Professional Paraplanner’s TDQ (Training, Development and Qualifications) series, is run in conjunction with key support providers, such as Brand Financial Training, and aims to test your knowledge of the financial services market, as part of your overall training goals and exam techniques.

The following questions, which can also be found in our December 2021 issue (Professional Paraplanner December 2021), relate to examinable Tax year 20/21, examinable by the CII until 31 August 2022.

QUESTIONS

1. One of your clients has recently been asked to be a trustee on a discretionary trust which has the bulk of its investment in equities. He is concerned about the taxation of any dividends for the trust and the beneficiaries. You tell him that:

A. the trust is liable for 38.1% income tax after they have exceeded their standard rate band and the beneficiary is deemed to have received trust income not dividend income.

B. the trust is not liable for any income tax and the beneficiary pays an extra 22.5% if they are a higher rate taxpayer.

C. the trust is liable for 37.5% Income tax with the first 10% covered by the tax credit and the beneficiary is deemed to have received trust income not dividend income.

D. the trust is liable for 38.1% Income tax after they have exceeded their dividend allowance and the beneficiary is deemed to have received trust income not dividend income.

2. You are reviewing the financial planning needs of a young couple, Simon and Jess, with two children under the age of 5. What would your general priorities be for them before they considered saving and investment?

A. Pay off all debts and put any required protection plans in place immediately.

B. Pay off expensive debts, protect the family, then put an emergency fund in place.

C. Complete an income and expenditure analysis to determine any surplus income.

D. Put an emergency fund and protection in place first.

3. Helen has made a chargeable gain of £4,500 on the surrender of her non-qualifying life assurance policy. If her taxable income in 2021/22 is £40,000 she will be liable for which of the following taxes on the gain?

A. Capital gains tax at 10%

B. Capital gains tax at 20%

C. Income tax at an extra 20%

D. Income tax at an extra 40%

4. The house-style employed by the investment management firm you work for is based on finding companies with long term sustainable advantage. What is the name given to this particular approach to investment management?

A. Value

B. Momentum

C. Contrarian

D. GAARP

5. Gertrude is considering taking out a home reversion plan but is concerned that if she dies within the next few years her children will lose out financially from the value of her property. What feature should she ensure her plan has?

A. No negative equity guarantee

B. Kitemark guarantee

C. Minimum inheritance guarantee

D. Safe Home Income Plan guarantee

6. Julia, a newly qualified teacher, is in the process of buying her first home near where she works using a housing association’s shared ownership scheme. What is the advantage of her paying stamp duty land tax as a one-off payment?

A. She can receive tax relief on the payment.

B. She will only have a further liability if she utilises staircasing.

C. She will not have a further liability if she buys a bigger percentage of the property.

D. The rate of stamp duty land tax is reduced by 1%.

7. The following investments have been made to a VCT, an EIS and a SEIS:

What is the total amount of tax relief that will be allowed?

A. £62,000

B. £73,500

C. £114,500

D. £116,500

8. How does the role of a Deputy differ from that of an Attorney under a Lasting Powers of Attorney (LPA)?

A. A Deputy is appointed by the Court of Protection whereas an Attorney under an LPA is appointed by the donor

B. A Deputy can make gifts on behalf of an individual whereas an Attorney cannot

C. An Attorney can sell property whereas a Deputy cannot

D. A Deputy must keep financial records whereas an Attorney does not need to

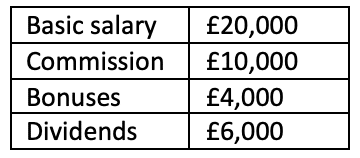

9. Simon, who is a director-shareholder in the business, is retiring in the tax year 2021/22 and will receive a pension based on his 25 years’ service in a 1/60th defined benefit pension scheme. Simon’s total remuneration consists of:

If the scheme’s definition of pensionable remuneration includes all of his earnings as an employee, Simon’s pension will be:

A. £16,667.

B. £15,000.

C. £14,167.

D. £8,333.

10. Which of the following is a feature of a Treasury bill?

A. Very illiquid

B. Issued by NS&I

C. Backed by the Government

D. Long-term maturities

![]()