and reinforces the case for favouring higher-quality investment grade issuers over high yield.

Secondly, interest rate volatility remains elevated as inflation has stayed more persistent than expected and geopolitical risks, including the escalation in the Middle East during Q1 2026, have continued to drive swings in government bond markets.

In this environment, lower-duration strategies have generally proven more resilient, as shorter-dated bonds are less sensitive to interest rate movements and have typically held up better during periods of market stress.

At the same time, investors continue to seek opportunities to enhance income beyond cash holdings. While cash rates remain relatively attractive, short dated investment grade credit can offer a meaningful yield pick-up over both cash and government bonds for only a modest increase in risk.

This has supported growing demand from pension schemes, company treasurers, and other investors looking to optimise liquidity allocations or progress through the later stages of portfolio de-risking.

In addition, with the yield curve now upward sloping, investors can achieve an attractive level of income from short-dated credit without materially extending duration exposure, reinforcing its appeal as a compelling risk-adjusted allocation within diversified portfolios.

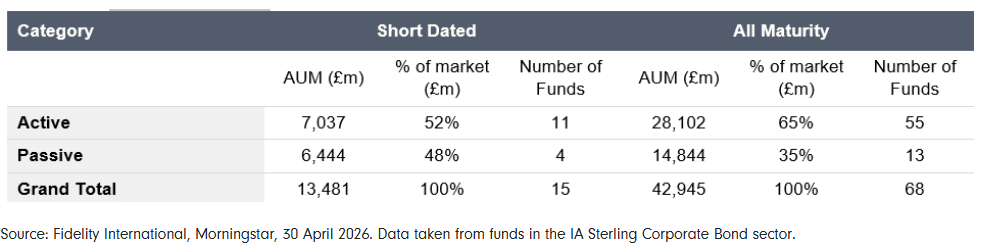

In short dated compared to all-maturity, passives represent a greater market share

When choosing short dated corporate bond funds, UK investors often look to passive vehicles, citing the lower return potential of the broader asset class.

Roughly a third of the all-maturity sterling corporate bond market is passive (£15bn out of £43bn) compared to almost half of the short-dated market (£6.4bn out of £13.5bn) per figure 1 below.

This may seem intuitive, as investors perceive there is little absolute return or potential excess return on offer in relatively low risk short dated corporate bonds. Therefore, why pay up for active management?

Figure 1: IA Sterling Corporate Bond sector, short-dated versus all-maturity

Passive is suboptimal in short dated corporate bonds

Despite this backdrop, we strongly believe that going passive in the short dated space is suboptimal, and this goes beyond the typical arguments for going active over passive, which include, for example, picking the winners and avoiding the losers (this certainly also applies here).

Our active approach specifically exploits the forced passive buying and selling at either end of the maturity spectrum.

Below we delve into this in more detail, highlighting the benefits of going active over passive in the asset class and how we specifically exploit short dated passive funds to our benefit.

As a general rule, passive funds underperform their indices on a net basis because of fees and transaction costs.

However, most passive funds tend to underperform their indices by more than the fees charged which we believe is due to the additional costs arising from elevated trading, associated with trying to replicate a short-dated index.

A 1-5 year index constantly has bonds entering the index as they move from six years to five years in maturity, and constantly has bonds falling out of the index as they move below one year in maturity.

This will lead to elevated trading for the passive community aiming to replicate this exposure, as they may be forced to buy and sell respectively at either end of the maturity spectrum.

To illustrate this, we compare the 1-5 year index we use for our Fidelity Short Dated Corporate Bond Fund with its all-maturity counterpart, to measure how many bonds would fall into the 1-5 year index (by moving from six years to five years maturity) and out from the 1-5 year index (by moving sub-one year maturity) over the following 12-months.

As of end-April 2026, 97 bonds would move from six years to below five years to maturity and enter the index while 103 bonds would move to sub-one year in maturity and fall out of the index, a total of 200 bonds.

The 1-5 year index contained 560 bonds as of end-April 2026, suggesting more than a third (36%) of the bonds in the index would move in the space of 12 months! And this excludes the impact from potential new issues.

This excessive and forced trading does not occur for all-maturity passive bond funds, and we’ve found evidence of short dated passive funds underperforming their indices more (after fees) than their all-maturity counterparts, despite being offered by the same provider and therefore presumably using the same trading processes.

