It’s too early to call an end to the growth cycle in 2025, says Naomi Fink, Chief Global Strategist, Nikko Asset Management, but she warns on the tail risks.

As we head towards 2025, anticipation that Donald Trump will implement growth-enhancing policies upon his return to the US presidency is boosting equity markets.

Prior to the US election, the stock and bond markets had priced in contrasting economic scenarios. Bond pricing pointed towards a significant slowdown in growth, whilst equity valuations kept getting richer.

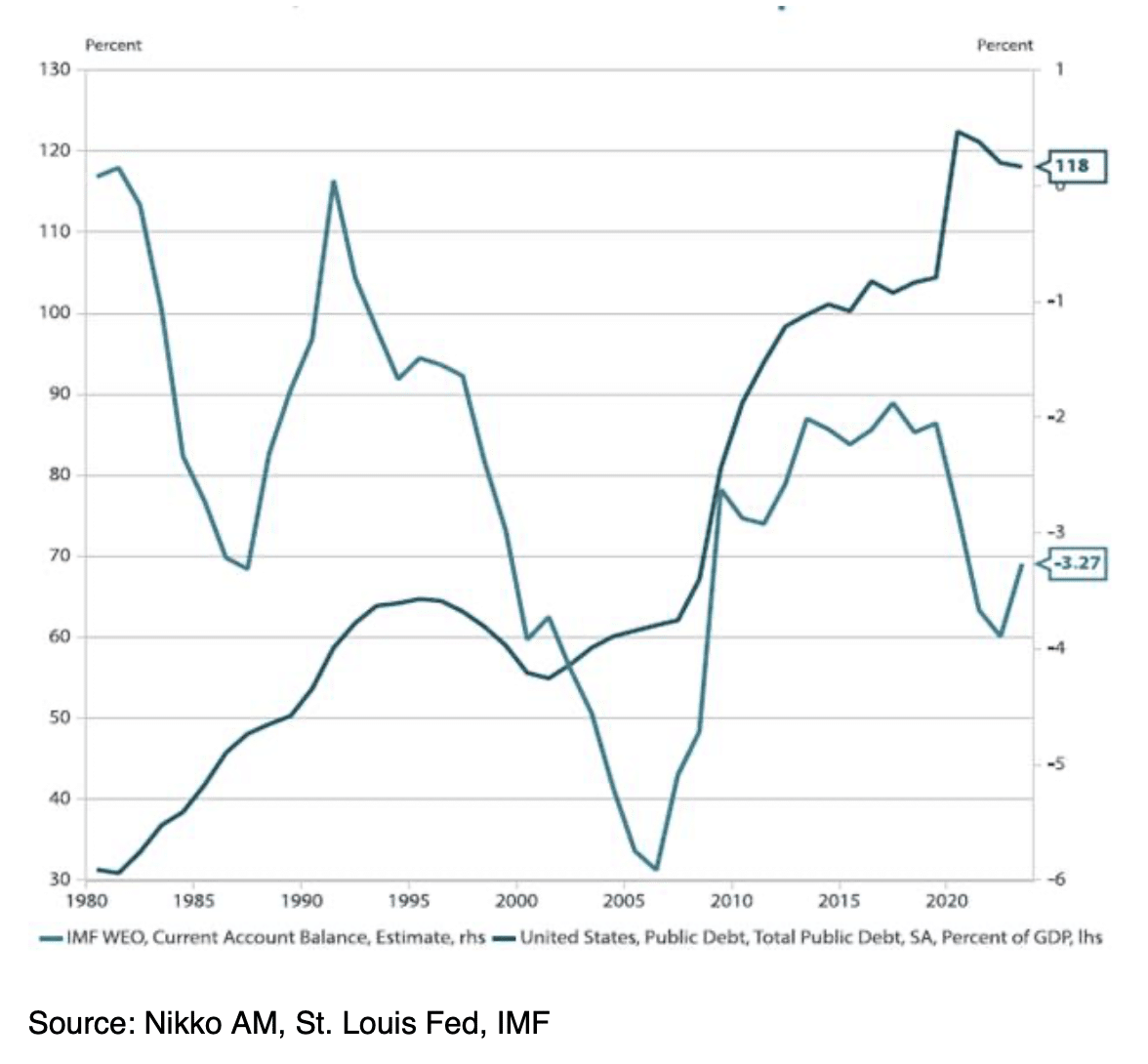

In the short term, Trump’s win put an end to speculation that weak underlying growth would prompt the Fed to cut rates aggressively and rapidly. However, continued caution may be warranted as already stretched US stock valuations have continued extending – even as the US debt-to-GDP ratio has effectively reached historical highs of 120% (see chart 1).

