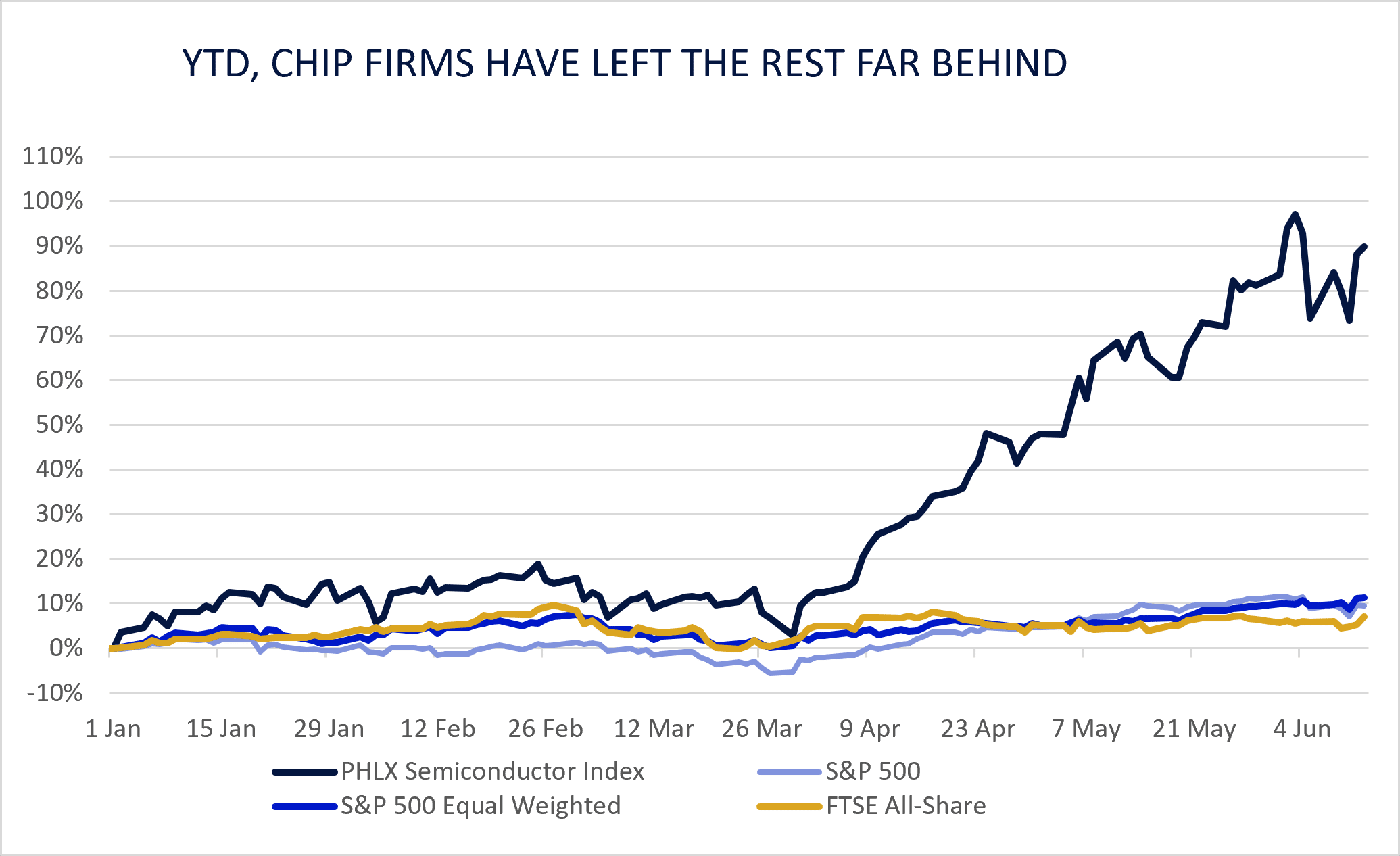

Stock markets have done pretty well so far this year. But in reality, the rally has been overwhelmingly driven by a handful of mega-cap hyperscalers and AI enablers – the companies building and powering the vast data centres that underpin this technological revolution.

But after a wild week or so in early June, that narrative has flipped: the darlings stumbled while the rest of the market perked up. Could momentum be starting to turn the other way?

We own many of these AI and AI-enabling companies. High-end chip designer Nvidia, search and AI giant Alphabet, e-commerce and data behemoth Amazon, chipmaking technology suppliers ASML and ASM International, and chip factory TSMC.

We also own stocks outside the tech sector that are making heaps of hay from supplying the concrete roots for the cloud: heavy machinery maker Caterpillar, data centre developer Equinix, and cabling and sensors manufacturer Amphenol, among others.