Exploiting the passive community

As active investors, we are happy to take out-of-index exposure across sub-one year bonds and up to six year maturity bonds.

For example, we can buy a sterling investment grade bond with five and a half-years left to mature, knowing this is about to enter the 1-5 year index and therefore benefit from forced passive buying.

At the other end of the maturity spectrum, we can buy bonds with sub-one year maturity to take advantage of forced passive selling.

This paper has additional benefits and can prove to be an attractive hunting ground for active investors despite being so close to maturity.

At April-end 2026, 7% of the Fidelity Short Dated Corporate Bond Fund (all off-benchmark) matured in less than one year. Somewhat remarkably, the average yield to maturity on this sub-one year paper (5.19%) is greater than the yield on the index (5.15%), despite the lower interest rate risk associated with it.

Part of this yield advantage is due to forced selling by passives due to their rules-based, rather than value-based, approach.

Banks are also unwilling to expend a significant amount of their risk in such instruments, allowing us to take advantage of this technical backdrop.

Sub-one year paper also acts as natural liquidity as the bonds mature generating cash for the portfolio. This has further benefits in a rising yield environment as we can then deploy the cash into higher yielding securities.

Investors who use the fund as a cash diversifier often like this liquidity feature.

Time to consider an active fund?

The Fidelity Short Dated Corporate Bond Fund is primarily invested in high quality short dated corporate bonds and was launched almost 10 years ago, employing a highly active approach.

The Fund is managed within Fidelity’s highly experienced sterling investment grade portfolio management function, alongside our flagship Fidelity MoneyBuilder Corporate Bond Fund.

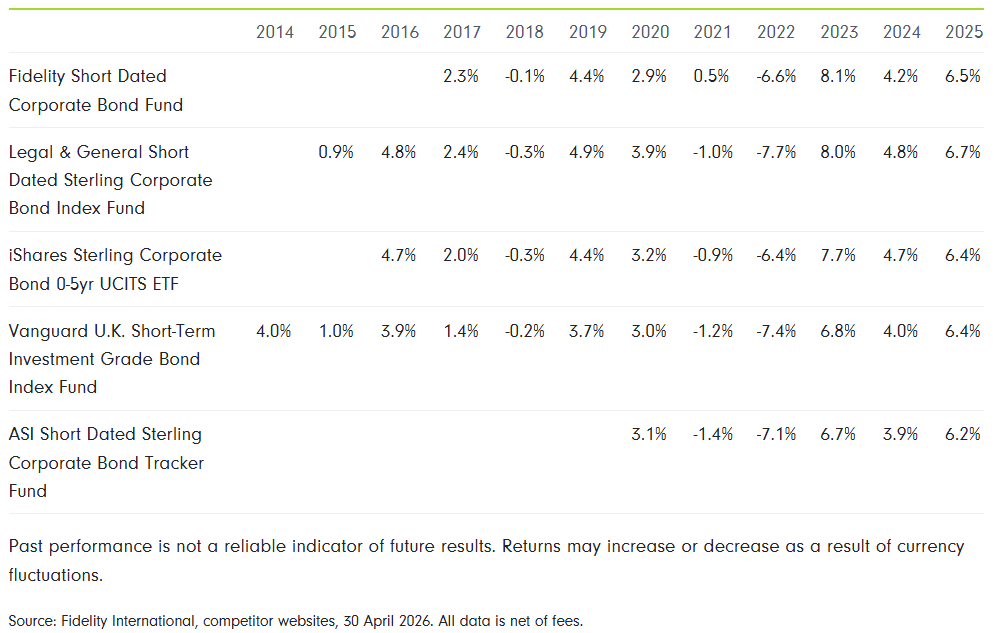

The Fund has generated attractive excess returns over index (after fees) since inception and is one of Fidelity’s lowest volatility bond funds.

The Fund has also delivered attractive outcomes relative to the passive community – outperforming each of the comparable passive funds over the last 5 years (after fees), with a lower volatility profile, lower maximum drawdown, and a more attractive Sharpe ratio.

Calendar year return tables

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. The writer’s views are their own and do not constitute financial advice.

This information should not be relied upon by retail clients or investment professionals. Reference to any particular investment does not constitute a recommendation to buy or sell the investment.

Main image: Background, swirl, richard-r-schunemann-3QsFMZLm_KU-unsplash