As the end of the tax year approaches, many investors are reviewing their portfolios and considering how best to maximise their ISA allowances. While the temptation to stick with past winners like US equities may be strong, growing concerns over a potential US recession and the recent underperformance of the S&P 500 highlights the significant risks of overexposure to a single market.

In recent years, the US market has been driven by a handful of technology stocks, creating a market heavily reliant on a single sector. But as market conditions have shifted and with increasing geopolitical uncertainties, cracks in the dominance of US equities are becoming apparent.

Many investors may not even realise they are heavily concentrated in the US. With global indices like the MSCI World weighted heavily towards US equities, particularly large-cap tech stocks, portfolios that track benchmarks often carry significant exposure to one region. This unconscious concentration increases vulnerability in market downturns and limits participation in growth opportunities outside the US.

Fidelity International highlights how diversification – spreading investments across regions and asset classes – is a crucial strategy to building resilience and managing risk.

The case for diversification

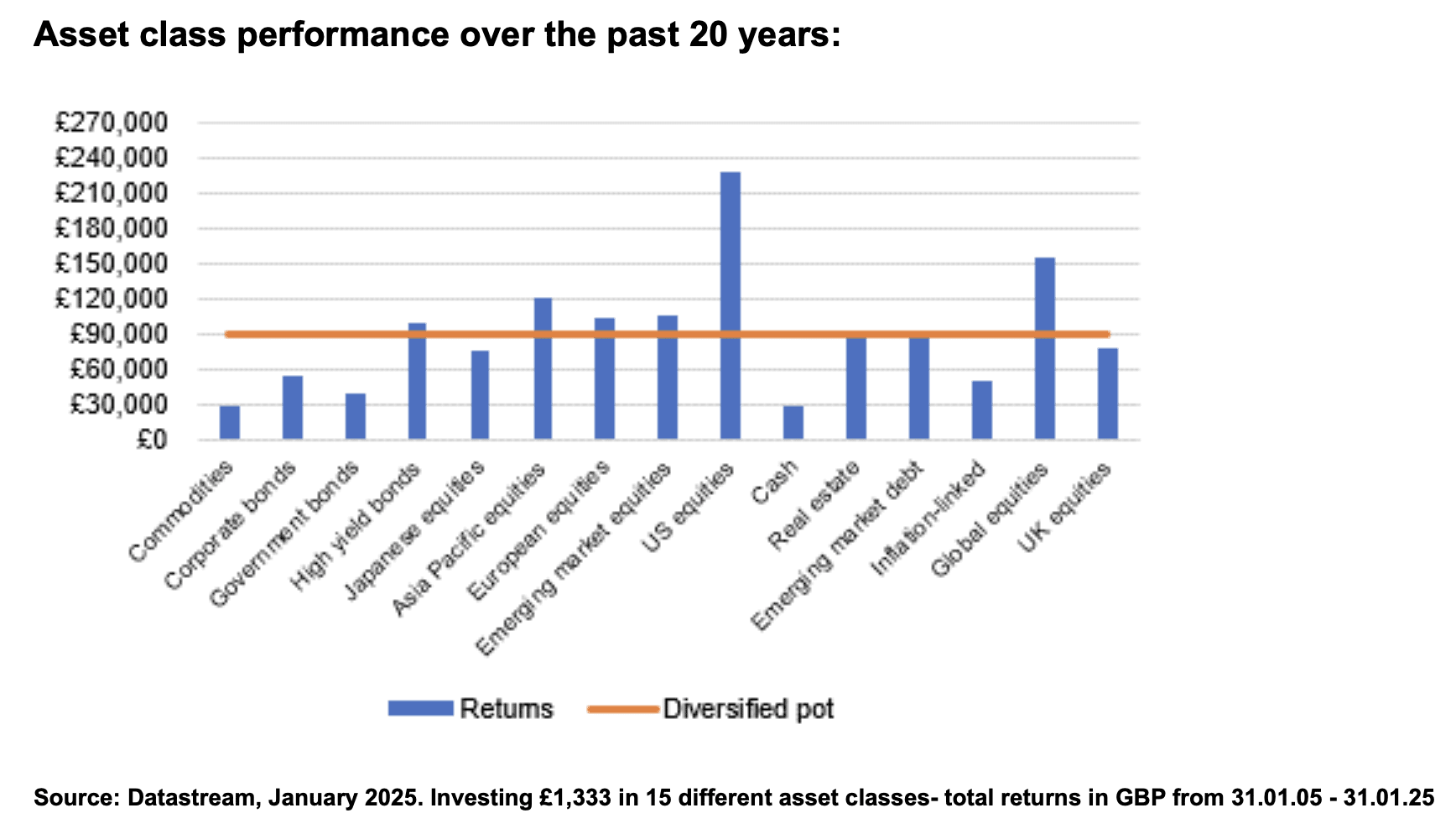

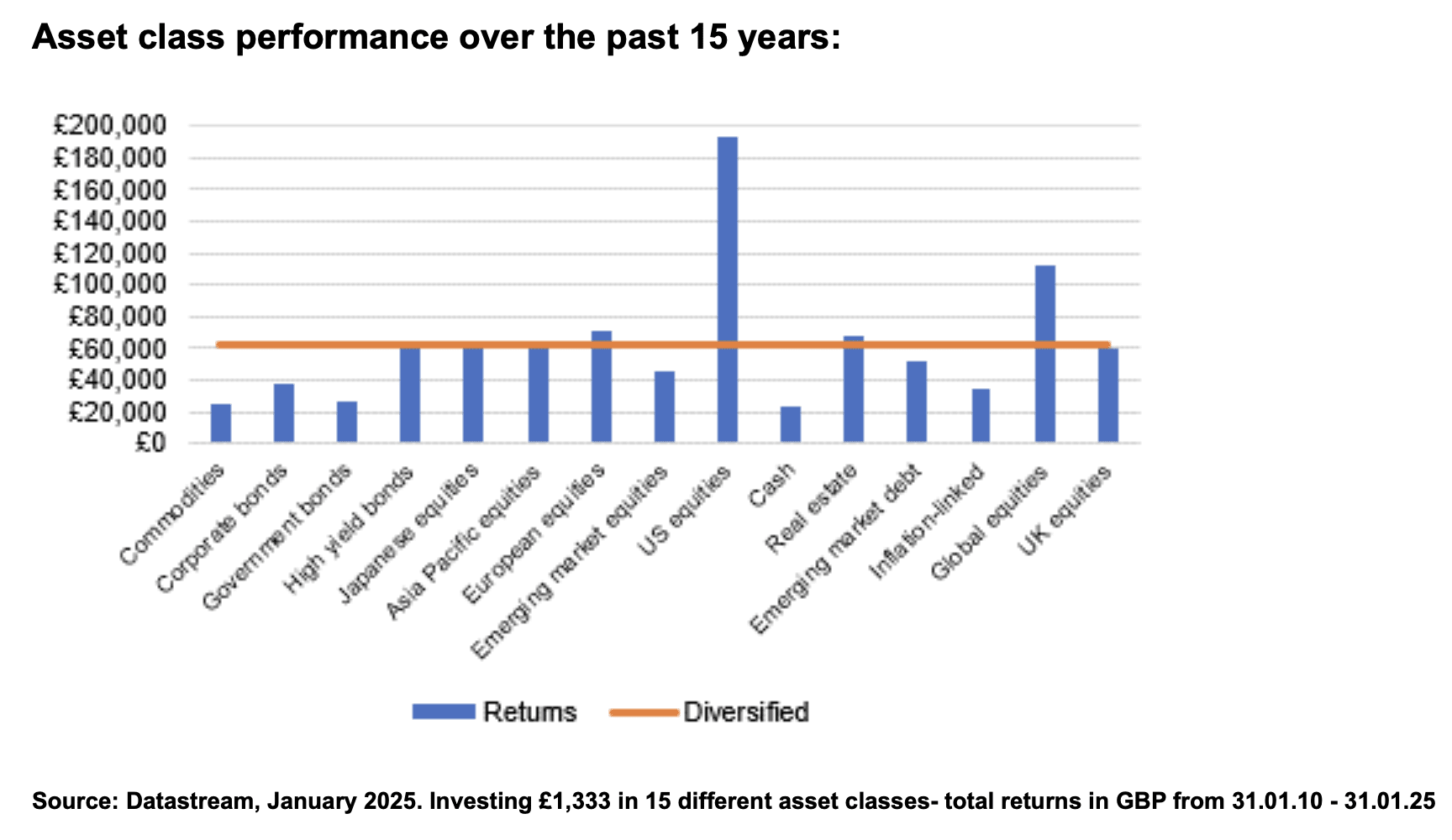

Fidelity examined the performance of two investment strategies over five, 15 and 20 years, comparing a concentrated approach – investing £20,000 in a single asset class, with a diversified portfolio – splitting that £20,000 and allocating £1,333 to 15 different asset classes.

Historical performance highlights the challenges of predicting which asset class will lead in the future. For example, over a 20-year period, US equities delivered outstanding growth, turning £20,000 into £229,484, while commodities underperformed, returning just £29,400. The range of returns is large – and unforeseeable at the time of investment.

