Japan’s transition to inflation represents a structural turning point for equity investors, says Theo Wyld – Portfolio Manager and Analyst on the Chikara Japan Income & Growth Fund and the CC Japan Income & Growth Trust plc. This article looks at the importance of pricing power.

Japanese stocks have rallied strongly following Prime Minister Sanae Takaichi’s decisive election victory in February.

Her LDP party secured 316 seats, comfortably above the 261 needed for an absolute majority, easing uncertainty and reinforcing confidence in the trajectory of Japan’s economy at a time when the market was already benefiting from powerful structural tailwinds.

However, while the election result may be helping to drive the Nikkei to all-time highs right now, political clarity alone will not determine the long-term performance of Japanese equities.

On that front, we believe one of the most influential forces of all will be inflation.

After decades of deflation, Japan has finally entered a sustained inflationary environment. And with this longer-term tide lifting some boats more than others, identifying quality stocks has become more important than ever.

Japan’s Inflation Story

For much of the past three decades, Japanese companies operated in an environment defined by stagnant prices, weak wage growth, and limited nominal expansion.

Stable costs and ultra-low often negative interest rates allowed even inefficient businesses to survive. Pricing discipline was less important, and the gap between strong and weak companies was compressed.

But that environment has now changed.

Sustained inflation has returned to Japan, and since 2024, the Bank of Japan has been taking advantage of this backdrop to free interest rates from their near-zero shackles, which they hope in turn will prevent runaway inflation.

So far, this looks to have been the case, with core year-on-year inflation of 2% in January matching the central bank’s target.

But inflation continues to present a double-edged sword to Japan.

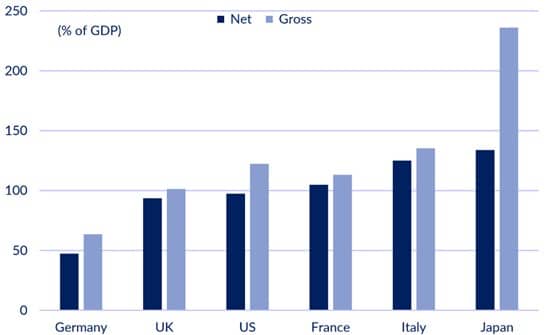

On the one hand, it’s helping to normalise the country’s economic balance after decades of extraordinary policies. Many headlines focus of gross debt as a percentage of GDP.

But one look at net debt as a percentage of GDP – which accounts for assets held by the country and is shown in the chart below, shows Japan is now approaching levels comparable to its global peers.

Added to which, the ratio has been improving and is expected to continue on this path, unlike many other developed economies.

Japanese Net Debt Compared with Gross Debt:

For companies, though, inflation introduces new pressures.

It increases operating costs, both in terms of input prices and, crucially, wages. Businesses operating with thin margins have little room to absorb these headwinds, and that means they must either raise prices or accept lower profitability.

It’s a critical shift.

In the past, deflation and ultra-low interest rates masked structural weaknesses. Today, inflation is exposing them, and companies must now rely on genuine competitive advantages to sustain profitability.

This is where pricing power becomes essential.

Stocks with pricing power are better equipped to pass rising costs onto customers while maintaining demand. This allows them to protect margins and preserve earnings even as inflation persists.

Strong brands, high market shares, and differentiated products all contribute to this resilience, and profit margins provide a clear indication of this strength.

Particularly, gross margins. Companies with high and stable gross margins relative to their competition often have some sort of economic advantage – a key attribute of a quality business.

In short, we believe inflation will drive a divergence in performance, and this is where active management becomes particularly valuable.

The companies we hold have an average gross profit margin of 34.6%, compared to 26.4% for the TOPIX as a whole[1]. This margin advantage can provide a meaningful buffer against rising costs and may help our portfolio businesses to sustain profitability as inflation persists.

The Importance of Pricing Power

Japan’s transition to inflation represents a structural turning point for equity investors.

The election result has helped lift the market in the near term. Companies with enduring business models have historically tended to outperform over the long term.

We believe investors who focus on higher-quality businesses with stronger margin profiles are best positioned to benefit from Japan’s evolving economic landscape.

[1] Per Bloomberg as of 27 February 2026

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. The writer’s views are their own and do not constitute financial advice.

This information should not be relied upon by retail clients or investment professionals. Reference to any particular investment does not constitute a recommendation to buy or sell the investment.

Main image: Japan, su-san-lee-E_eWwM29wfU-unsplash