Prior to the election, we had assessed that tail risks, such as disruptions to the US yield curve, had increased but the unexpectedly strong mandate won by the Republican Party has lowered the risk of immediate Congressional conflict over the debt ceiling. However, it has also increased longer-horizon tail risks associated with the anticipated fiscal easing combined with an already stretched US fiscal position.

Chart 1: US debt, current account balance as percent of GDP

Meanwhile, markets outside the US have been factoring in potential disruptions from tariffs and other isolationist policies forthcoming from the US. For example, while Chinese stimulus so far may have been disappointing, Chinese government officials have every reason to wait until they can assess the new US administration’s plans before offering any additional stimulus for domestic demand.

Separately, the October snap election in Japan resulted in a loss by the ruling coalition led by the Liberal Democratic Party (LDP) of its majority. Without a majority the LDP-led coalition has had to compromise with opposition parties. This has led to proposals for fiscal stimulus designed to support lower-income households. These measures have the near-term potential to support domestic demand, even as uncertainty over the impact of US trade policy has tempered the yen’s rebound.

Compared to Europe however, the situation in Japan is still more favourable. Europe, struggling with lagging demand, is dependent on the European Central Bank (ECB) to deliver additional stimulus. This is particularly acute as Europe is gripped by trade uncertainty from the US, a political crisis in France, and by a forthcoming snap election in Germany currently scheduled for February 2025.

