Increases in longevity in the UK mean that the risks are skewed towards us living longer, healthier lives. But too many of us are in cash to achieve a decent retirement pot. The problem is how to entice caution savers/investors into the equity market, to potentially improve their retirement income, says Carl Stick, Rathbone Income Fund Manager.

Risk and uncertainty are part and parcel of life. We are always thinking about odds of some sort. Is it going to rain today, and if so, should I take an umbrella? Should I play it safe and lay up short or be bold and go for the green at the 15th (huge congrats Rory McIlroy).

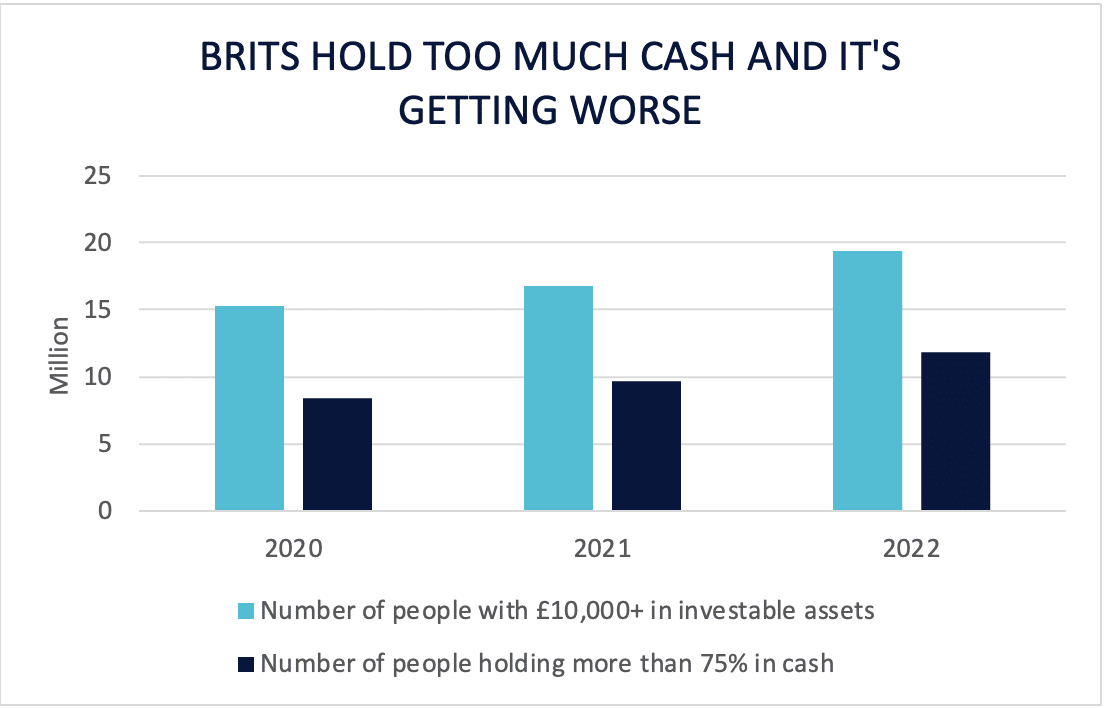

These risks and uncertainties can become overwhelming and, perhaps, paralysing when it comes to money. The Financial Conduct Authority (FCA) knows that Brits are simply not embracing risk as they should and that it increases the chances that many won’t have enough to fund the retirement they expect. Improving this take-up of risk is actually one of the FCA’s long-term goals. Unfortunately, it’s not going well. The number of people with more than £10,000 in investable assets increased by roughly 25% between 2020 and 2022 (the last update) to almost 20 million. Yet the number of people holding three-quarters or more of that money in cash is up 40%.

Source: FCA

The British public’s reluctance to invest will be no secret to you. Yet there’s a new aspect to this old problem: ‘money dysmorphia’ is how many are describing it. People who are objectively well-off financially are increasingly anxious about their finances. One survey of 2,000 people with more than £250,000 that could be invested showed 35% of men and 40% of women were worried about losing it. In reality, the bigger risk is arguably that people outlive their savings in retirement – unless there’s a sea change in risk appetite.

The pension ain’t what it used to be

When the modern UK pension was introduced in 1948 the cost wasn’t considered to be high. A three-stage life model was conceived: you were a child and went to school; you worked; and then you retired (at 60 for women and 65 for men). Yet, in 1948, life expectancy in the UK was 70 for women and 66 for men. For the average man, that meant paying in for almost 50 years and likely dying before receiving a penny. Meanwhile, the ratio of workers to pensioners was advantageous, people paid flat-rate contributions and received flat-rate benefits, making the pension model a one-size-fits all exercise. Obligations and benefits were static, and a predictable system worked in an unpredictable world – for a time.

Current life expectancy is 79 and 83 years for men and women respectively. That now means 13 years of payments for the average man after the current retirement age of 66 and 17 years for women. The longer we live, the greater the uncertainty, and the increasingly defunct the old three-stage system becomes. This has stretched the generosity of the state pension and transfers more responsibility to each of us to fund our retirement.

London Business School economics professor Andrew Scott, in his book The Longevity Imperative, argues that we must chew over some knotty financial questions. If our working lives are increasingly episodic, we must decide when and how much to save, to borrow, and to spend. We must cope with increasing uncertainty. Scott cites a World Economic Forum report on six major economies which worryingly suggests that the typical individual will outlive their savings by between eight and 20 years. The risk of our wealth running out is clear and present:

Source: World Economic Forum Analysis

Spending and saving decisions are influenced by a cascade of ‘risky’ decisions. When do you stop working? Having stopped working, how much money do you think you will need to maintain an appropriate standard of living? Even if you know how much you may want to spend and how comfortable you want your lifestyle to be, you don’t know how long this expenditure will last – how long you live will define how much you spend. And even if you correctly guesstimate your lifespan, your health span could be very different, which impacts both your earning power while in work and what you may need to spend in retirement. And having thrown all this into the melting pot, you then need to decide how much risk you want to take with your hard-earned wealth – cash saved at the risk-free rate or invested at higher risk to consider the greater uncertainties of life. Pension planning is a complex unknowable game of risk and traditional thinking is inadequate.

We’re back where we were before: people worried about their future and instinctively reducing risk with their finances. Advice is crucial to explaining the risks that clients cannot see and encouraging them to increase risk and therefore their expected returns.

Equity income to the rescue?

Financial advisers are well positioned to encourage people to take more risk to ensure they can achieve their goals and retire comfortably. People’s decisions to spend, save or invest are established upon unknowable outcomes – but it’s this uncertainty that, paradoxically, demands a greater role for equity investment, we believe. Because increases in longevity mean that the risks are skewed towards living longer, healthier lives. Although we cannot know the future, the assumption must be that we will need to finance longer lives. And that means either working longer, spending less, or generating greater investment returns. We think investment probably needs to start sooner rather than later, as well, to mitigate downside risk and maximise the compounding power of investment.

Our focus, as income fund managers, is to create a solid, dependable and growing income stream that advisers and their clients can rely on, both for accumulating their wealth and when decumulating assets later in life. Done right, this should mitigate the need to draw down capital at retirement, which can drastically reduce retirees’ wealth, especially during market sell-offs.

That lets advisers focus on mitigating the other unknowns facing their clients and should help them encourage clients to take the risk required to get them to the futures they seek.

Mian image: edge2edge-media-uKlneQRwaxY-unsplash