This recovery is not V-shaped, or synchronised, says Anthony Rayner of the Premier Miton Macro Thematic Multi-Asset Team.

For some time, we have expressed doubts as to a V-shaped recovery in economic activity. A massive policy response and stockmarkets performing the ‘perfect V’, with many now close to their pre-downturn highs, encouraged the V narrative. However, policy can only do so much and economies are not stockmarkets.

In the US, for example, big tech has driven markets higher. They were index heavyweights before the crisis and have benefited during the crisis for well-documented reasons. Indeed, markets have been less held back by traditional cyclicals like financials and industrials which have performed less well, in part due to the tepid economic recovery. Covid-19 was unlikely to be a one quarter event.

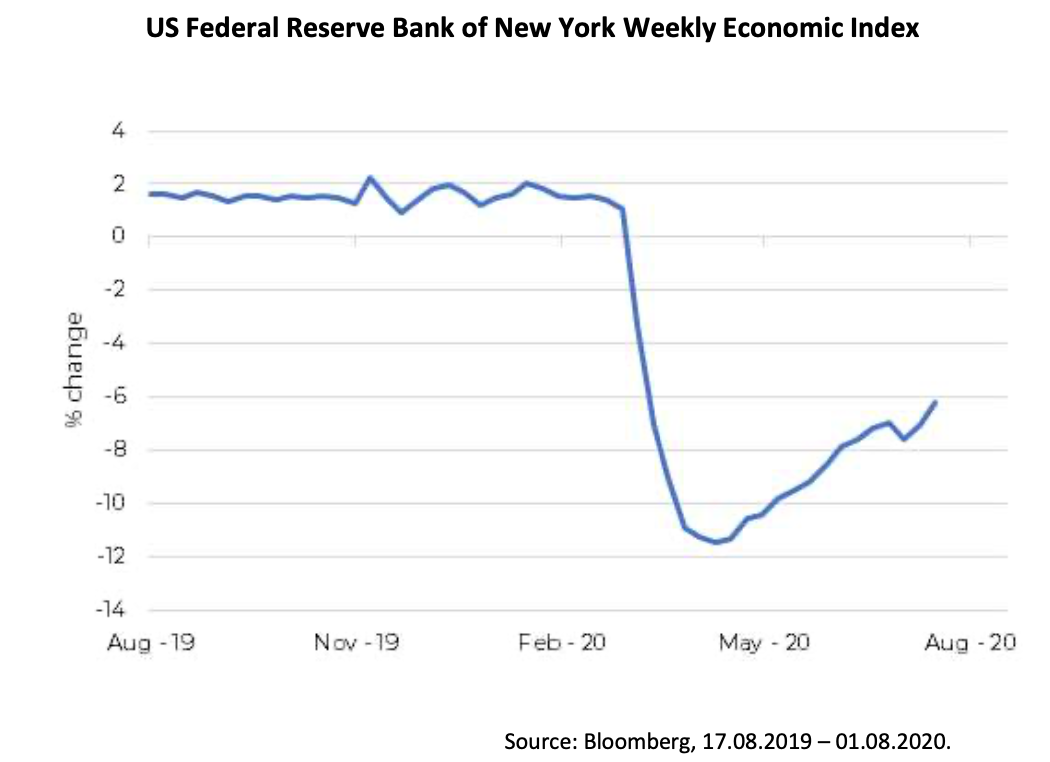

The lack of V rebound in economic activity is well illustrated by one of the more timely economic data series, namely the US Federal Reserve Bank of New York Weekly Economic Index, which is updated twice weekly, and is designed to reflect US GDP growth rates. It is clearly not a V.

It’s a good reminder as to the limitations of forecasting. It’s rarely simple and we think it’s OK to say visibility is poor, when it is, and especially when emotional response mechanisms are elevated, such as in recent months, or around the Brexit referendum for example.

Digging down further into the data shows that, not only is it not V-shaped, but also that economies are experiencing wildly different recovery paths. These are much better illustrated via alternative high frequency data points now available through big data analysis, which suggests that we are seeing multi-speed recoveries. As an example, looking at indicators like vacancies or consumer spending (see FT website “Pandemic crisis: Global economic recovery tracker” for this and other tech-driven data analysis), the UK is faring much worse than most of its peers so far.

So, it’s not a V and it’s not synchronised but what does this mean for multi-asset portfolios? Our base case remains lower for longer, but where economic and policy risk is high. Therefore, for equities, our preference is fairly defensive, and this means traditional defensive stocks like utilities and consumer staples, as well as quality growth companies where earnings are more visible, such as our themes. Similarly, we tend to avoid the traditional cyclicals, such as banks, oils and materials. For bonds we are keeping interest rate risk and credit risk pretty low. Gold has been trimmed but remains a significant position, reflecting the higher economic and policy risk.