Stephen McPhillips, technical sales director, Dentons Pension Management Limited looks at unauthorised payments from registered pensions schemes that are SIPPs or SSAS

This article was first published in the March 2020 issue of Professional Paraplanner.

Registered pension schemes enjoy many tax advantages. These can range from tax relievable employer and member contributions through to income tax-free returns, capital gains tax-free growth and beyond that to tax-free lump sums upon taking retirement benefits and inheritance tax-free death benefit payments.

Substantial tax advantages such as these are extremely valuable. They do however, come with conditions. Breaching any of the conditions relating to payments to members and / or employers can be a very costly exercise for the scheme member and / or employer. There can also be implications for the scheme administrator attached to the scheme. This article focusses on “unauthorised payments” to members and employers as they might relate to self invested personal pensions (SIPPs) and / or small self administered schemes (SSAS).

Unauthorised member payments

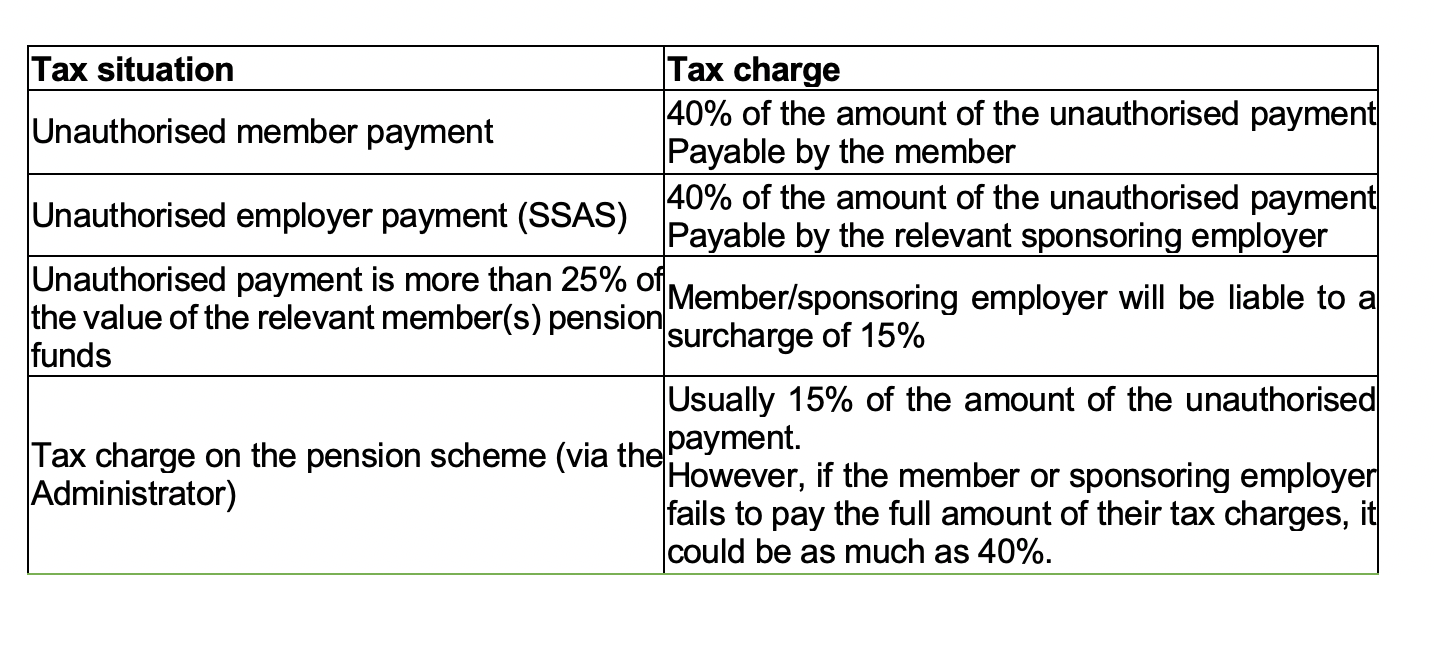

When an unauthorised payment is made to a scheme member, a tax charge of 40% of the amount of the unauthorised payment is levied. This is payable by the scheme member.

If the unauthorised member payment exceeds 25% of the member’s fund value, there is a further surcharge tax amounting to 15% of the unauthorised payment. This is also payable by the member.

In addition, the scheme administrator will usually be subject to a tax charge of 15% of the unauthorised payment. However, this could increase to 40% if the member fails to pay all of the tax charges that have arisen.

It therefore follows that tax charges of 70% (or more) of the unauthorised payment amount could arise where such a member payment occurs.

Examples of unauthorised member payments include:

- A loan directly or indirectly to a member or anyone connected with the member, including a company controlled directly or indirectly by a member.

- Payment of benefits to anyone other than the member whilst the member is still alive.

- Benefit payments to a member before the age of 55 (unless they satisfy the ill health requirements or have a protected lower pension age).

- Value shifting, i.e. where a pension scheme enters into a transaction that increases the value of an asset or decreases the amount of a liability of a member, or a person connected with a member (and in the case of a SSAS, a sponsoring employer), on anything other than what would normally be expected on arm’s length terms.

This is not an exhaustive list and care should be taken to ensure that unauthorised member payments do not take place.

Unauthorised employer payments

When an unauthorised payment is made to an employer, a tax charge of 40% of the amount of the unauthorised payment is levied. This is payable by the employer.

If the unauthorised employer payment exceeds 25% of the member’s fund value, there is a further surcharge tax amounting to 15% of the unauthorised payment. This is also payable by the sponsoring employer.

In addition, the scheme administrator will usually be subject to a tax charge of 15% of the unauthorised payment. However, this could increase to 40% if the sponsoring employer fails to pay all of the tax charges that have arisen.

It therefore follows that tax charges of 70% (or more) of the unauthorised payment amount could arise where such an employer payment occurs.

Example of unauthorised employer payments

A loan from a SSAS to a sponsoring employer that does not satisfy each and every one of the strict requirements for such a loan to be an authorised payment. Such requirements include the fact that the loan must be secured by a First Legal Charge over a suitable asset or assets.

Potential impacts on SIPP and SSAS

Most responsible providers of SIPP and SSAS arrangements will take all necessary and reasonable steps to avoid the occurrence of any such tax charges. In turn, this will often mean that providers will:

- Undertake robust due diligence on any proposed investment which could give rise to unauthorised payments. For example, a peer to peer lending platform might not be acceptable to a provider if the end borrower cannot always be identified.

- Operate a strict company policy on SSAS loans to employers in order to ensure that the five strict HMRC requirements are met in full without any additional complications (such as the SSAS trustees taking possession of any property which could be deemed as “taxable property” in the event of default by the borrower – items such as plant and machinery, stock, etc.).

- Not permit the shifting of any value from one member to another within its arrangements.

Summary table

Total tax charges for an unauthorised payment could be as high as 70% of the amount of the unauthorised payment.