Sanae Takaichi’s election to the LDP presidency may raise expectations for corporate cash mobilisation, writes Junichi Takayama, Japan Investment Director, Amova Asset Management.

Sanae Takaichi was elected to be the first female president of the ruling Liberal Democratic Party (LDP). This follows the LDP’s two defeats in the national elections over the past 12 months under the previous leadership. This was considered a ‘change of government’ within the LDP (from the left to the right) and the initial reaction in the market was higher stock prices, depreciation of the Japanese Yen and higher government bond yields, the so called Takaichi trade, with rising expectations of higher government spending.

However, forming a coalition to achieve the majority votes in the parliament required to become the prime minister became a struggle after the junior coalition partner Komeito left the coalition amid differing views on political funding and other things. (At the time of writing, Takaichi has been elected the first female prime minister after the LDP formally signed a coalition agreement with the Japan Innovation Party, a center-right, reformist political party).

Behind the news

Behind this historic political victory of Takaichi and the following political turmoil (along with the two Japanese Nobel prize winners announced in the same week) dominating the headlines, there was a significant event which would have been covered more extensively by the media had it not been for these breaking news stories.

This event involves the Taiwanese electronic component maker and a well-known Apple supplier Yageo’s tender offer to buy Shibaura Electronics, known for its competitive sensors, measuring devices and control equipment. This offer will likely be remembered as a watershed moment in the context of corporate governance, and more specifically competition for corporate control in Japan. This deal was unusual in that it was effectively a hostile acquisition by a foreign company which, in the end, the government gave a green light to.

It was October 3, the day before the LDP presidential election that Yageo announced that it had secured enough shares in its tender offer to take control of Shibaura Electronics, which we believe is why the news was not covered more extensively by the media.

However, competition for corporate control is clearly heating up with several ‘hostile’ takeover attempts made after the M&A guidelines were released in August 2023 by the Japanese government in an effort to drive more M&A activity. Some bids succeeded, while in other cases, target companies were eventually acquired at even higher prices by a white knight after a bidding war, benefiting existing shareholders.

Low hanging fruit: Cash-rich companies

Needless to say, in this increasingly competitive environment for corporate control, companies with low valuations, high free float or idle assets (or any combination of these) are among the most vulnerable to unsolicited tender offers.

