Fidelity International’s Multi-Asset team has published their latest views on which asset classes and markets are presenting the greatest opportunities and risks, and this article zooms in on the key take aways.

To download Fidelity International’s full Global Asset Allocation Insights for June 2026: Global Asset Allocation Insights – June 2026

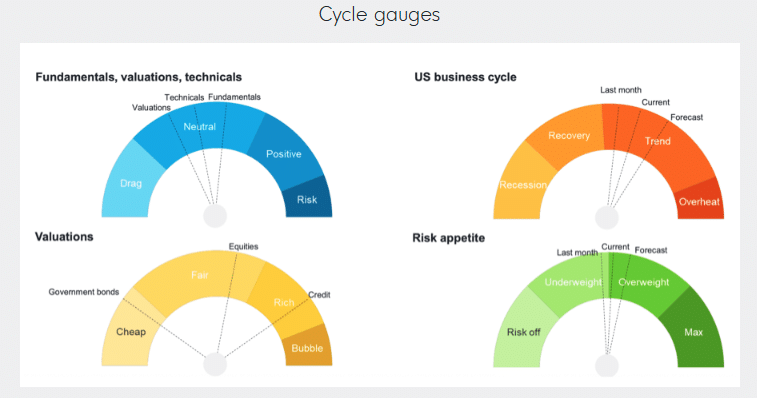

The key insights:

What has changed?

- Energy shock feeding into the macro backdrop: Higher oil prices are beginning to tighten financial conditions and add to inflation pressures, particularly across Europe and parts of Asia.

- Move underweight European equities: Energy vulnerability, weaker earnings momentum, and rising external risks lead us to a more cautious view of European equities despite improving fiscal support.

What has stayed the same?

- Markets looking through the conflict: The global economy still showing strength and investors are focusing on resilient growth and earnings fundamentals as expectations shift towards a messy resolution rather than continued escalation.

- Macro divergence across regions is increasing: Commodity exporters and more energy-independent economies are proving relatively resilient, while energy importers are facing a more difficult inflation-growth trade-off.

What are we watching?

- Energy market and supply disruption: The duration and severity of the shock will be key for inflation, growth, and central bank expectations.

- Signs of macro slowdown emerging in the data: Whether higher energy prices begin to weigh more materially on consumer demand, margins, and business confidence.

- Durability of broadening earnings growth: Whether earnings momentum can continue broadening beyond US mega-cap technology into other regions and sectors, alongside potential high-profile IPOs this year and their impact on sentiment.

Best ideas for investment outcomes

Growth

- Japan and EM equities preferred, particularly Korea, South Africa, and Brazil, supported by structural tailwinds, earnings momentum, and attractive valuations.

- Thematic equities related to the grid upgrade benefit from idiosyncratic return drivers as the US and EU look to accommodate greater demand and more renewable energy.

Income

- Emerging market bonds in select local markets continue to look attractive given elevated yields and commodity-exporting fundamentals.

- Quality income equities provide relative defensiveness and stability, particularly in an environment of higher uncertainty. Dividend growth and strong balance sheets remain key filters.

Capital preservation

- Commodities, particularly energy exposure, have proven to be the most effective hedge in the current environment, providing protection against geopolitical risk and inflation.

- Gold remains a medium-term diversifier, however its behaviour has been less consistent as a hedge during the recent volatility.

- We remain positive on selected real assets, particularly transition materials such as copper, supported by structural demand from electrification, reshoring, and AI demand.

Uncorrelated returns

- Absolute return strategies, driven by active investment decisions and incorporating idiosyncratic sources of risk – particularly those with a focus on tail risk mitigation.

Source: Fidelity International, May 2026. Views reflect a typical time horizon of 12–18 months and provide a broad starting point for asset allocation decisions. However, they do not reflect current positions for investment strategies, which will be implemented according to specific objectives and parameters.

Main image: graphs, jakub-zerdzicki-9PwLeZA-RGc-unsplash