Laura Suter, director of personal finance at AJ Bell looks at how dividend tax has changed seven times in 11 years, with the latest rate hike coming in the 2025 Budget, which has seen basic-rate taxpayers go from effectively 0% tax to 10.75% by 2026, and provide some tips on how to beat the dividend tax hike.

Dividends have faced an onslaught of changes over the past decade, and investors and company owners have seen soaring bills during that time. Over 11 tax years we will have had seven different systems for dividend tax, with either the tax rates or the tax-free allowance changing. During that time basic-rate taxpayers have gone from paying effectively 0% tax on their dividends to 10.75% from next year, with just a £500 tax-free allowance. The figures lay bare just how much more expensive it has been to be an income investor with money outside an ISA or pension, and how company directors have faced a crackdown on their tax rates.

The crunch on dividends has dragged millions more people into paying the tax for the first time. Figures from HMRC, obtained under an FOI from AJ Bell, found that 3.7 million people are expected to pay dividend tax this year, which has more than doubled since 2021/22. Over £18 billion in dividend tax is set to line Treasury coffers for this tax year alone. The tax changes from April next year are expected to add another £280 million to this for the next tax year and £1.2 billion a year on average from 2027/28.

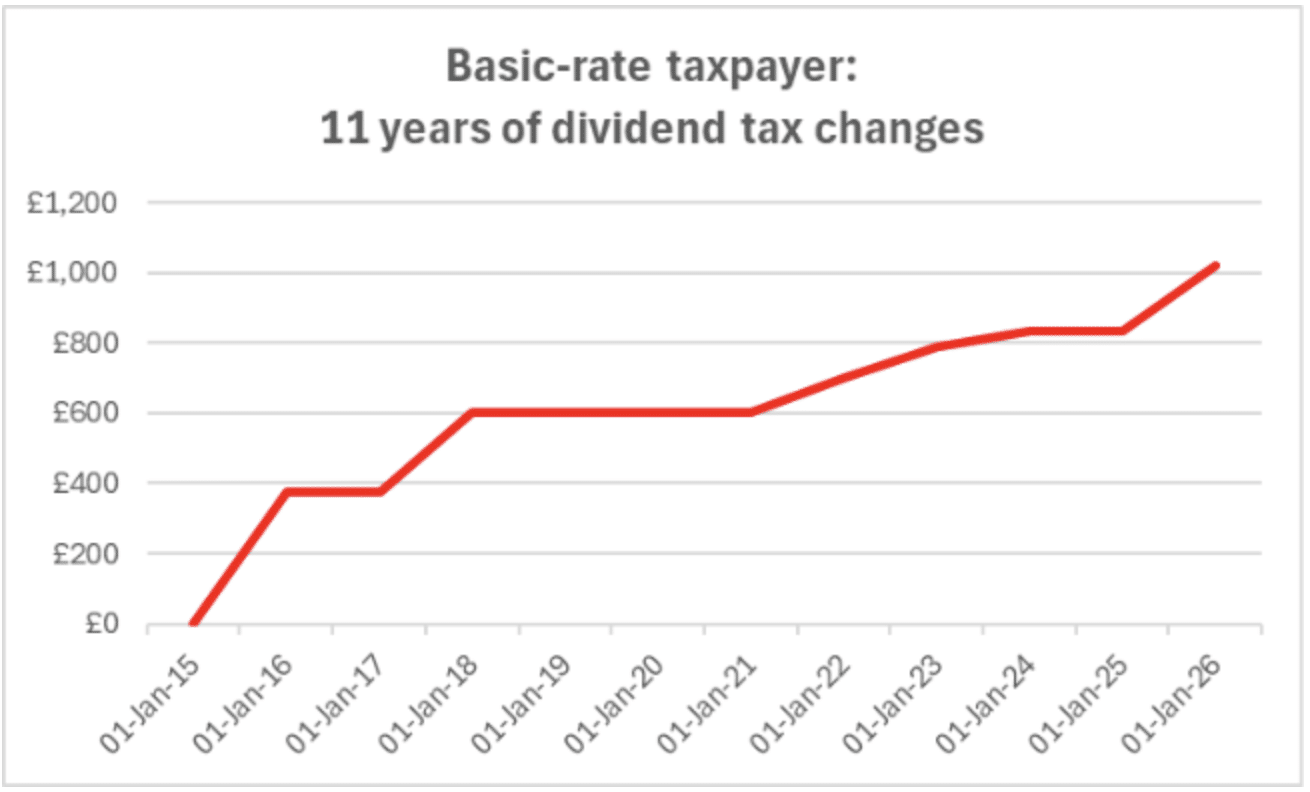

A basic-rate taxpayer with £10,000 of dividends a year, assuming they’d used their personal allowance already, would have paid no tax on dividends in 2015, but 10 years on they will be handing over £1,021 in tax on that income from April next year. Those with sizeable taxable dividends have seen their tax bill rise dramatically, with a basic-rate taxpayer on £30,000 of dividends paying no tax in 2015 and £3,171 from next April.

