Japanese bonds continue to adjust, with higher yields opening up opportunities that were absent just a few years ago – David Roberts, Head of Fixed Income at Nedgroup Investments comments.

Japanese bonds continue to play catch up to other G7 bonds – with market manipulation being prevalent until recently whereas QE was generally wound down elsewhere 3-4 years ago.

Government policies aimed at stimulating the economy are well known, requiring added bond supply

A weak Yen continues to boost exports at the expense of imported inflation

We, like the market believe the Bank of Japan remains ‘politically influenced’ and is behind the curve (too slow to raise rates, should have done so in 2022).

The sell off, especially in long maturity bonds has been extreme.

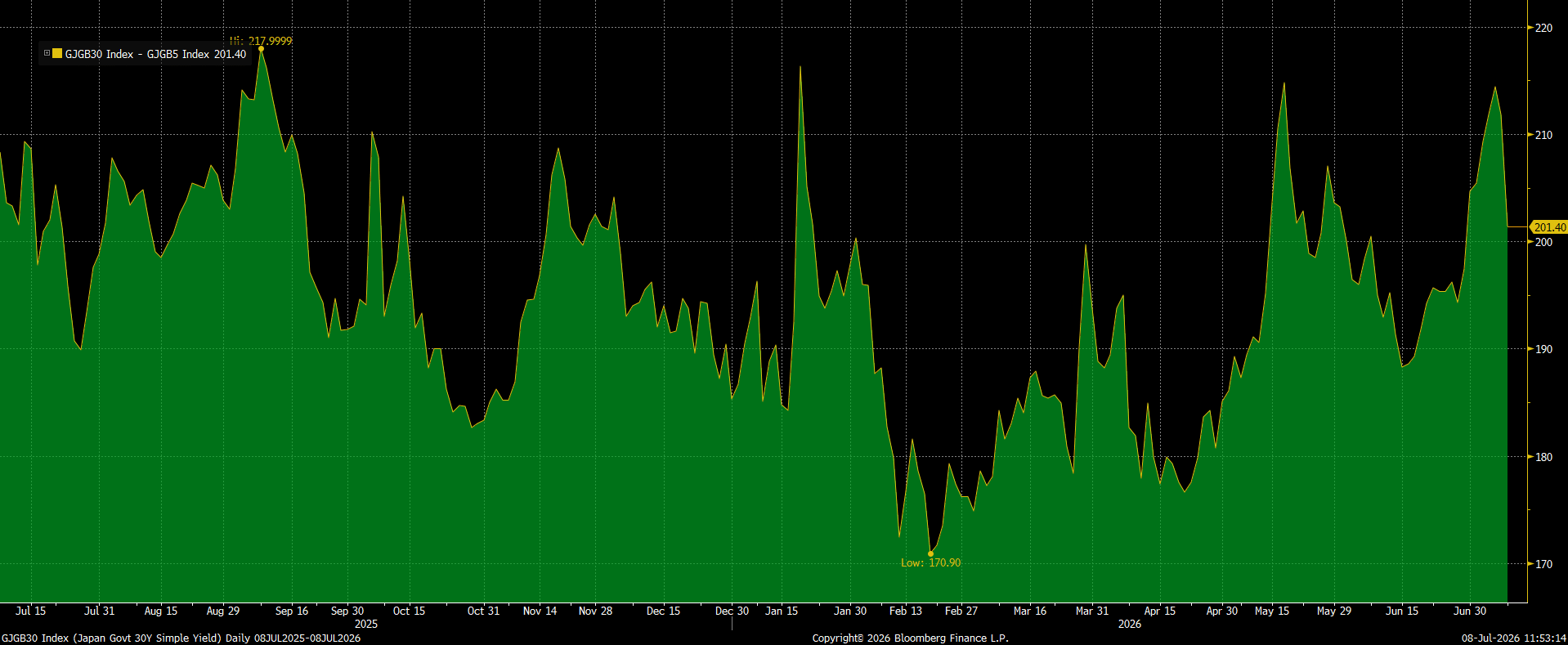

We are now paid much more to own Japan for 30 years than we are to own Germany. We remain well underweight Japanese bonds but are ‘index neutral’ longer dates and zero weighted to short dates.

