Dan Bosiacki, Technical Consultant at AJ Bell provides some food for thought – literally – in this article about whether or not clients should take their tax free cash.

You will likely know of clients, be they your own or those serviced by your colleagues, that peel the lid off years of disciplined pension savings, crystallise a pot and begin drawing income from it, sometimes with barely a second thought.

It’s a bit like going straight for the cone and skipping the ice cream.

Whilst the code for eating such desserts thankfully remains unwritten, we do have pension and tax rules to work with, and they suggest that not everyone is suited by waiving their way to their wafer.

Tax-free cash is one of the most advantageous tax breaks that many of us will receive in our lifetimes.

Restricted for the majority to the lower of 25% of an individual’s fund value or their available Lump Sum Allowance (which for most is £268,275), it is one of the recognised kick-off events, along with an uncrystallised funds pension lump sum (UFPLS).

The pension rules

The regulations have been subject to major upheaval in recent years as we know.

During the era of the lifetime allowance, both events (PCLS and drawdown) were separate crystallisations of the pension.

For now, we’re in calmer waters. Only lump sums are tested and anything taken over the member’s lump sum allowance is taxed at their marginal rate.

That at least allows for sensible tax planning to take its course rather than the unwelcome shock of the lump sum tax charge.

The nuance

This latest raft of regulatory change has undoubtedly brought flexibility and optionality, and we are seeing our members grasp it with both hands, particularly where a valid reason exists for not following the administrator’s standard policy.

That is to forego the PCLS element of a crystallisation. However, this decision must be fully considered because the implications can differ across the demographical spectrum.

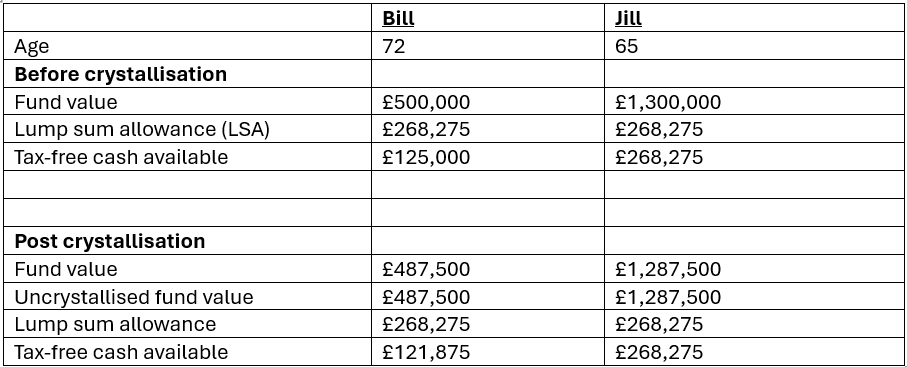

Let’s take the example that your client has no other taxable income and wishes to take £12,500 from their pension.

As no tax would be due on this because it falls within their personal allowance for tax purposes, they decide to forego their tax-free cash.

However, the decision to forfeit the ice cream (PCLS) in favour of the cone (drawdown) can be significant.

While Bill and Jill are both basic rate taxpayers and have identical tax positions, the impact of the crystallisation is felt more firmly by Bill, who loses his ability to take £3,125 tax-free cash in the future following his decision to forego tax-free cash.

Jill, however, has sufficient savings built up at the point of crystallisation to not feel the impact of the deferral.

This is because Bill’s tax-free cash is limited to 25% of his uncrystallised fund value, whereas Jill’s tax-free cash is limited by the lump sum allowance.

Aside from the crunch, there are reasons why both Bill and Jill may want to consider forgoing their tax-free lump sum.

- They may have retired overseas and are holding residency in a country that doesn’t recognise the status of UK pension tax-free cash, simply treating any payment as taxable income. Double taxation treaties should be reviewed where they are in force for a full tax position.

- They are in good health and wish to purchase a larger annuity at outset, potentially because they believe favourable rates won’t be sustainable long-term and the product they have found beats bank accounts and ISAs.

- They have limited LSA remaining and some pension savings elsewhere that take priority.

The essence of the story is to take care with the decision.

Clients can often be tax neutral particularly when drawing from their pensions slowly and within the personal allowance but their entitlement to tax-free cash can be lost rather than saved for the next sunny day.

As the priority for clients is often to pay less tax, it’s a tax break not to be surrendered lightly.

Main image: ice cream cone, zach-camp-3D0HUHFcRrk-unsplash