Fidelity recently held an Applied AI Workshop, inviting experts and companies to discuss their experiences with the technology. What emerged strongly was a sense of a rapid rate of improvement in the underlying technology, which means that the largest frontier models continue to improve, and the cost of running smaller models continues to fall. Here, the asset manager unravels some of the key considerations for AI as it transitions towards mass adoption.

The market is betting on fast mass adoption of AI

We recently organised an Applied AI Workshop to understand how Artificial Intelligence is being applied by real-world industries outside of the tech sector. We engaged with a number of AI experts including users, vendors, academics and consultants who are involved in the process. It became clear that there are a number of considerations that companies are trying to resolve, including questions around budgets, IT infrastructure, ethical and security concerns, and recognising the value proposition of the technology.

A crucial milestone for any new technology is the point the adoption curve inflects. Typically, we see early adopters embrace the innovation, followed by mass-market adoption as the wider market becomes convinced of its utility.

The market expects the AI infrastructure build-out to continue rapidly as tech companies assume the adoption curve is going to ramp up. Of course, this is a big assumption, which our analysts are constantly testing. Adoption rates also vary by industry. In some industry. The adoption of new technologies tends to be rapid in some industries such as digital media, creative, and consumer internet. However, things can move more slowly in more complex or regulated sectors such as financial services.

Exploring the ROI case for AI adoption

A key part of the transition of new technologies into mass market appeal is cost. Prices for new innovations start high and as efficiencies are found, costs fall, making the novel solutions more attractive to a wider audience. In AI, computing costs are still high and there are other elements that are expensive.

In simplistic terms, an AI model requires training then it is ready to execute solutions (otherwise known as an “inference”). Training a model requires enormous computational power – this includes chips, which can be expensive. Nvidia’s latest available H100 GPU is estimated to cost around US$40,000 per unit. Meta is currently building two clusters of 25,000 GPUs each to train future models. In addition, when a business wants to deploy models for their own specific purposes this may require additional fine-tuning.

While training and fine-tuning the model are one-off costs, running the model is an ongoing expense. Inference calls in isolation require fat less computer power than training but if a model is used intensively this may require a high volume of calls. Our research shows that the cost of inference is falling rapidly due to more efficient algorithms and more powerful computer systems.

Company executives are thinking hard about the investment required to build out AI solutions cost-effectively and the timeline to achieve overall net cost savings. In the current macro environment this involves a series of trade-offs. Questions around where the AI budget will come from will have to be resolved.

Businesses will need to form a clear view about the value that AI offers to answer these questions. Speakers at our AI workshop highlighted how AI is being used to increase the productivity of existing processes, rather than doing entirely new things. The return on investment (RoI) case behind the adoption of systems such as Microsoft CoPilot seems genuinely impressive, and it is much easier to adopt this when it complements current operations rather than having to change how the business runs.

Companies also have to weigh up other considerations that will affect the benefits they capture from AI, such as which Large Language Model (LLM) to use (closed or open source?), the additional requirements for power and the associated impact on carbon emissions, and whether to develop in-house solutions or outsource.

The practical considerations – data, skills, regulation and security

At our Applied AI Workshop we unravelled user journeys, uncovering a number of underappreciated challenges that companies are currently wrestling with:

• Data – many companies are grappling with the quality of their data, which must be of a high standard to extract the most benefits from AI. Data is often stored in fragmented silos, incompatible formats, or housed in inadequate data infrastructure; all these impede the seamless integration of data into AI systems. Data governance is also important – you would not want an LLM to surface confidential data to the wrong person, even within the organisation.

• Skills – given that generative AI is a relatively new field with fast growth, labour skills have not kept up. There is a shortage of talent with specific skills needed to harness AI, whether integrating AI infrastructure, manipulating data, incorporating AI models, or deploying AI solutions. Employers also have to predict what skills will be required in future; for example, should they look for coders and IT engineers now knowing that AI is likely to dramatically alter these roles over time? The skills gap is likely to be an ongoing challenge.