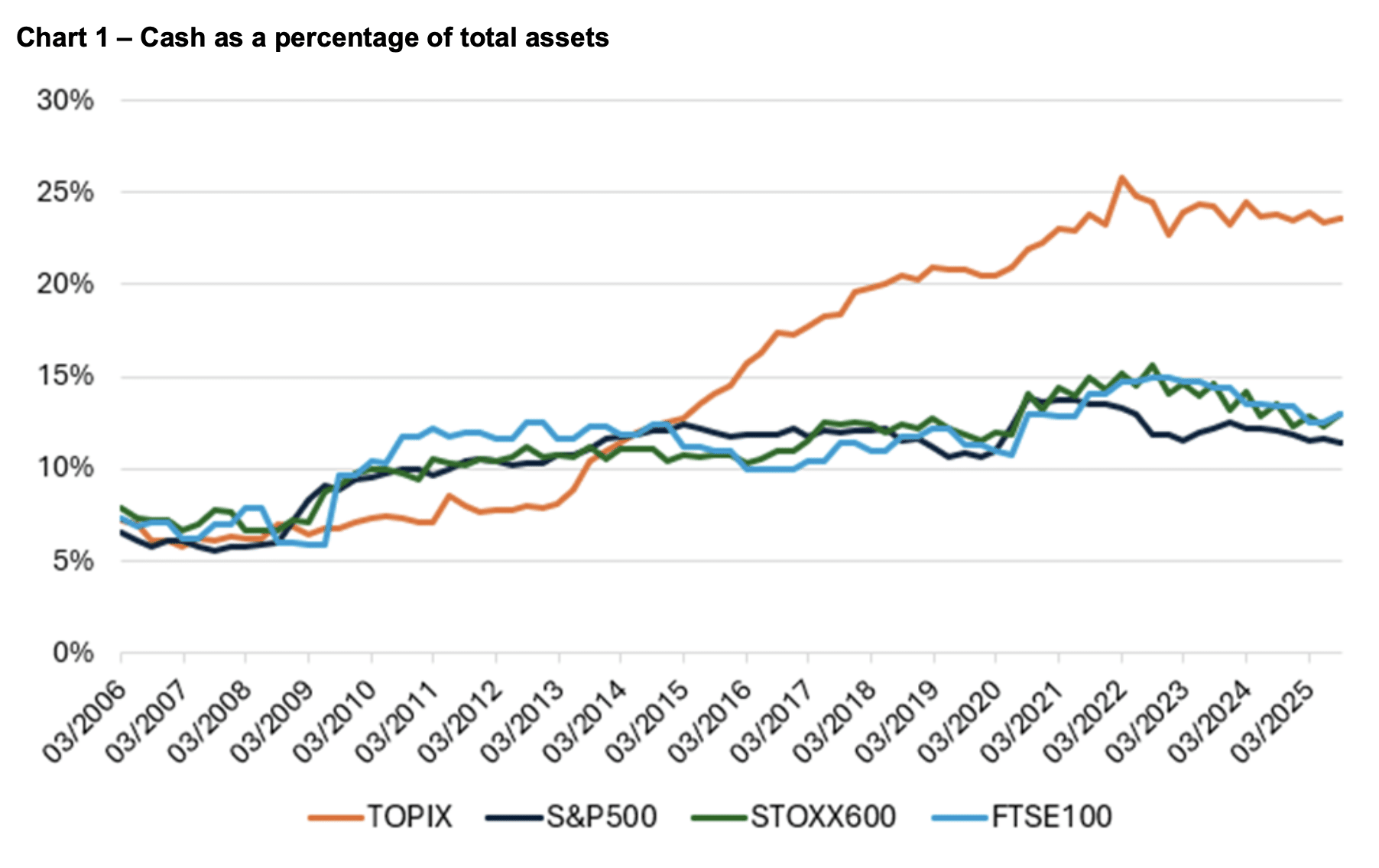

In Japan, the majority of companies listed on the prime market are net cash positive as the management teams have been quite conservative in their financial strategy. Hoarding cash over the years resulted in significant levels of cash sitting on their balance sheets (Chart 1).