The diversified portfolio achieved £89,995 over the same period. Although it was outperformed by some individual asset classes, notably US and global shares, it offered stability, beating nine out of the 15 analysed asset classes, including cash (£30,071) and government bonds (£39,009). This consistency underscores how diversification can protect against underperformance, while still participating in growth opportunities. Meanwhile, focusing solely on recent top-performers exposes investors to significant risks if markets shift.

Over a 15-year period, Japanese equities (£64,329) and real estate (£67,313) outperformed the diversified portfolio (£62,143). Yet these gains were cyclical, with Japanese equities underperforming over 20 years (£76,282 vs £89,995) revealing the unpredictable nature of markets and the risks of relying too heavily on individual asset classes.

In the shorter five-year timeframe, the benefits of diversification remain evident. Commodities performed well, with returns of £33,028, but their longer-term performance lagged significantly, and they were the one of the worst-performing asset class over 15 years (£24,706 vs £62,143) and 20 years (£29,400 vs £89,995).

Tom Stevenson, Investment Director, Fidelity International, comments: “Would investors have been better off simply putting all their money into US equities? In hindsight, yes. But to have done so 20 years ago would have required the kind of foresight that investors do not enjoy. The longer I study financial markets, the more I understand how little we really know about the future. As investors, we don’t have a crystal ball – we don’t know what’s going to happen and we don’t know how investors will react to what does unfold.

