Just Group has called for greater scrutiny of the effectiveness of pension communications after FCA research revealed that women risk missing out in retirement due to poorer levels of engagement.

Figures from the FCA’s Financial Lives Survey showed a high proportion of people are not taking an interest in pension matters, with women (12%) less than half as likely as men (26%) to be highly engaged with their pensions.

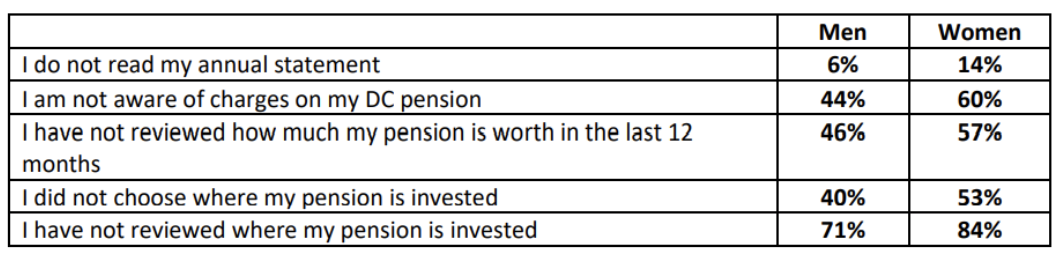

Women were also less likely to read their defined contribution pension statement than men, review the value of their pension pot or know about pension changes.

Stephen Lowe, group communications director, Just Group, said: “Sending out information is easy but the hard part is presenting it in a form that engages and informs a wide range of people. Most people say they do read their annual statement although the number who don’t is more than double that for women than men. Anything more complex – knowing what the charges are or whether they choose the investments – shows much lower levels of engagement, especially among women.”

Stephen Lowe, group communications director, Just Group, said: “Sending out information is easy but the hard part is presenting it in a form that engages and informs a wide range of people. Most people say they do read their annual statement although the number who don’t is more than double that for women than men. Anything more complex – knowing what the charges are or whether they choose the investments – shows much lower levels of engagement, especially among women.”

While developments such as automatic enrolment into workplace schemes and good quality default investment funds have made it possible to accumulate retirement savings without being engaged, Lowe warned that a passive approach does not work as people reach the point of needing to access their pension. Take-up of free, impartial advice from Pension Wise was found to be significantly lower among women than their male counterparts, with only one in 10 (12%) aware of the service.

Lowe explained: “The system works best where people who are engaged with their pensions have the freedom to make active decisions but those who are less interested are protected from harm. The current weak point is where defined contribution savers start to make decisions about how best to use their funds, at this point they are most vulnerable to poor choices and to falling for scams.”

Just Group has called upon the Department for Work and Pensions and the FCA to become far more “ambitious” with their interventions than they have been to date.

Lowe added: “Introducing wake-up packs at age 50 has not materially increased usage and the evidence from the stronger nudge trials shows implementing this intervention will not deliver the usage level to that which the government aspires.

“We need to plan to succeed, not plan to fail. An effective way to address this would be to automatically enrol people into pension guidance sessions, just as we do into workplace pensions. That way the least engaged, least knowledgeable and least confident are sure to receive the professional support of an expert to help talk through their options. They won’t even have to know such a service is available to still reap the benefits of it.”

FCA data on engagement with defined contribution contribution pensions