For professional advisers and paraplanners only. Not to be relied upon by retail investors.

John Calverley, chief economist of investment support firm Tricio Investment Advisors, looks at investing in the post-Brexit, post pandemic environment, with particular focus on the positioning of portfolios.

With the taming of Covid in sight (we all hope) and with Britain’s final departure from the Europe Single Market now behind us, how should we position portfolios? The US business cycle is always my starting point. China is becoming increasingly important for the world economy but the US cycle still dominates. The good news is that the Covid recession is likely ushering in a new economic upswing which should last a while.

US economic upswings typically last 7-10 years and see a prolonged rise in stock markets. So, the background for investing in risk assets today is supportive, although with two important caveats. First, US stock markets today are already on high valuations. Those valuations can be justified by low interest rates but low rates may not last. Indeed bond yields have already started to rise, causing volatility in markets. Secondly, and related, there are reasons for worrying that this upswing could see rising inflation, something that has been largely missing in the two upswings so far this century.

The impact of Covid

But can we totally ignore Covid-19 now? There is a very good chance that Covid is completely tamed over the next year, with the help of vaccinations and better treatments. We might still wear masks in crowded places, need tests for some activities and require booster shots. But social and business life will most likely resume as before, without needing social distancing or periodic distancing. This is what’s happened after all pandemics in history, with cities resuming their buzz and people soon forgetting the trauma. For stocks this suggests we will continue to see a rotation into cyclical and recovery stocks and away from the Covid-safety shares, particularly technology.

However, there is still a residual chance that Covid variants defeat these hopes, requiring continued social distancing and perhaps periodic lockdowns into 2022 and beyond. That would leave those same recovery stocks vulnerable. Some companies that have hung on for the last year despite social distancing requirements and periodic business closures and with the help of government support, may not survive another year of limited stop-start trading. This risk is still holding some of these stocks back, despite gains in recent weeks.

The impact of Brexit

What of Brexit? The deal agreed finally in December was a ‘hard Brexit’. It prioritised sovereignty for the British parliament – the freedom for the UK to choose its own rules – at the expense of significant new barriers to trade. While the interests of major manufacturers such as in the car and aero-space industries were looked after, small companies face new difficulties in exporting. Meanwhile service industries such as finance, business services, media and fashion, all big exporters and employers, face restrictions on operating in the EU which will drag some companies and jobs onto the Continent. It is still too early to say how far this will go. Indeed negotiations on some of these sectors are not finished yet. But it will be a drag, particularly on London.

The bottom line is that there is a hit to the UK economy while some companies, mainly small and medium sized, will need to change their business models. Estimates suggest the overall effect of Brexit is to lower GDP by 3-4% in 2030 compared to what it otherwise would have been (starting from 2016). The effect could be greater if immigration is severely restricted though early indications are that policy will still permit substantial immigration, though less freely from the EU.

A hit to GDP of 3-4% is not huge and indeed is dwarfed by the effects of Covid. Moreover, some of that was already taken in 2017-19 when the British economy grew only slowly despite very strong growth internationally. UK investment stagnated in those years just as US investment surged. The bottom line is that the UK will muddle through and as uncertainty lifts, business confidence and market sentiment should improve.

Looking at valuations

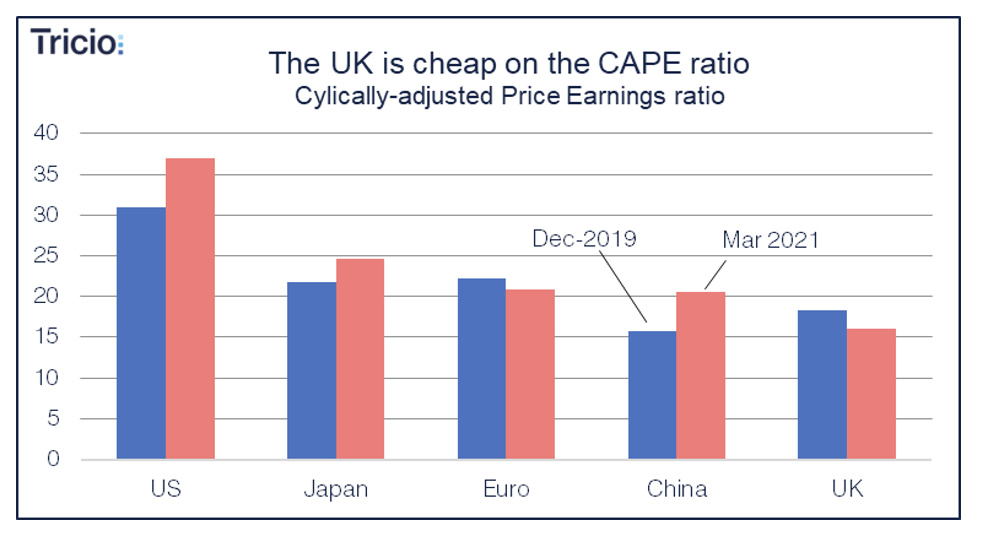

This brings me to valuations. As already noted, the valuations on US stocks are high. The cyclically adjusted price earnings ratio (CAPE, which compares the current index price with the last 10 years of earnings to smooth out the earnings cycle) is about 37 times, the highest it has ever been except in 1999-2000 during the first technology bubble. While this level can be justified by low interest rates, rates are rising now and if Covid is defeated as expected, US 10 year yields are likely to move into the 2-3% range before long. We continue to underweight bonds in our asset allocations. In contrast, valuations on UK stocks are very modest and indeed lower than at end-2019. In our asset allocation models we are overweighting UK stocks both large and small and also US small cap stocks which have lagged larger stocks.

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. John’s views are his own and do not constitute financial advice.