“Take the last five years as an example: we’ve experienced a pandemic, wars in Europe and the Middle East, the worst inflationary spike since the 1970s and a dramatic rise in interest rates after a prolonged period of cheap money. Despite all this, US equity investors have been handsomely rewarded thanks to the dominance of technology companies and the market’s recent love affair with AI. However, recent developments – including the underperformance of the S&P 500 and growing fears of a US recession – are a stark reminder that no market dominance lasts forever.

“Our analysis reveals that over five, 15 and 20 years, US equities have consistently outperformed a diversified portfolio. However, valuations in the US today are relatively expensive and returns have been driven by a small handful of stocks, meaning the S&P 500 index comes with a high degree of sector risk.

“Will US equities outperform for the next five, 15 and 20 years? And, in particular, will the US market continue to be dominated by a small handful of large technology stocks? No-one knows; the future is uncertain. Faced with this uncertainty, what can we do? First, we can avoid making big bets on regions, sectors, or asset classes. Yes, we can kid ourselves we saw the winners ahead of time. More likely, we got lucky. The cure for the absence of foresight is diversification. We can’t always anticipate the next big trend, and that’s why spreading investments across a range of asset classes provides resilience, balances risk and ensures we’re not overly reliant on a single sector or theme.

“As we approach the tax year-end, now is the perfect time to review your portfolio and ensure your investments are working towards your long-term goals. A diversified ISA not only mitigates risk but helps you stay resilient through market cycles, allowing you to be invested confidently in what matters most.”

Main image: john-bakator-iQOzInmMxEY-unsplash