Sometimes a disposal produces a CGT result that isn’t the one you were planning for, particularly where markets have moved sharply or transactions happen close together. Quilter’s latest article explores some good news, in that the way disposals and repurchases are matched can materially change what gets reported. With the right timing, the 30-day matching rules can turn an unwelcome outcome into something far more manageable.

The 30-day share matching rule is designed to avoid the practice of rebasing gains by selling one day and buying back shortly after, known as ‘bed and breakfasting’.

If you sell shares and then buy the same shares back within 30 days, the disposal is recalculated using the repurchase cost, rather than the original pooled cost, which can change the gain or loss reported.

This rule has a useful side effect, if you act fast enough it can be used to ‘undo’ a gain or loss triggered in error.

Example

- Dan has sold all the units held in a fund in error realising a gain.

- Before the sale he held 30,000 units with an average (pooled) cost of £0.30 per unit.

- The disposal price was £1.31 per unit. Giving him £39,300 proceeds and creating a gain of £30,300.

Repurchase and 30-day matching recalculation

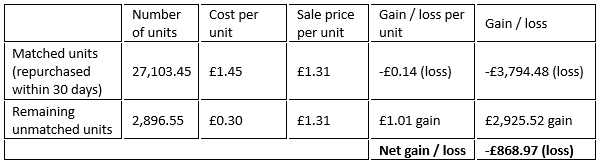

- Dan buys back the same fund using the £39,300 proceeds within 30 days.

- By this time, the fund price has risen to £1.45, which buys 27,103.45 units.

- The 27,103.45 repurchased units are matched against the 30,000 units sold, and the repurchase cost (£1.45) is used to recalculate the gain for the matched units.

- The remaining 2,896.55 sold units are unmatched. The gain on these units is still calculated using the original pooled cost (£0.30).

The re-calculated gain on the sale creates a loss of £3,794.48 and a gain on unmatched units of £2,925.52.

Gains and losses made in the same tax year are offset, this gives us a net position of -£868.97 (loss).

Before you use the on the 30-day rule

You need to buy back the same fund

Funds often have multiple share classes (e.g., bundled/unbundled, income/accumulation, hedged/unhedged).

The 30-day rule only applies if you repurchase the same share class. If that class is closed to new money, you may not be able to correct the disposal this way.

A helpful side effect, not the purpose

The 30-day rule is sometimes described as a way to fix disposals made in error.

It can help, but the result depends on how the fund price moves between the sale and the repurchase, so you can only estimate the outcome in advance.

Price movement can leave a residual gain or loss

In Dan’s example, the fund price rose, which turns the original gain into a net loss under the 30-day rule.

If instead the price had fallen to £1.25, the gain would be £0.06 per unit (overall £1,800) – much lower than the original error, but not a complete reversal.

Switches may create a second disposal

If the error was a switch, you may need to sell the fund bought in error to fund the repurchase. That sale is a separate disposal and can create its own gain or loss.

Summary

The 30‑day rule has a useful side effect, but it isn’t a guaranteed fix. It can reduce or even remove an unexpected gain, but price fluctuations and part‑matching can still leave a residual gain or loss.

It also gets much more complex where more than one fund is involved. When choosing a platform, make sure it includes a CGT calculator to do the heavy lifting.

Main image: tax, calculator, red book, recha-oktaviani-h2aDKwigQeA-unsplash