We are paid an extra 2% to own 30-year versus 5-year. Over the past year, that is little changed.

Source: Bloomberg

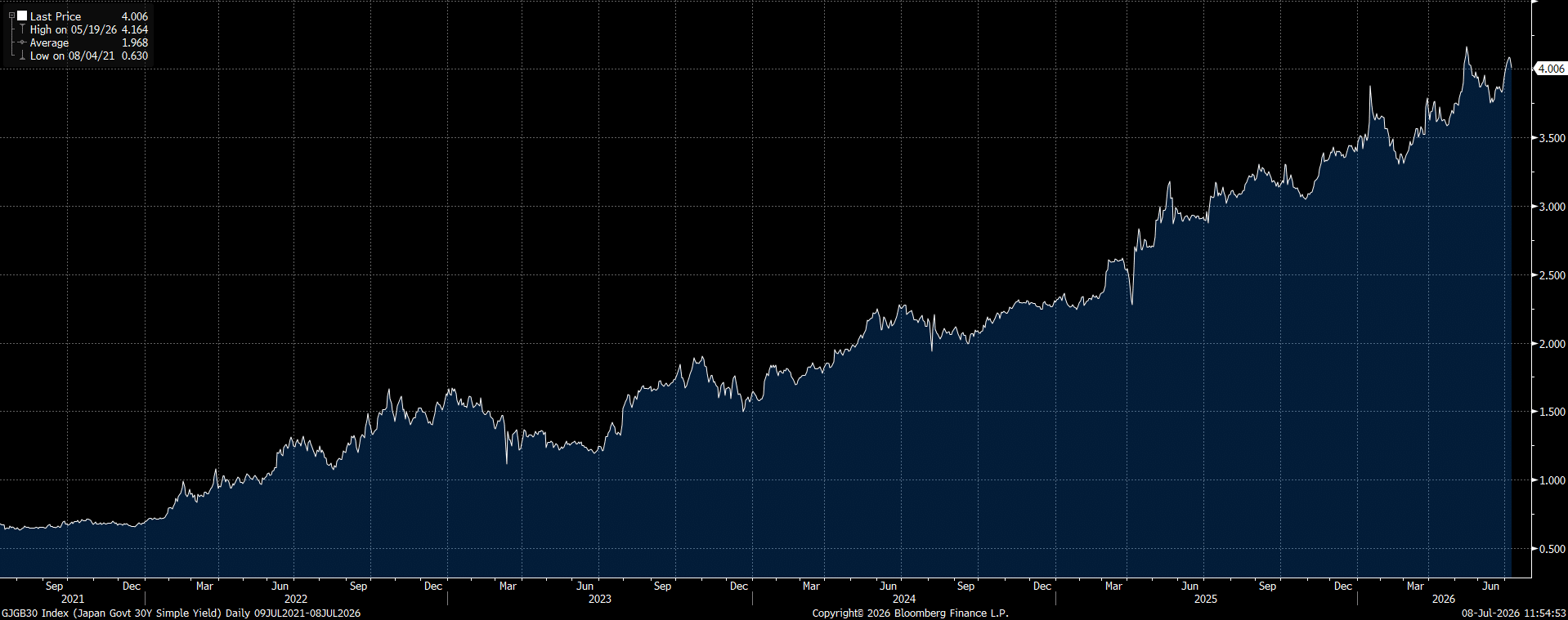

JGBs have sold off hugely since 2021, unlike Western markets, the pace of sell off was initially too slow. Western markets have actually moved little since 2024.

Thanks in part to the BOJ being too slow to move, Japanese bonds continue to fall in price/rise in yields. However, the time to sell was 2021 in my opinion, not 2026.

We started buying late 2025. Previously Japan had been our largest underweight. Value, entry point are of paramount importance to bond investors.

Source: Bloomberg

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. The writer’s views are their own and do not constitute financial advice.

This information should not be relied upon by retail clients or investment professionals. Reference to any particular investment does not constitute a recommendation to buy or sell the investment.

Main image: japan, manuel-cosentino-n–CMLApjfI-unsplash