Continuing her series of articles for Professional Paraplanner, Steph Willcox, Head Actuary at Dynamic Planner, considers where cash flow modelling now sits within the context of Consumer Duty and the retirement income advice review.

It’s now been over a year since the New Consumer Duty was published, and six months since the FCA published their guidance for good cash flow modelling when demonstrating suitability.

Whilst the Consumer Duty was light on actual guidance for using cash flow modelling, their subsequent publishing wasn’t. They clearly set out five findings from their review into retirement income advice and what they expect from paraplanners, advisers, and everyone involved in the financial advice world.

Today I’m going to take a look at the five findings so that you can see what steps you might already be taking to meet the FCAs definition of good practice.

Finding 1: Firms relying on information without considering accuracy

The FCA recognises that a great cash flow plan cannot happen without great data, but is concerned that advisers are using out-of-date information, or blindly accepting client updates without questioning what has been provided.

Possible steps you could take to improve this:

- Ensuring the data used in cash flow modelling is up-to-date and valid, this will include salary information, as well as how contributions are paid, expenditure and investible asset valuations

- Check that all sources of income are collected – you may provide a checklist of likely sources of income, or use bank statements to support a client’s own declarations

- Check that expenditure levels now and in the future are reasonable – you may want to compare this to standard levels of expenditure like the Retirement Standards published by PLSA and updated regularly.

- Try to reduce the amount of estimated figures used in the modelling unless necessary

Finding 2: Using justifiable rates of return

The FCA specified that “the returns used within cashflow modelling are one of the most important parts of the model” and “firms [should] have a reasonable and justifiable basis for all assumptions they use in the model.”

Possible steps you could take to improve this:

- Check that where you are picking investment assumptions yourself, two clients invested in similar assets would have the same or similar investment assumptions

- Check there is a process for determining the correct rate of return to use

- If you are using software, check that you understand what rates of return are being used, and the frequency with which they are reviewed and updated

- If you are not using a stochastic cash flow model, make sure that stress testing of the investment assumptions are being performed as standard

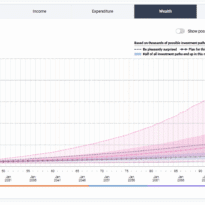

Finding 3: Planning for uncertainty

The FCA has found that cash flow planning can be misleading for clients where it is poorly explained to clients. Examples of this include mixing real and nominal terms or planning for average life expectancy.

Possible steps you could take to improve this:

- Check that outputs are shown in real terms if possible

- Plan beyond life expectancy since people generally underestimate their life expectancy

- Highlight the results of your stress testing, or highlight the lower percentile outputs if using a stochastic model

- Produce alternative scenarios for clients to show the impact of higher withdrawals on the invested portfolio

Finding 4: Consumer understanding

A clear part of Consumer Duty is ensuring that your clients understand what they are looking at, particularly if they have reports they are taking away outside of adviser meetings, and the FCA is keen to ensure that all communications received from an adviser are consistent, or explainable if they are not.

Possible steps you could take to improve this:

- Be aware of differences in communications and try to keep all messaging consistent, particularly communications being sent directly to the client

- Ensure that any reports to the client, or notes to the adviser, clearly explain differences in scenarios if they have been produced

Finding 5: Consider the output

The FCA want to ensure that advisers are reviewing the information they are about to provide, to check it’s appropriate and based on suitable assumptions. They particularly highlight that cash flow models could include withdrawing from assets before they are available – like a pension before the minimum pension age – or from illiquid assets that a client has no desire to sell, or that expenditure items might not be detailed enough to cover specific life events.

The FCA is also encouraging advisers to check how long funds will last under the base and additional scenarios.

Possible steps you could take to improve this:

- Consider what scenarios would be meaningful for each client, rather than producing the same scenarios for all clients

- Check that the results of the cash flow model seem reasonable, and are in line with other cash flow plans you have produced

- Check that the important outputs of the cash flow model are clearly shown in communications

Summary

I hope that this reconsideration of good practice helps you to understand where you are meeting or exceeding the FCAs expectations, and highlight where more consideration may be needed in your cash flow plan creation.