We were underweight the CPU end of the computer chip market, which did extremely well in 2025 and year to date, after generally lagging for several years as the world fell in love with GPUs. That’s been a stiff headwind.

Source: FactSet; 31 Dec 2025 to 12 Jun 2026, GBP total return

Adding cyclical exposure – with an exit route

To try to balance this, we’ve bought two passive ETFs: the Franklin Templeton FTSE Korea and iShares MSCI Global Semiconductors.

The companies in these indices are extremely cyclical – their fortunes ebb and flow with the broader economic cycle – and therefore not typically regarded as ‘quality’ businesses, which are our usual hunting ground.

We believe this approach gives us exposure to a part of the market that’s been powering ahead while also retaining the flexibility to swiftly exit if conditions change.

ETFs are liquid and can be sold at a moment’s notice, which is important when you’re buying into areas that could be very volatile (both up and down).

Think of it as renting rather than buying: we get the benefit of the neighbourhood without committing to the mortgage.

Meanwhile, we sold our holding in business consultancy Accenture. The business has been under great strain from AI threats.

While the business has actually managed to deliver growth in sales and earnings, the risks surrounding its future have grown markedly.

We swapped our North American insurance broker, Brown & Brown, for Marsh & McLennan, the world’s largest insurance broker. Brokerage companies have had a hard time in the past year or so since we bought Brown & Brown. The ubiquitous AI concerns are relevant here as well.

We still believe that a more complex and harder insurance landscape should lead to more business for brokers.

Even if insurers themselves were squeezed both by having to price risk more keenly to win business and by the rising cost of honouring claims, the broker takes a percentage with less risk. We swapped to Marsh because its valuation was much more attractive relative to Brown & Brown for a much larger and more dominant business.

One stock we have brought on from our bench is Arista Networks. This business is a specialist in building ultra-fast and low-latency networks for big data centres and cloud computing.

It designs the high-speed networking switches that sit at the heart of modern data centres, with hyperscalers and large enterprises among its main customers.

As the industry eschews fibre optics for cheaper, copper-wired Ethernet cables when wiring the ever-larger data centre clusters for the latest and fastest AI models, Arista looks well placed to take share in a growing market, supported by sustained capex from the very companies underwriting our chip holdings.

Crucially for us, this is also a quality business: a strong balance sheet, high operating margins and consistent cash generation. Just the kind of long-term compounder we like to own.

UK government bonds: Attractive on paper, risky in practice

We have also reduced our UK government bond (gilt) holdings again. In the lead-up to the local elections – which proved disastrous for the Labour government and sparked a leadership challenge from the left wing of the party – we felt it prudent to lighten our exposure.

Our concern is straightforward: if the party tacks further left in response, the resulting policies would likely unnerve the bond market.

More spending commitments, without a credible plan to fund them, means more gilt supply. And more supply, in the absence of commensurate demand, puts upward pressure on yields and downward pressure on prices. That’s bad for bondholders.

On a usual basis, gilts look attractive. Yields are decent, and the income they provide is nothing to sniff at. But it’s the risks around the edges that keep us from filling our boots.

Higher energy prices, driven by the ongoing Middle Eastern conflict, mechanically hit UK inflation more than in many other developed markets because of the structure of the UK’s power market.

We still have a decent amount of gilts in our portfolio, but lately we’ve been more inclined to spread more of our ‘Liquidity’ government bond assets across different countries to diversify ourselves.

We continued this strategy, using the cash raised from selling gilts to buy the US Government 4.125% 2036 and US TIPS (inflation-linked) 1.25% 2031.

The inflation-linked bonds should protect us if US inflation remains higher than expected for longer because of the effects of the Iran war on energy prices and the rapidly rising cost of memory chips.

What needs to happen next

Since the conflict with Iran began, AI companies and their suppliers have carried the market. For this performance to really broaden out, we think the Strait of Hormuz must be unequivocally reopened to tanker traffic.

That would ease anxieties around the costs of energy and fertiliser (and therefore food).

When the rally is driven by a handful of mega-cap names, diversified multi-asset portfolios like ours will inevitably lag. When it broadens – when more sectors and geographies start to participate – that’s when portfolios built on quality, diversification and risk management come into their own.

The Pakistani-brokered agreement to reopen the strait and work towards a lasting peace seems a promising start. However, this path is unlikely to be smooth – the continued fighting between Hizbollah in Lebanon and Israel is a case in point.

We hope that both the US and Iran have more to gain from peace than from continued conflict, which should continue to push them to de-escalate.

Main image: background flow, multi-colour, sean-sinclair-C_NJKfnTR5A-unsplash