Earnings growth robust in the US and Japan, valuations likely peaking

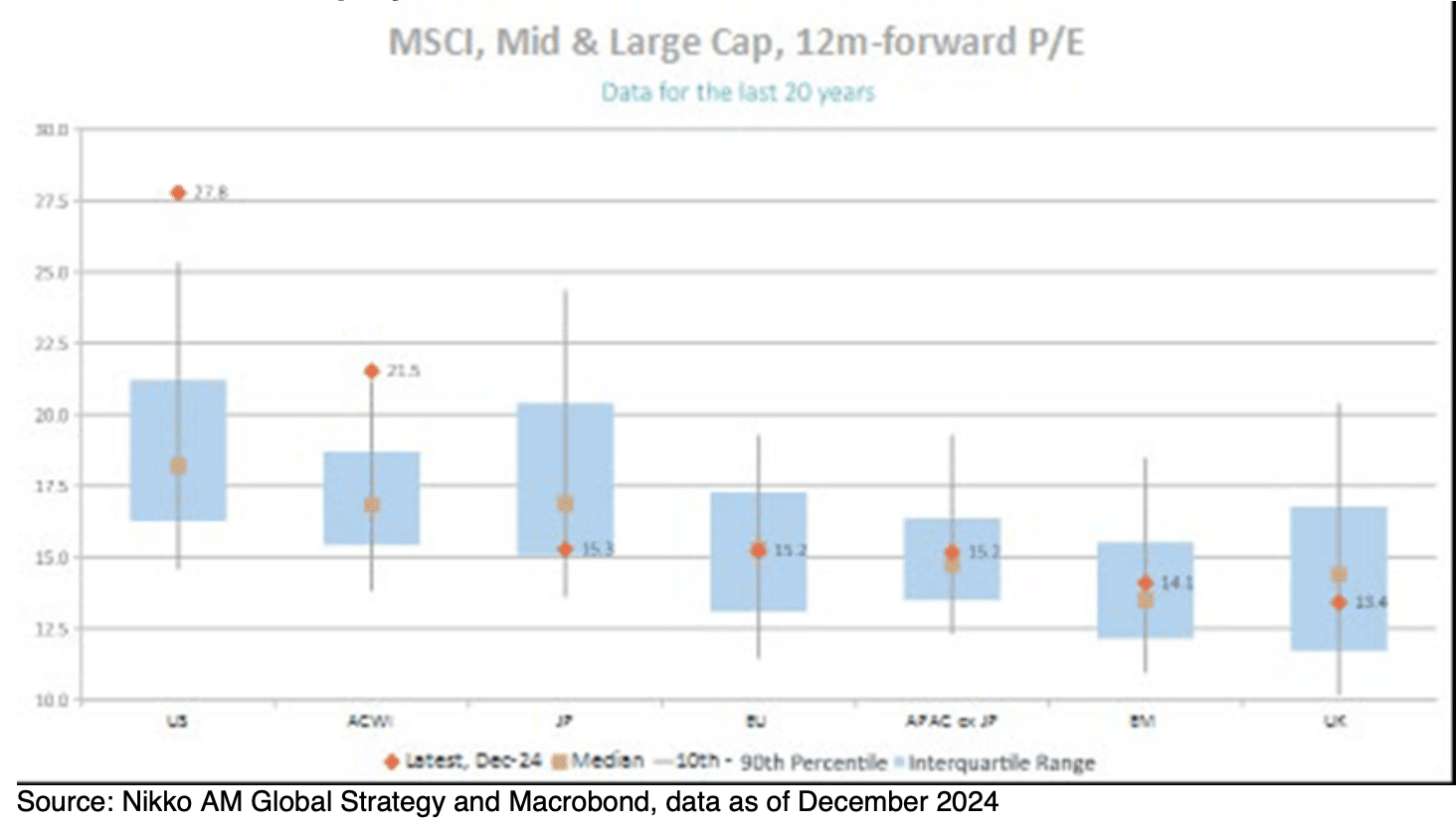

It is undeniable that the US equity markets, which are highly concentrated, are richly valued when historical and geographical comparisons are made. As we see in chart 2, US P/E multiples are far above their recent 20-year range. This is also causing global portfolios to exceed their historical valuation ranges due to the rapidly growing relative US market capitalisation.

Despite this, there are few apparent catalysts to bring equity prices immediately lower. This is largely due to double-digit earnings growth that continues to exceed expectations alongside accommodative financial conditions. For example, US and European credit spreads are near historical lows while the Fed is still cutting rates. Our overall outlook for US earnings remains upbeat but we believe valuations may have peaked, and we expect index gains to lag earnings growth in 2025.

Chart 2: Relative equity market valuation

Meanwhile, we continue to foresee healthy earnings growth driving gains for Japanese stocks despite being at the lower end of their 20-year valuation ranges and likely to remain relatively flat over 2025.

US valuations will likely remain higher than global counterparts over the near-term horizon whilst we expect European earnings to remain mired in the low single digits, possibly even turning negative as growth in the region remains sluggish and the consequences of future US tariffs are as yet uncertain.

For UK and Australian stocks, we believe there is a reasonable probability that earnings growth will fall into negative territory at some point during 2025, with valuations unlikely to rise beyond average historical levels.

The Hang Seng, which is driven by internet stocks and financials, may receive a modest boost from ongoing tech sector interest and the possibility of stimulus from China in response to US protectionism over the course of 2025

In light of these factors, we have upgraded our near-term economic outlook for the US and anticipate Japan’s “virtuous circle” to remain intact. We expect the Fed’s rate cuts to date to enhance already accommodative financial conditions in the US. Predicting the timing of any cyclical market downturn remains challenging but we would highlight heightened tail risks associated with policy disappointments in the US as an area to monitor. We continue to see risks as biased towards the inflationary, and believe expansionary US fiscal policy is ultimately unsustainable.

The ongoing cycle extension, along with upside risks of inflation, supports holding stocks which may help protect the future purchasing power of investors. In contrast, the upside may be limited for bonds, notably US bonds despite good alternatives to US assets currently limited when considering the political instability in other major economies such as France, Germany, and South Korea. It is currently unclear if these sources of instability will intensify or peter out, therefore we would avoid doubling down on areas affected by heightened political risk.

The current situation notwithstanding, we continue to favour assets that provide diversification hedges against US market risk. Despite its low yield, we see the yen as a risk haven that is likely to offer downside protection in the event of an equity market correction. We continue to favour gold, as well as rotating exposure towards Japanese domestic demand-related stocks. These stocks show signs of sustainable structural recovery and are less correlated with US growth and stimulus than Japan’s export-oriented firms.