Higher-rate taxpayers have faced a bigger increase in their tax bills than additional rate taxpayers, thanks to the big hike in tax rates – their rate has gone from an effective rate of 25% in 2015 to 35.75% from next year. In comparison additional-rate taxpayers have seen a rise from an effective rate of 30.56% in 2015 to 39.35% from 2022.

This is shown in the figures, with a higher-rate taxpayer earning £30,000 in dividends paying £3,046 more in tax than they did in 2015 from next April. That’s a 40% increase in their tax bill, and £606 more than the increase seen by an additional-rate payer. Even at £10,000 of dividends a higher-rate taxpayer has seen a £896 hike in their tax bill, to £3,396 next year, while an additional-rate payer has seen a lower £682 jump (to £3,738).

| How dividend tax changed from 2015 to 2026 | |||||||||

| Basic rate taxpayer | Higher rate taxpayer | Additional rate taxpayer | |||||||

| Dividends | Tax bill in 2015 | Tax bill in 2026 | Increase | Tax bill in 2015 | Tax bill in 2026 | Increase | Tax bill in 2015 | Tax bill in 2026 | Increase |

| £10,000 | £0 | £1,021 | £1,021 | £2,500 | £3,396 | £896 | £3,056 | £3,738 | £682 |

| £20,000 | £0 | £2,096 | £2,096 | £5,000 | £6,971 | £1,971 | £6,112 | £7,673 | £1,561 |

| £30,000 | £0 | £3,171 | £3,171 | £7,500 | £10,546 | £3,046 | £9,168 | £11,608 | £2,440 |

Source: AJ Bell

Source: AJ Bell. Based on £10,000 of dividends.

How the system has changed

In 2015 basic-rate taxpayers enjoyed zero tax on their dividend income, thanks to a notional 10% tax credit that perfectly matched their 10% tax rate. When the tax rules changed in 2016 many were protected by the £5,000 tax-free dividend allowance, which when coupled with any remaining personal allowance that the individual had meant many were protected from paying any tax. But that allowance has since been slashed by 90%, to just £500 from 2024. At the same time dividend rates have ratcheted up over the years and from next year they will go up again, creating a double squeeze on those with even smaller taxable dividend amounts.

| How dividend tax has changed over the years | ||||

| Date from | Basic rate | Higher rate | Additional rate | Dividend allowance |

| 06-Apr-15 | 0% | 25% | 30.56% | £0 |

| 06-Apr-16 | 7.50% | 32.50% | 38.10% | £5,000 |

| 06-Apr-18 | 7.50% | 32.50% | 38.10% | £2,000 |

| 06-Apr-22 | 8.75% | 33.75% | 39.35% | £2,000 |

| 06-Apr-23 | 8.75% | 33.75% | 39.35% | £1,000 |

| 06-Apr-24 | 8.75% | 33.75% | 39.35% | £500 |

| 06-Apr-26 | 10.75% | 35.75% | 39.35% | £500 |

| Source: AJ Bell/HMRC | ||||

How to mitigate the dividend tax

All investments held in an ISA or pension aren’t subject to the dividend tax, so the route to a lower tax bill is to move money into these accounts, assuming access to this money is needed and it can’t be tied up in a pension.

Potentially £40,000 can be moved into an ISA before the latest tax hike starts to really bite by using this year’s allowance now and next year’s as soon as the new tax year starts in April.

For those with a spouse who also hasn’t used their ISA allowance this year (and doesn’t have their own investments outside an ISA) this allowance can be doubled, shifting the portfolio away from tax more rapidly. These processes are called ‘Bed and ISA’ and ‘Bed and Spouse and ISA’.

If the non-ISA investment pot is larger than the allowances the smartest move is to prioritise shifting the biggest dividend-paying investments into an ISA first. This means more of the dividend income can be sheltered from tax first and therefore cut the tax bill.

To do this the portfolio would need to be ranked by the holdings and how much income they generate, moving the highest income generating investments into an ISA first. The exact amount of tax saved depends on the specific portfolio and how quickly those income-paying investments can be moved into an ISA.

Main image: mjh-shikder-X762DfCZwRA-unsplash