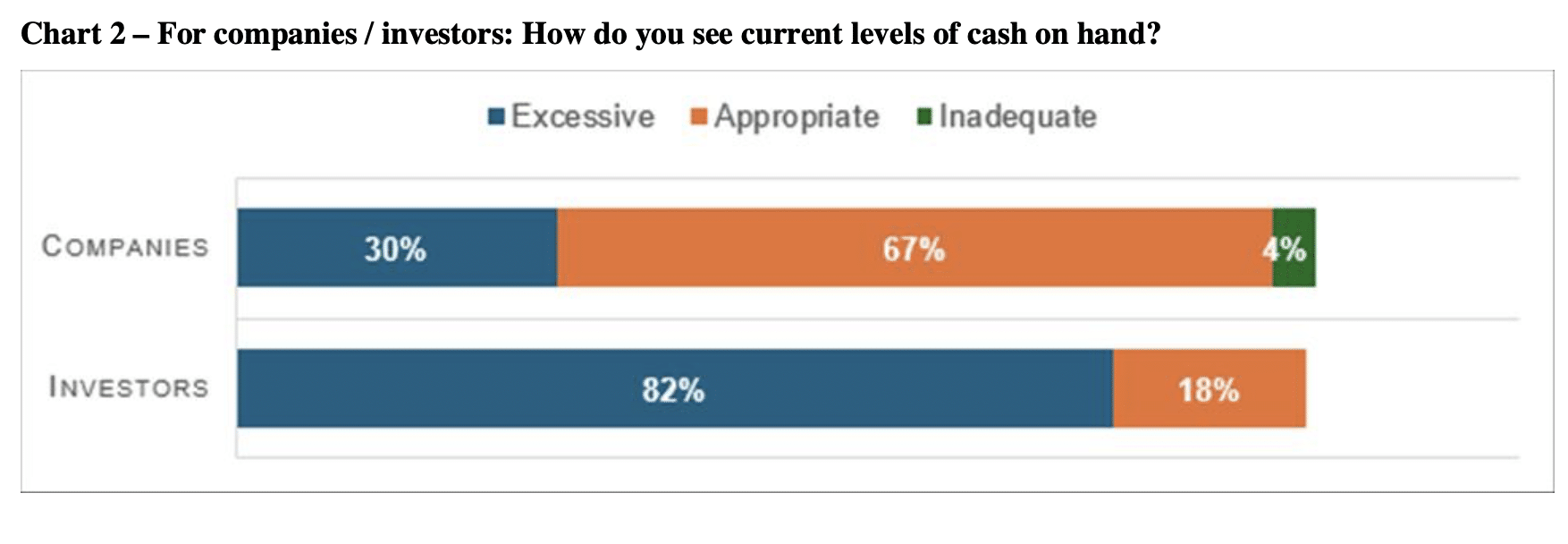

A survey conducted by the Life Insurance Association of Japan indicated that while 67% of companies consider their cash reserves to be at an appropriate level, 82% of investors view them as excessive, highlighting a persistent gap in perception between corporates and shareholders. It appears that there is still significantly more room for companies to improve their capital planning to boost capital efficiency.

More scrutiny on capital allocation on the horizon

According to the Nikkei, the number of companies disclosing detailed capital allocation policies through July nearly doubled year-on-year, reaching 309. Companies have been more mindful of capital efficiency, especially after the TSE’s guidance in March 2023, boosting shareholder distributions to deploy excess cash in recent years but there is more work to be done.

In June 2025, Japan’s Financial Services Agency (FSA) released a document titled “Action Programme for Corporate Governance Reform 2025”, which basically says that a decade after the launch of Japan’s Stewardship and Corporate Governance Codes (in 2014 and 2015 respectively), progress is evident. However, sustainable growth and long-term value creation at companies require more than compliance and that companies and investors must shift from box-ticking to active, strategic governance reform.

Within the document, the FSA specifically mentioned that “Consideration should also be given to clarifying the board’s accountability in verifying whether each company appropriately assesses its current resource allocation, such as whether it is effectively utilising cash for investments (in revising the Corporate Governance Code)”.

On October 6, Bloomberg reported that “Cash-rich companies in Japan may feel the heat after the election win of the pro-stimulus conservative Sanae Takaichi, as she has in the past expressed concerns about excess corporate cash holdings.” Other political parties have also expressed concerns about the growing retained earnings at Japanese companies.

In game theory, a “dominant strategy” is one that yields a higher payoff than any other strategy, regardless of the choices made by other players. In a similar way, we believe that for cash-rich companies, irrespective of future political developments, whether immediate or long-term, utilizing excess cash will benefit them under different political scenarios, making mobilizing cash a “dominant strategy”. Effective use of cash will enable companies to fend off shareholder activists or hostile suitors with higher valuations and less idle assets. Companies will also be able to avoid destroying shareholder value (i.e., avoid yielding real negative returns) amid ongoing inflation, which has now become the norm.

Conclusion

In Japan’s shifting corporate landscape, cash-rich companies are facing growing pressure. Years of conservative financial management have left many firms with large cash reserves, making them increasingly vulnerable to unsolicited bids and hostile takeovers. Investor sentiment contrasts sharply with corporate views – while most companies see their cash levels as appropriate, a majority of investors consider them excessive.

Regulatory bodies, including the FSA, are pushing for more strategic capital allocation. The recent acquisition of Shibaura Electronics by Taiwan’s Yageo underscores the intensifying competition for corporate control. As inflation persists and shareholder activism rises, deploying excess cash is becoming a “dominant strategy” for companies to enhance value and fend off threats.

Regardless of how Japan’s political turmoil unfolds, there will be a growing focus on cash-rich companies, which are likely to mobilize their reserves to enhance value, defend against takeovers, and meet rising expectations for capital efficiency.

Main image: jezael-melgoza-alY6_OpdwRQ-unsplash