Deferral of the State Pension can give higher rates of payment further down the line but the benefits have to be weighed.

People who reach State Pension age on or after 6 April 2016 receive the new State Pension. They can

benefit from a 1% increase in their weekly State Pension for every nine weeks that payments are deferred,

equivalent to around 5.8% extra income for every full year deferred.

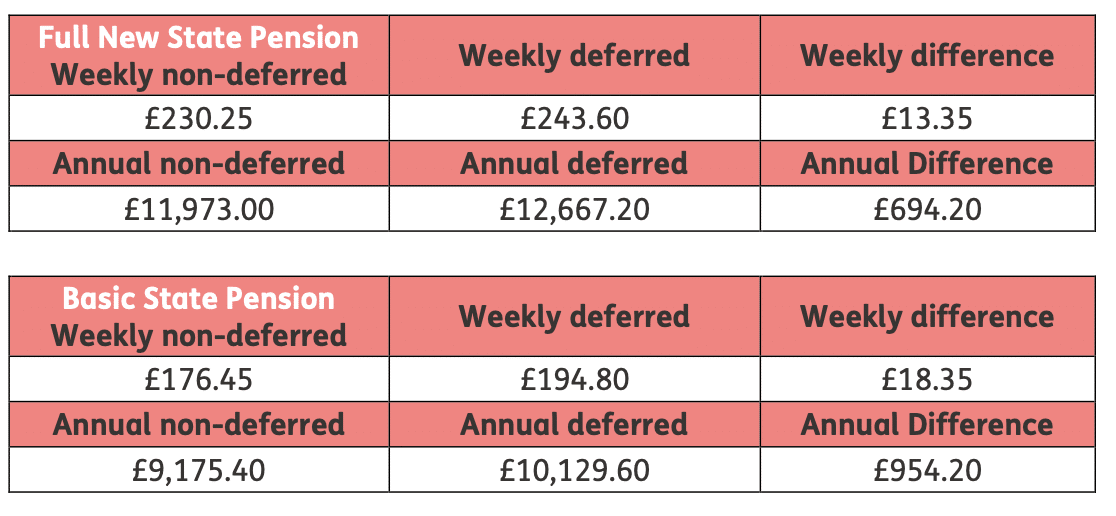

With the triple lock boosting the new State Pension to £230.25 a week this year, those who defer their

payments for the 2025/26 financial year will benefit from an extra £13.35 a week – which equates to an additional £694.20 of income every year for life (plus any inflation-linked increases).

Those who reached State Pension age before 6 April 2016 and chose to defer are treated more generously,

with an extra 1% State Pension income for every five weeks deferred, equal to an annual rise of 10.4% or

£954.20, which can be taken either as extra income or a lump sum.

Source: Just Group

However, research by Just Group showed awareness of the potential to defer the State Pension was low among those aged 40-65, and only only one in 10 (10%) adults aged 66-75 said that they had delayed its receipt.

Among those that deferred, the main reasons for doing so were not having a financial need to claim straight away, the higher payment down the line, and not needing the payment as they were continuing to work.

Just Group points out that it takes around 17 years to break even if the State Pension is deferred for a year, so health and life expectancy are key considerations when weighing up whether an individual could benefit.

Currently, any extra income accrued through deferring the State Pension offers protection against inflation – a valuable safeguard for those planning for a long retirement.

Main image: zach-lucero-qAriosuB-lY-unsplash