Ella Pumford, content manager at St. Modwen Homes, explores the options for buying a house, what schemes may be used and if there is a best time to buy.

Buying a home is one of the biggest investments we make in our lives. However, while the average house price in the UK is valued at £249,633, the cost of mortgages among other factors means that the total cost of the home-buying process can vary between individuals.

Even then, house prices continue to rise year on year. At time of writing, in England, house prices have increased by 7.6% in the past year. Competition spurred on by the housing crisis may mean that this increase is set to continue. This raises the question: when is the best time to buy?

‘Immediately’ is not always the answer. The true cost of a house will depend on your personal finances at time of purchase, and it can vary depending on which financial schemes are used to help. Jumping into a sale too soon can cost more than it’s worth.

Government schemes

On 3 March 2021, Rishi Sunak unveiled his latest budgetary plan for the nation. Included in this were schemes for home buyers which may make the process of climbing the property ladder easier for many people.

Stamp Duty holiday extension

The Stamp Duty holiday extension reduces the tax paid when buying properties. Under this scheme, homebuyers will only pay stamp duty on properties above the value of £500,000. This scheme was set to end on 31 March 2021. However, the Government has extended this until 30 June 2021.

Buying a property within this timeframe could save homebuyers up to £15,000 before the tax break ends.

The sale of properties must be completed before the 30 June deadline. However, the opportunity to save on Stamp Duty could be extended based on buying choices.

As a national housebuilder, St. Modwen Homes has its own Stamp Duty holiday extension which is available on a selected number of homes until 30 September 2021 and buying a new build property can help save thousands beyond the Government’s June deadline in many other locations. The housebuilder has also launched a new ‘Mortgage Paid’ offer for those buying a new-build home. Available on selected homes at developments across the country, the company will essentially pay up to six months of the mortgage. The offer is only available for a limited time, but being six months mortgage free could save thousands.

5% mortgage deposit

A new mortgage scheme has enabled lenders to offer mortgages to more homebuyers with lower deposits from April 2021. The Government-backed 95% loan-to-value mortgage scheme means that first-time buyers and current homeowners will be able to purchase a home with just a 5% deposit.

The scheme will run until December 2022. So, for buyers wanting to take advantage of this new offer, applying for a mortgage before this deadline may be the best time to buy. A lower deposit means that they will have more money in their pocket on moving day to help furnish your new home, or some extra cash to save for a rainy day.

The scheme is similar to the Help to Buy: Equity Loan which is solely available for first-time buyers who are buying a new-build home.

First-time buyer?

As mentioned above, it’s now easier for first-time buyers to get onto the property ladder with help from the Government-backed Help to Buy: Equity Loan scheme. Similar to the 95% LTV mortgage scheme, first-time buyers can also use a 5% deposit to buy their home.

The key difference with the Help to Buy scheme is in eligibility and how the finances are organised.

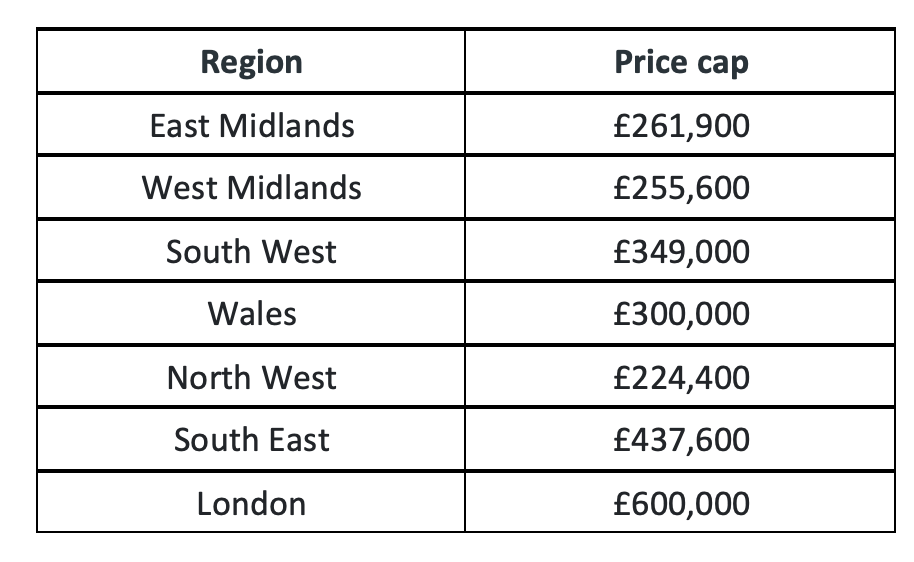

Firstly, the individual must be a first-time buyer and be buying a new-build home, and they will need a 5% deposit of the value of the property. The Government will provide an equity loan of up to 20% of the property value (or 40% in London), which is interest-free for the first five years. This means the buyer will only need to borrow 75% of the property value from a mortgage lender.

The total value of the property is capped depending on the location but they will likely be above a first-time buyer’s budget. The regional caps range from £261,900 to £600,000:

This scheme runs between April 2021 and March 2023.

Best time to save

If it’s not looking like the best time to buy right now, it’s always the right time to save. For those buying their first home, Help to Buy schemes along with various ISAs mean that individuals can prepare for their homebuying journey.

Unfortunately, Help to Buy ISA are no longer available but those with existing accounts can continue to deposit up to £200 each month. For first home buyers, the Government will top up money savings into the scheme by 25%. Up to £12,000 can be saved, receiving an extra £3,000 from the government. This incentive is valid until until November 2029 to save and until November 2030 to claim the 25% bonus.

Another scheme that is open to new savers is the Lifetime ISA allowance scheme. Up to £4,000 can be saved into the ISA each year and the Government will top it up by 25% at the end of the tax year.

This isn’t a scheme for those looking to buy a home in the short term. The money must be in the account for at least one year. The money must also be used to buy a first home, otherwise, the funds are available to withdraw at age 60 and over. A 20% fee is charged for withdrawals of money before age 60.

Remember, the higher the mortgage deposit, the lower the loan amount and, therefore, the lower the repayments.

It can be argued that this is an exciting time for those who are buying a home — especially for first-time buyers. New schemes mean that those with a proactive nose to hunt out the best deals can save thousands when they buy a home. But ultimately, there’s no set date for the best time to buy.

The new buying schemes will be useful for those looking to buy their home in the near future as thousands of pounds can be saved. But those who are planning ahead should aim to save as much as possible before they buy their home, as in the long term, larger deposits make the mortgage application and mortgage repayments easier.