Ian Lowes, managing director of Lowes Financial Management and founder of StructuredProductReview.com, looks at the FTSE CSDI Index, an alternative underlying which can allow enhanced returns to be offered on structured products using the index.

In Spring 2020 financial markets nosedived with the coronavirus pandemic unfolding rapidly, catalysed by global consternation festering and whole countries being ‘locked down’. One of the consequences of such uncertainty was that companies, not least those listed on the FTSE 100 Index, significantly reduced the dividends they paid out, if not stopped them entirely. Throughout 2020, 53 current or former members of the FTSE 100 Index had cut, deferred, or cancelled over £37 billion of dividend payments[1]; the forecasted dividend yield for 2020, as quoted in December 2019, was 4.7%, with the yield in December 2020 falling to 3.2% (AJ Bell)[2].

In Spring 2020 financial markets nosedived with the coronavirus pandemic unfolding rapidly, catalysed by global consternation festering and whole countries being ‘locked down’. One of the consequences of such uncertainty was that companies, not least those listed on the FTSE 100 Index, significantly reduced the dividends they paid out, if not stopped them entirely. Throughout 2020, 53 current or former members of the FTSE 100 Index had cut, deferred, or cancelled over £37 billion of dividend payments[1]; the forecasted dividend yield for 2020, as quoted in December 2019, was 4.7%, with the yield in December 2020 falling to 3.2% (AJ Bell)[2].

The decrease in dividend yield, coupled with a heightened degree of uncertainty more generally, made forecasting increasingly difficult to the extent that the banks were building in a greater margin for error. Resultantly, this played a significant role in the coupons offered on FTSE linked structured products being substantially lower than pre-pandemic levels. The FTSE Custom 100 Synthetic 3.5% Fixed Dividend Index (FTSE CSDI) was created in July 2020 to offer a solution.

