History suggests that starting valuations remain one of the most reliable inputs into long-term returns. At a time when many equity markets are priced for optimism, that is a perspective worth keeping close says Ben Whitmore, Co-Manager of the TM Brickwood Global Value Fund and TM Brickwood UK Value Fund.

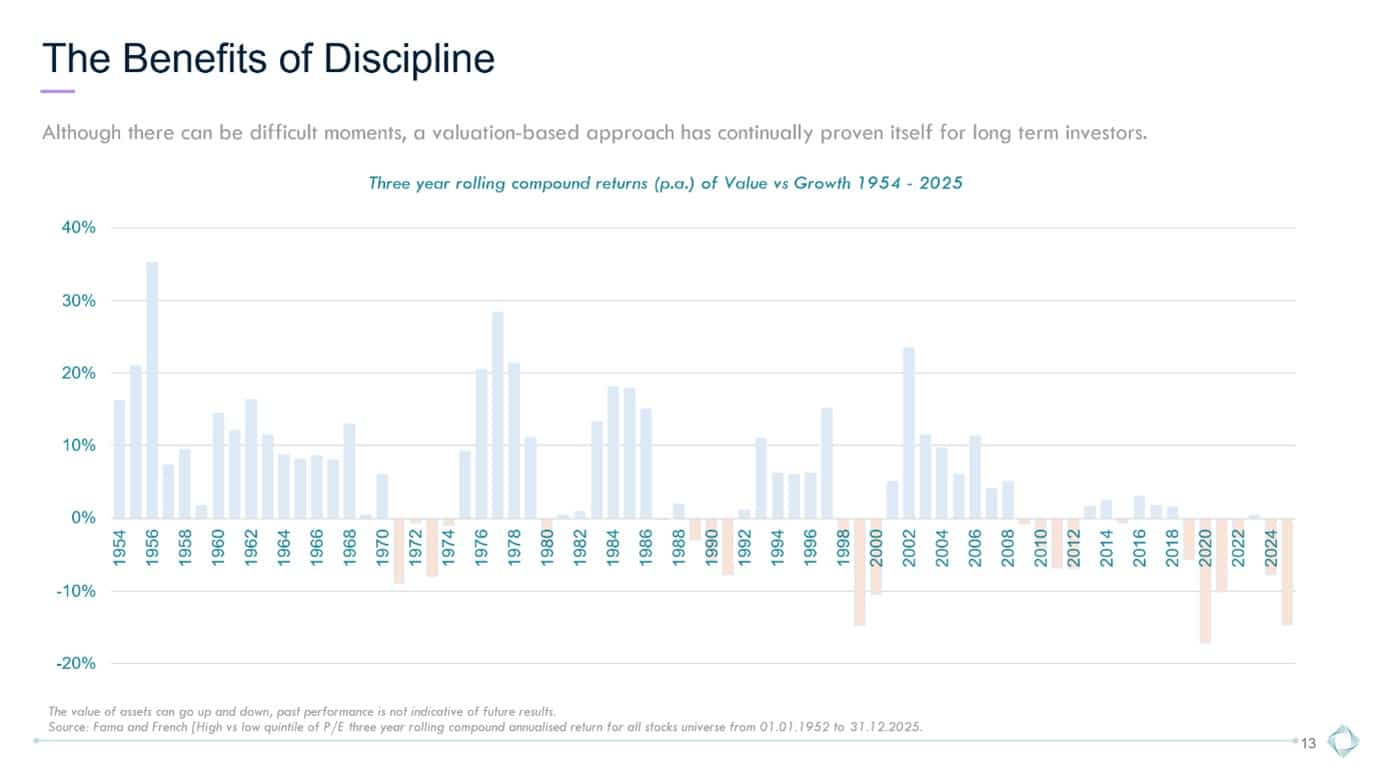

Over the past 70 years, value has been a successful style of investing. However, there are four difficult periods within recent memory, when abandoning it may have felt entirely reasonable.

The recession of the early 1990s, the late-1990s technology boom, the aftermath of the global financial crisis, and more recently during the dominance of a narrow group of large US technology companies.

Yet, each time, value has eventually reasserted itself. Not smoothly, and not on a neat timetable, but persistently enough to matter for long-term investors.

The uncomfortable truth is that the value premium has never been easy to harvest.

It requires living through long stretches where valuations may continue to look cheap for longer than expected, and where expensive stocks keep getting more expensive.

Unemotional screening

Living through this discomfort is easier if you can remain dispassionate and disciplined. That’s why we use two screens: the cyclically adjusted price earnings (CAPE) yield and Greenblatt.

The CAPE yield has historically been a very good predictor of subsequent ten-year returns. The higher the CAPE yield the higher the subsequent return and vice versa.

