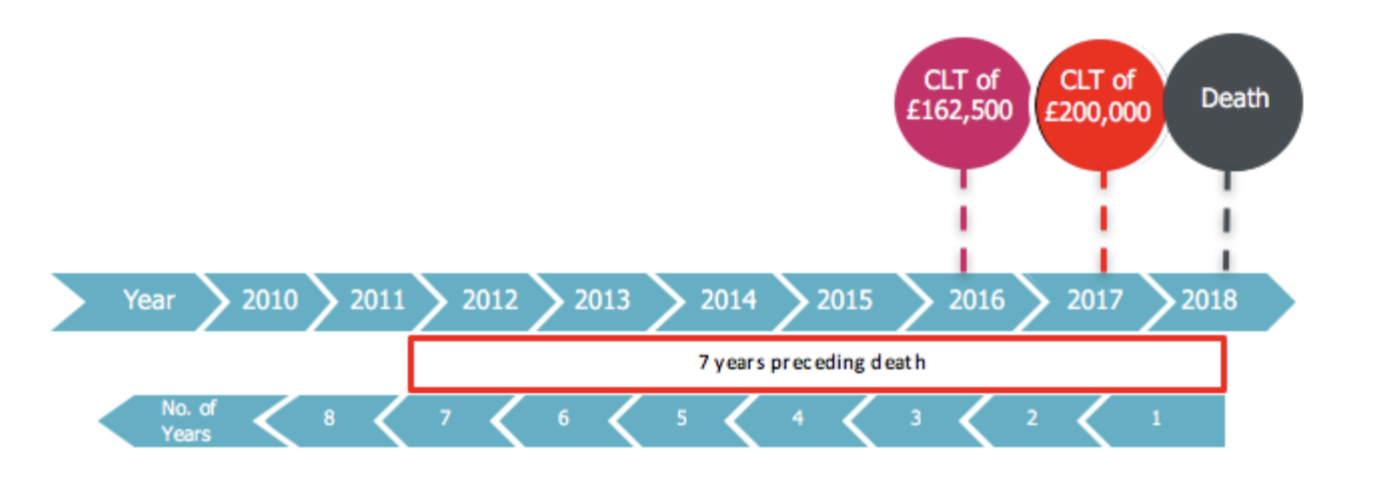

Example 3b – CLTs and death within 7 years

Amy gifts £162,500 to a discretionary trust

The following year, Amy gifts £200,000 to another discretionary trust Amy dies a year after creating the second discretionary trust

* The timeline above shows that both CLTs are in the 7 years preceding death. The first CLT has already used £162,500 of the nil rate band. The second CLT has used the remaining £162,500 of the nil rate band and there was an entry charge on £37,500 of the £200,000 gift at the rate of 20% (half the death rate). See however ‘grossing up’ comments above.

* On death, the IHT due on the CLT is recalculated at the rate of 40% (full death rate). The tax will be calculated at 40% on the £37,500 over the nil rate band. The tax already paid at 20%, for the entry charge, can be deducted from this and only the difference will be payable. It is important to note that the nil rate band at the time of death will apply and if the CLT was made more than 3 years prior to death, taper relief can be applied. If the IHT calculated on death is less than the tax already paid as an entry charge, there will be no refund of the tax paid.

How PETs & CLTs interact with each other

Order of trusts

If an individual is considering using a combination of different types of trust, the order in which the trusts are created should be taken into account.

If a loan trust is being used, this would normally be set up first. This is due to the fact that the settlor lends the money to set up the trust and as it is not a gift, it is neither a PET or a CLT. This will, therefore, have no impact on subsequent gifts.

For gifts made at the same time, usual planning would be to consider making CLTs before PETs. If done in this order, there is no risk of a “failed PET” reducing the nil rate band available throughout the lifetime of the trust created by the CLT.

PETs before CLTs

There are two issues to consider – entry charge on lifetime gifts into trust and impact of death.

Lifetime gifts

CLTs accumulated in the 7 years leading up to the start date of a lifetime discretionary trust are included to determine if an entry charge applies. PETs have no impact on this accumulation.

Impact of death

If, in a 7 year period, the individual makes a PET, then a CLT and subsequently dies, the PET will become a “chargeable transfer” (or “failed PET). Both the “failed PET” and the CLT will be included in the IHT calculation of the individual.

In addition, if a PET has been made in the 7 years leading up to the trust creation, and subsequently “fails’, becoming chargeable, this causes an impact to the trust when assessing for periodic charges.

This is because the nil rate band available to the trust at the 10 year point is by reference to chargeable transfers in the 7 years prior to the trust creation. The nil rate band is reduced by the amount of “failed PETs” and so there will be less nil rate band to set against the trust fund value in the 10 year assessment.

CLTs before PETs

Again, there are two issues to consider – lifetime gifts and impact of death.

Lifetime gifts

During lifetime CLTs have no impact as PETs do not become chargeable unless the individual dies within 7 years of making them.

Impact of death On estate

When calculating the IHT payable by the estate, “failed” (or chargeable) PETs and CLTs made in the 7 years before death are included.

On gifts

The 14 year rule applies where there are CLTs in the 7 years before a PET which has “failed”. This rule is there to ensure that gifts which become chargeable are taxed appropriately.

To work out if tax is payable on a gift, the law says that it must be added to any chargeable gifts made in the 7 years before the gift concerned.

* A ‘chargeable gift’ is a gift which is not fully exempt.

* A PET is potentially exempt and only becomes fully exempt if the individual who made it survives for 7 years.

As gifts are placed in the order they were made, starting with the oldest and moving towards the date of death. CLTs made in the 7 years before the “failed” PET will use nil rate band first, meaning that there could be more IHT due than anticipated on the “failed” PET.

Example of the 14 year rule

Amy gifts £275,000 to a discretionary trust 12 years and 2 months ago

6.5 years later, Amy gifts £500,000 to her son Peter

Lifetime gifts

Total gifts equal £775,000

The gifts are a mixture of PETs and CLTs, so the interaction between the two will need to be considered.

The first gift was a CLT of £275,000 (assume that the nil rate band was £275,000). There were no previous CLTs so, there was no entry charge.

The second gift was a PET of £500,000. Unlimited amounts can be given as PETs and provided Amy lives for 7 years there will be no IHT consequences. The previous CLT has no bearing on the PET whilst Amy is alive.

The gifts were made 6.5 years apart.

Impact of death

[continued on next page]