FTSE CSDI Index

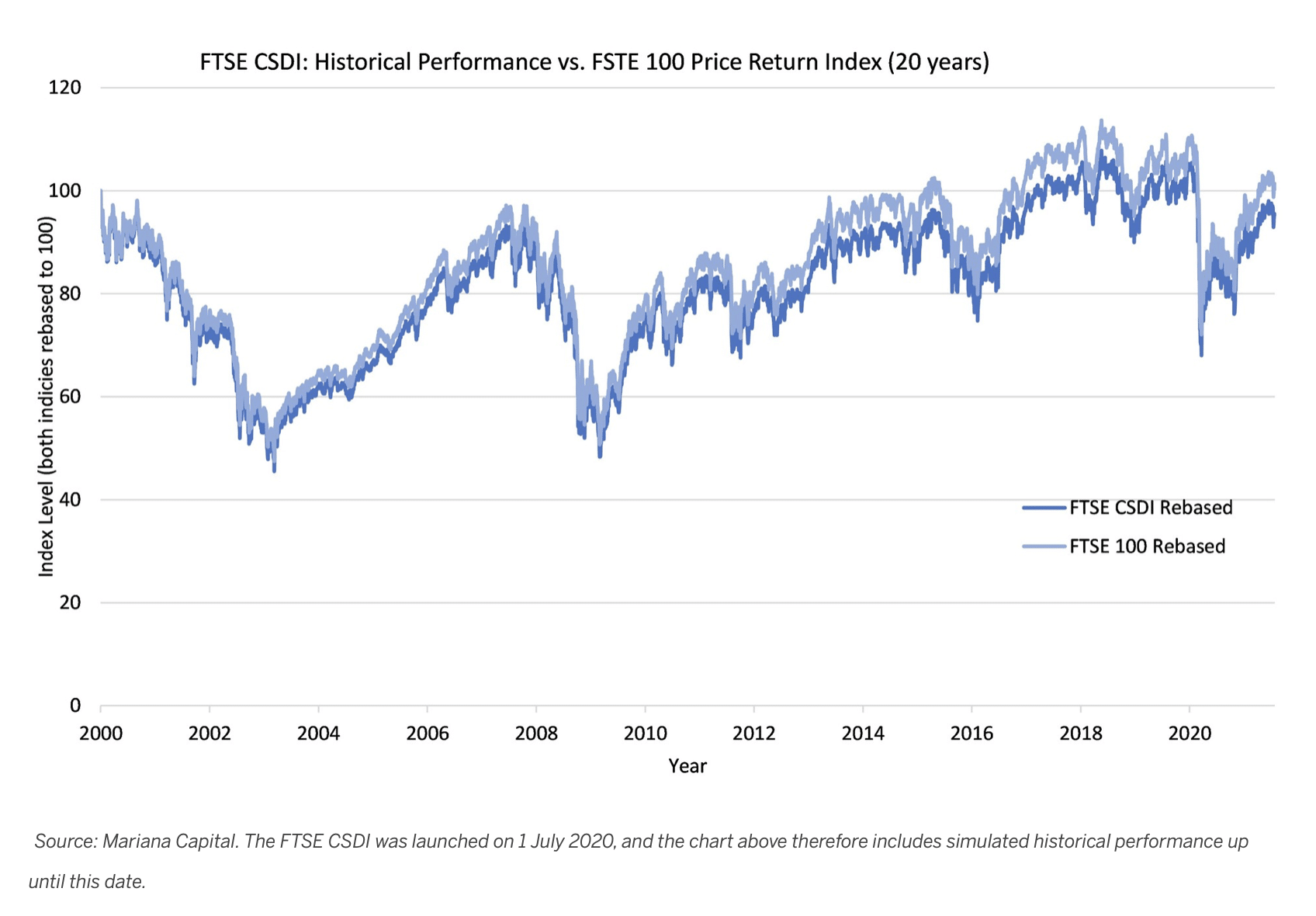

The FTSE CSDI Index was created specifically for structured products by FTSE Russell, the same organisation that calculates and publishes the FTSE 100 Index. The CSDI tracks the same 100 shares but unlike the FTSE 100, the CSDI includes the benefit of the dividends paid by the 100 companies (which have historically averaged around 3.5% per annum) and then deducts the equivalent to a fixed 3.5% dividend per annum, on a daily basis.

As reward for the structured product investor accepting the risk of variability of dividends, the counterparty bank does not have to; the net result is that the returns that can currently be offered on structured products are enhanced by using the CSDI which is around 98% correlated with the FTSE 100 index.

Source: Mariana Capital. The FTSE CSDI was launched on 1 July 2020, and the chart above therefore includes simulated historical performance up until this date.

The result is that the index will perform almost identically to the FTSE 100 if dividends are at 3.5% pa, moderately underperform if they are less, and moderately overperform if they are more.

Whilst there will be a draw on the FTSE CSDI relative to the FTSE 100 during periods of dividend yield shortfall below the fixed 3.5% decrement, any shortfall thus far has been negligible, and we believe that investors are being adequately potentially rewarded by the increased coupon payable under CSDI contracts, as indicated by the table below. Conversely, if dividends do transpire to be above 3.5% the CSDI will outperform the FTSE 100 – great if you’re also being compensated for taking the risk that didn’t come to fruition.

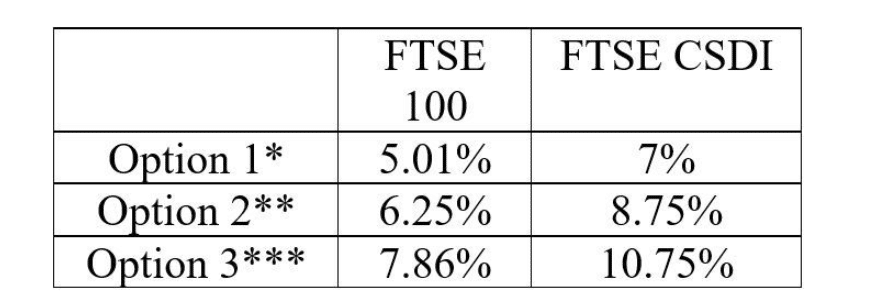

The table below shows the indicative coupons offered by Morgan Stanley International PLC at the time of pricing the Mariana 10:10 Plan September 2021[3], utilising the FTSE 100 index compared to those achieved utilising the FTSE CSDI index.

*The kick out barrier for Option 1 begins at 102.5% in year two, reducing by 2.5% pa thereafter, down to 82.5% in year ten.

**The kick out barrier for Option 2 remains at 100% throughout.

***The kick out barrier for Option 3 remains at 105% throughout.

Dividend yields post pandemic

As we begin a steady return to normalcy as a society, financial markets are beginning to follow suit; the forecasted FTSE 100 dividend yield for 2021 is currently 3.7% (AJ Bell)[4], up 0.5% since December 2020.

Although the forecasted yield has improved somewhat, it remains well below pre-pandemic yields, which coupled with lingering socioeconomic uncertainty means that the benefits offered by the FTSE CSDI remain; investors utilising the CSDI as an underlying take on the risk of variability of dividends so the bank doesn’t have to, which should translate to higher potential coupons on offer than with equivalent FTSE 100 contracts.

If dividends continue to increase, there will of course come a point where the coupons under new CSDI contracts are in line with FTSE 100 contracts – though the dividend yield will likely need to be considerably above the 3.5% decrement in order to outweigh the certainty provided by the CSDI.

For more information on the FTSE CSDI, please see here. A link to the current price of the Index can be accessed via www.Lowes.co.uk/CSDI. Details of the latest Mariana 10:10 and 8:8 Plans, linked to the performance of the FTSE CSDI, can be found here.

[1] https://www.ajbell.co.uk/sites/ajbell.co.uk/files/20201210_AJBYI_Dividend_dashboard%20FINAL.pdf

[4] Source: Mariana UFP

Structured investments put capital at risk. Past performance (actual or simulated) is not a guide to future performance.

Disclosure of interests: Lowes has provided input into the concept, development, promotion and distribution of the 10:10. Lowes has a commercial interest in these investments as a result of its involvement. Where Lowes is involved in advice on these investments to retail clients, it will not receive benefit of any fees for its involvement, other than those fees payable by the client to Lowes.