David Jane and the team at Premier Miton Investors, will be watching how two interlinking conflicts play out over the coming months before taking action.

At present financial markets might be balancing fundamentals against liquidity. The same may be true of the real economy, while employment and business prospects have been under pressure, household and corporate liquidity in the US is very strong. How these two interlinking conflicts play out over the coming months will be crucial for markets.

The early stage of the post-crisis equity rally has been heavily driven by liquidity as central banks globally have injected huge amounts of cash into banking systems which, without an obvious place to go in the real economy, inevitably finds its way into asset prices. This huge rise in equity prices now means that US equity markets are materially higher over one year, despite a large fall in economic activity and corporate profits.

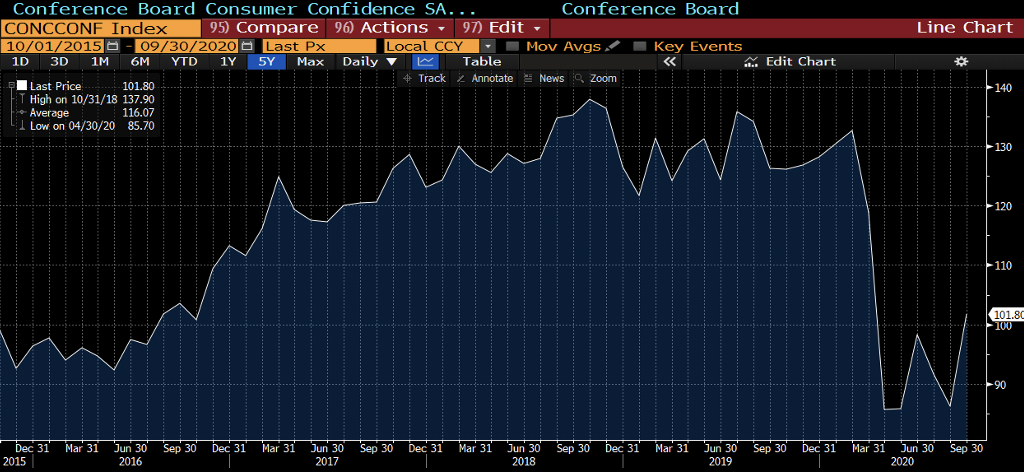

The government income support schemes as a consequence of Covid lockdowns have had a profound effect on consumers cash positions, particularly as they have been less inclined to spend money recently. Strangely, despite there being a recession, US households have record cash levels. At the same time ongoing economic uncertainty is leading to weakening consumer confidence.

Corporate liquidity has also been supported by governments and especially by a huge recycling of central bank liquidity into corporate bond issuance earlier in the year. So while profits may be under pressure, outside of a few obvious industries, balance sheet cash positions are very strong. Businesses have money to spend, what they lack is the confidence in their future prospects to invest heavily.

Markets always recover well before economies recover as they anticipate the future, however, the current year seems somewhat extreme. As we look through to the end of the year we need to see a stronger economic recovery to justify current levels, absent further injections of liquidity. Indeed, while central banks remain supportive it seems unlikely that further massive liquidity injections will come about in the absence of a significant sell off. Hence, we might think that economic prospects are becoming ever more important.

This is where the US consumer might come in. For many years US consumers have been a major driver of economic growth. This year they have taken some major hit to confidence, with jobs prospects deteriorating, lockdowns and other restrictions on spending. These however have been more than offset by direct government handouts, such that their balance sheets are in great shape. If they start to spend their windfalls the flywheel of the US economy could really start to spin, leading the corporate sector to hire and invest some of that excess cash.

Holding consumers back has been the volatile news flow this year and they still have a highly contentious election to contend with, in November. However, these issues will pass and at some point they will realise that in aggregate they have plenty of money to spend. Confidence had been strong throughout the Trump Presidency until the virus hit, but now appears to be beginning to recover.

Chart source: Bloomberg

If this trend continues the recovering economy globally will be given a strong boost. This in turn would help to support current equity market levels.

We are not believers in attempts at predicting the future, we do however like to consider a range of future scenarios and how we would need to adapt to each of them. Were the US consumer to come through with some strong growth in the coming months this might be a spur to drive a rotation in equity markets. Thus far the recovery has been heavily driven by growth stocks, particularly in the digital economy and new energy themes. Were we to see a stronger cyclical rebound, some of the harder hit areas might start to perform. This would require a degree of rebalancing from us. However, we do not act pre-emptively. Until we see evidence of this playing out in stock prices we would not act. The outcome of these two Tugs of War is still unclear.