The CAPE yield takes the average of the real earnings over the last ten years and divides it by the market capitalisation of the company.

This allows us to look for lowly valued companies across a business cycle (ten years) and compare companies across countries with different rates of inflation.

The Greenblatt screen ranks stocks separately by valuation and quality and then combines the ranking. The lowest combined rank highlights companies with the best combination of value and quality.

These screens are unemotional and keep us pointed towards lowly valued stocks with potential to rerate.

What “value” looks like today

The value opportunity set has evolved in recent years, and will continue to evolve as market dynamics change.

For example, in 2020 the UK the screens were highlighting banking, telecommunications, tobacco and mining.

Today’s value universe includes a growing number of companies that would previously have been described as “quality compounders”: businesses with strong brands, resilient cash flows and global reach, whose valuations became stretched during the low-rate era and have since normalised.

Diageo, Bunzl, Tate and Lyle, Reckitt Benckiser and Croda are good examples.

In parallel, there are former growth stocks where expectations proved too optimistic and prices adjusted accordingly. These are names such as the UK housebuilders, JD Sports, B&M, Burberry and Prudential.

The passage of time means that areas that were once too expensive for value investors to consider are now lowly valued and vice versa.

It has been said that, if you follow the stock market for long enough you will ultimately see every stock on every rating.

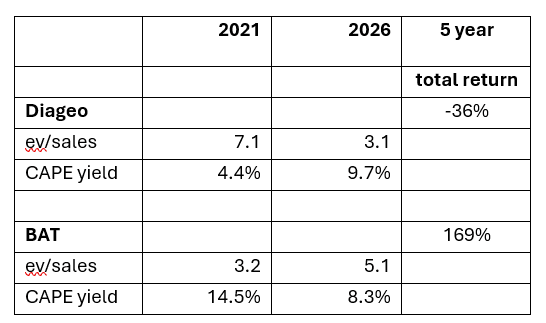

When valuations do the heavy lifting

A simple comparison from the consumer good sector illustrates the point. In 2021, shares in Diageo were trading on a very low CAPE yield of 4.4% versus the long run average of the UK stock market of 6.5%.

The prospects for Diageo were deemed to be good. At the same time, British American Tobacco (BAT) was very lowly valued with a CAPE yield of 14.5% with worries over its future.

Fast forward five years and the picture looks very different. The valuations have now reversed with a very different set of share price performances.

Diageo’s share price has struggled as higher valuations met slower growth, changing consumer behaviour and a dividend cut.

British American Tobacco, meanwhile, delivered strong returns as fears eased and cash generation proved more resilient than expected. Importantly, this outcome did not require heroic forecasting. It relied primarily on starting valuation.

Source: Brickwood 27 February 2026

Today, using the same discipline to identify lowly valued stocks, we have recently invested in Diageo.

Because, for investors, the lesson is straightforward but powerful: low valuations can provide a margin of safety even when the narrative feels uncomfortable, while high valuations leave little room for error, even in excellent businesses.

Concentration

Global indices have become increasingly concentrated. The largest stocks now dominate returns, and many are exposed to the same theme: artificial intelligence.

So while holding an equity market tracker may feel diversified because it owns hundreds or even thousands of companies, in reality, risk is increasingly concentrated in a narrow group of very large, very expensive businesses.

In the case of the MSCI All Countries World Index, the top ten constituents now represent close to a quarter of its market capitalisation.

When sell-offs occur, this concentration matters. Moves in a small number of stocks can drive overall index performance, for better or worse.

In contrast, value portfolios tend to spread exposure more evenly across regions and sectors, not by design, but as a by-product of valuation discipline.

For investors, this creates an important behavioural benefit. When investors worry about how long a rally can last, value strategies can offer a way to stay invested while acknowledging those concerns, rather than trying to time exits or make wholesale asset allocation shifts.

Patience remains non-negotiable

None of this is an argument that value will outperform tomorrow, next quarter, or even next year. It is an argument that valuation still matters, particularly when markets are expensive and narrow.

Value investing works slowly, unevenly and often uncomfortably. It requires patience, a tolerance for looking wrong in the short term, and an acceptance that the market’s enthusiasm for fashionable themes can persist longer than expected.

But history suggests that starting valuations remain one of the most reliable inputs into long-term returns. At a time when many equity markets are priced for optimism, that is a perspective worth keeping close.

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. The writer’s views are their own and do not constitute financial advice.

This information should not be relied upon by retail clients or investment professionals. Reference to any particular investment does not constitute a recommendation to buy or sell the investment.

Main image: arturo-anez-Q_vhJv5im-8-unsplash