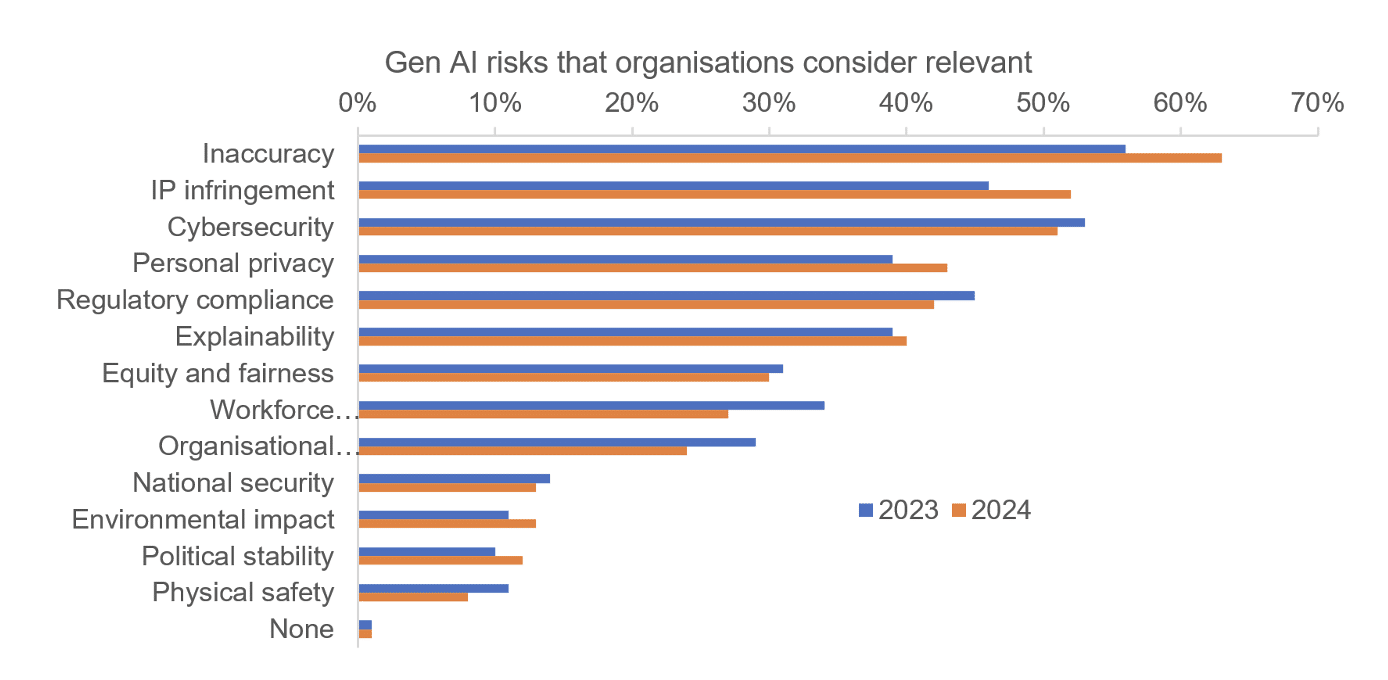

• Ethics, regulation, and security – companies are still adjusting to the ethical, regulatory and security implications of incorporating AI. Executives are hesitant about entrusting their IP and data to external ecosystems given the lack of transparency in many AI platforms. Companies also have to develop cybersecurity frameworks to protect their AI systems and they are unclear about ownership issues related to AI output. These obstacles are some of the reasons why AI has been slower to penetrate certain areas such as human resources departments.

• Company culture – among employees, we are hearing that there is fear about potential displacement caused by AI. Some workers are sceptical about the benefits of AI while others are concerned about the implications for their careers. Some companies have reported that it tends to be larger teams that are more resistant to embracing AI than smaller groups. This highlights that AI not only requires companies to change their IT plant, but also needs them to change their business process.

The practicalities of AI adoption

Source: McKinsey, March 2024. Note: 1,363 survey participants. Inaccuracy ranges from customer journeys and summarisation to coding and creative content.

Generative AI is not going away

The current AI trend offers huge potential and is a broad theme that will disrupt a range of industries beyond the tech sector, for example how it is already changing music creation and computer code generation. Investors should approach the technology holistically recognising that different parts of the value chain offer differing mixes of exposure and levels of risk.

Generative AI is still in the developmental stages where companies are exploring how best to use it. The computing infrastructure is not yet established, the compliance framework is underdeveloped, and there are a number of resource gaps limiting the pace of expansion. As investors, it’s important to combine long-term thinking and understanding of big picture implications with a bottom-up understanding of what is happening at the ground level of adoption. We believe that investors should be exposed to AI, but in a way that is fully cognisant of the risks as well as the rewards involved

The AI theme is likely to last for many years and have far-reaching effects. This is genuinely a marathon, not a sprint. There will be many winners – from household names to companies that haven’t even been founded yet. Some companies will deliver while others will disappoint. But we can be certain that we will never return to the way things were before ChatGPT arrived – generative AI is here to stay.

Read more Fidelity perspectives here>

Important information

This information is for investment professionals only and should not be relied upon by private investors. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of an investment in overseas markets. Investments in emerging markets can be more volatile than other more developed markets. Reference to specific securities should not be construed as a recommendation to buy or sell these securities and is included for the purposes of illustration only.