Dan Atkinson, head of Technical at Paradigm Norton Financial Planning, explores how our personal experience of money shapes our relationship with it – our money story – and how we can deal with a clash between advice logic and client actions

Have you ever picked up a client file and just been baffled? Why on earth would they do ‘that’? You pick it up again and ask yourself what were they thinking when they decided to take that action? In your eyes there is no logic, reason, or rationale. What on earth were they thinking!

An important lesson to learn is that most people, most of the time, do make sense – to themselves. The challenge for us is to understand their money story.

What do I mean by a money story? Everyone has their own view on the world and understanding of how money works. This is formed in part by upbringing (either to conform to it or rally against it) and in part by how money has touched our lives. These teach us very different lessons and the lessons we experience are far more powerful than those we read in a book.

In The Psychology of Money, Morgan Housel highlights that our personal experiences of money represent just c0.00000001% of what has actually happened in the world. Yet we use our experiences to form c80% of our understanding of money. Some of the experiences which shape our understanding of money might include:

- How we were taught about money growing up

- How affluent or indebted our parents were

- The local economy where we grew up and where we now live

- What work was like for our parents and our working life so far

- Our experience of inflation and investment returns

- And (to an extent) sheer luck!

With a great diversity of experiences, it is not surprising that our money stories can differ widely. If we can start to understand someone’s money story their decisions won’t seem as crazy as you think!

We, as paraplanners, are not exempt from the influence of money stories. As well as needing to consider our clients’ money story we need to be aware of our own story (and sometimes the advisers’ we work with!). Understanding the differences will help us communicate better with our clients and enable them to make good, well informed decisions.

To help us understand, let me share how inflation is written into my money story.

Inflation in my money story

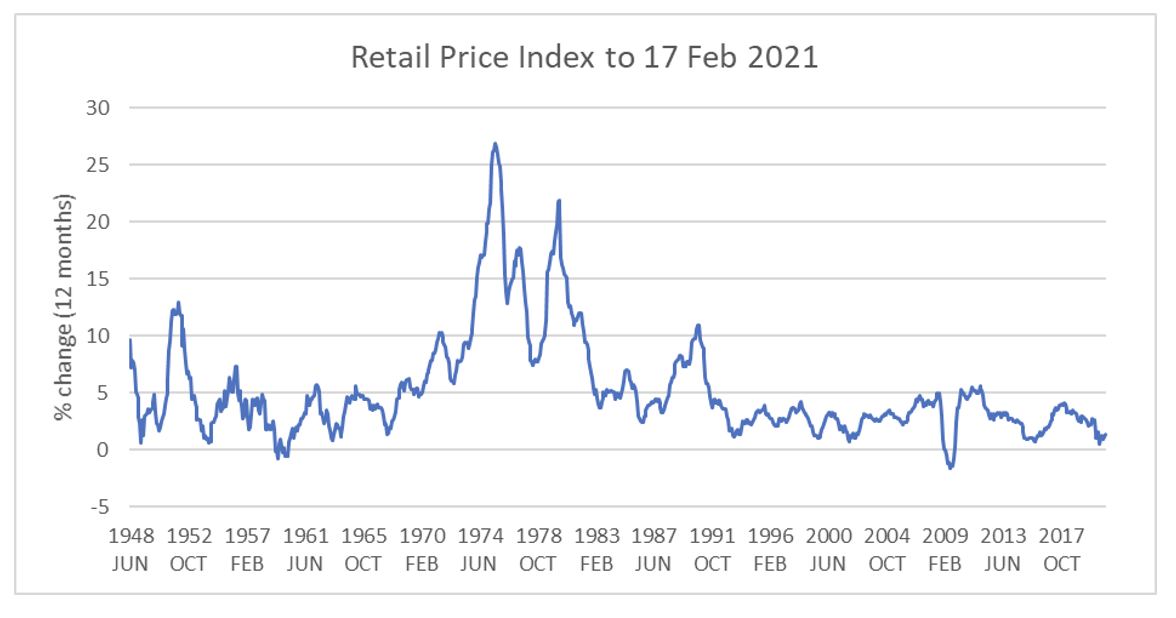

Whilst it’s not an ‘official’ national statistic anymore, the Retail Price Index is a helpful measure of inflation going back to just after World War 2. You can access it on the Office of National Statistics website https://www.ons.gov.uk/economy/inflationandpriceindices/timeseries/czbh/mm23. As we know, inflation is important because (if it goes up) it increases the amount of money needed to fund the lifestyle we desire. Our personal rate of inflation will differ from this headline rate because the goods and services we buy are likely to differ from the ‘basket’.

Since I joined the profession, I’ve seen headline inflation peak at just over 5% and fall below -1%. Over the last decade RPI inflation has averaged around 2.7% p.a. Inflation being around this level is a part of my money story. It’s not been a huge concern at this stage in my career – other than the inevitable train travel season ticket price reviews (which have not solely been upward I might add! Check out the ORR data https://dataportal.orr.gov.uk/media/1736/rail-fares-index-january-2020.pdf).

However, this isn’t necessarily the experience of all the people we work with and the clients we serve. Take a look at the chart below of changes in the Retail Price Index.

If my money story accounted for inflation in the 1970s I would have a very different view. That decade saw average inflation around 13% p.a. peaking at c27%. If my money story had that chapter of rapidly rising prices in it I would likely be concerned about the impact of inflation on achieving my financial planning goals.

The interesting thing is that I know that inflation can be much higher than at present. I’ve even looked at the data going back to 1210 from the Bank of England (https://www.bankofengland.co.uk/-/media/boe/files/statistics/research-datasets/a-millennium-of-macroeconomic-data-for-the-uk.xlsx?la=en&hash=73ABBFB603A709FEEB1FD349B1C61F11527F1DE4) which shows inflation as high as c50% when the Magna Carta was reaffirmed (for the third time in return for a property tax) and as c-30% when Queen Elizabeth I took the throne!

But my money story shouts louder than this empirical data. It affects the way I behave and make decisions. Kept unchecked a lack of respect for inflation could come back to bite me in the future.

Dealing with a clash of money story

So, what happens when our money story – as perceived by us, the adviser, our firm – clashes with the client’s money story? What should we do?

Last year I received an interesting piece of advice – don’t throw a fact bomb on an emotional fire. It’s tempting to find some data which agrees with your point, but if we don’t communicate with empathy at best it will be ignored and at worst it will antagonise.

I think there are three helpful things we can do:

- Check your ego at the door. You might be factually right, but the important thing is to enable the client to make an informed decision. Focus on that outcome – not making ‘you’ look clever…

- Look at your own money story in the mirror. Are there aspects of your perception of the world which are not aligned with the big picture? These might be clouding our reasoning and understanding. Pay particular attention to the differences in your money story and the client’s.

- Be humble and honest. If you are right (and you could be wrong!), don’t forget that the objective is to enable the client to make an informed decision – not to make them feel inferior or in any way inadequate as a result of their money story. If you need to help them broaden their money story, be open about it, but build on their current one – don’t dictate a complete rewrite. Enable them to make good, well informed decisions by being their partner, not their schoolteacher.

So, the next time you open a file and think ‘what were they thinking!’ (or perhaps have a conversation with a colleague), take some time to understand what they are thinking. Is this a clash of money story and how might you address it?

This article was first published in the April 2021 issue of Professional Paraplanner.