With the bond market making a comeback, for this month’s three-year track record focus, Juliet Schooling Latter, research director, FundCalibre, talks to the Grace Le, co-manager with Stephen Snowden, of the Artemis Corporate Bond fund.

Last year was an annus horribilis for corporate bonds, as a sharp rise in inflation caused by the conflict in Ukraine compounded the uncertain backdrop from the existing Covid supply chain issues. That’s without discussing the damage from the most inept mini-budget in history.

The result was a 19 per cent fall for sterling corporate bonds – the worst in history and more than double the 9 per cent loss made during the Global Financial Crisis in 2008*. This was caused by the unusual anomaly of gilts and credit spreads rising – the last time this happened was 1999**.

But the old saying goes that it is always darkest before dawn – and opportunities are appearing.

“On the one hand you are getting paid some of the highest yields to own the index, while on the other hand there is less downside and interest risk.”*** That’s the view of Artemis Corporate Bond co-manager Grace Le.

Grace says investment-grade yields have now readjusted meaningfully relative to other asset classes’ yields. Having also been very cautious on valuations in the government bond market at the start of the year, she also says they are now seeing pockets of value emerging***.

Attractive valuations are only part of the argument – because of falling bond prices, investors can now buy a bond below its redemption value. Essentially, a bond is valued at 100 – meaning an investor gets 100 per cent of the loan back when a bond matures. Investors can buy these bonds at 90 per cent and get back 100 per cent at the maturity of the bond – giving them downside protection. A rare occurrence not seen since the GFC****.

The investment grade sector is home to some of the strongest companies in the world – Covid actually proved that. You would’ve expected many companies to struggle to fund debt in that environment – but the opposite was true, with companies buying back debt. In the last quarter of 2022 we saw General Electric, GSK, Tesco Property, HSBC and TFL all buy back their bonds****.

“Investors are also taking less interest rate risk. The combination of higher yields, lower risk of capital and lower interest rate risk is attractive. It’s rare these stars align. The index now yields 5.5 per cent,” adds Le.

Artemis Corporate Bond was launched by bond veteran Stephen Snowden in October 2019. He had joined from Kames earlier that year. Grace also joined from Kames in December 2019 – where she was co-manager on a number of investment grade mandates – becoming co-manager of this fund in March 2020.

The managers target corporate bond opportunities at various stages of the economic cycle – analysing markets from a top-down and bottom up perspective, evaluating fundamentals and the outlook for inflation.

Corporate profitability and management strategy are also assessed, with the team evaluating any factors hindering or improving the company’s competitive positioning and any downside risks. Valuation then comes into play. Sector sentiment is also analysed, including structural changes potentially impacting certain sectors. The team focuses on UK, US, and European issues, with at least 80 per cent of assets in or hedged back to sterling.

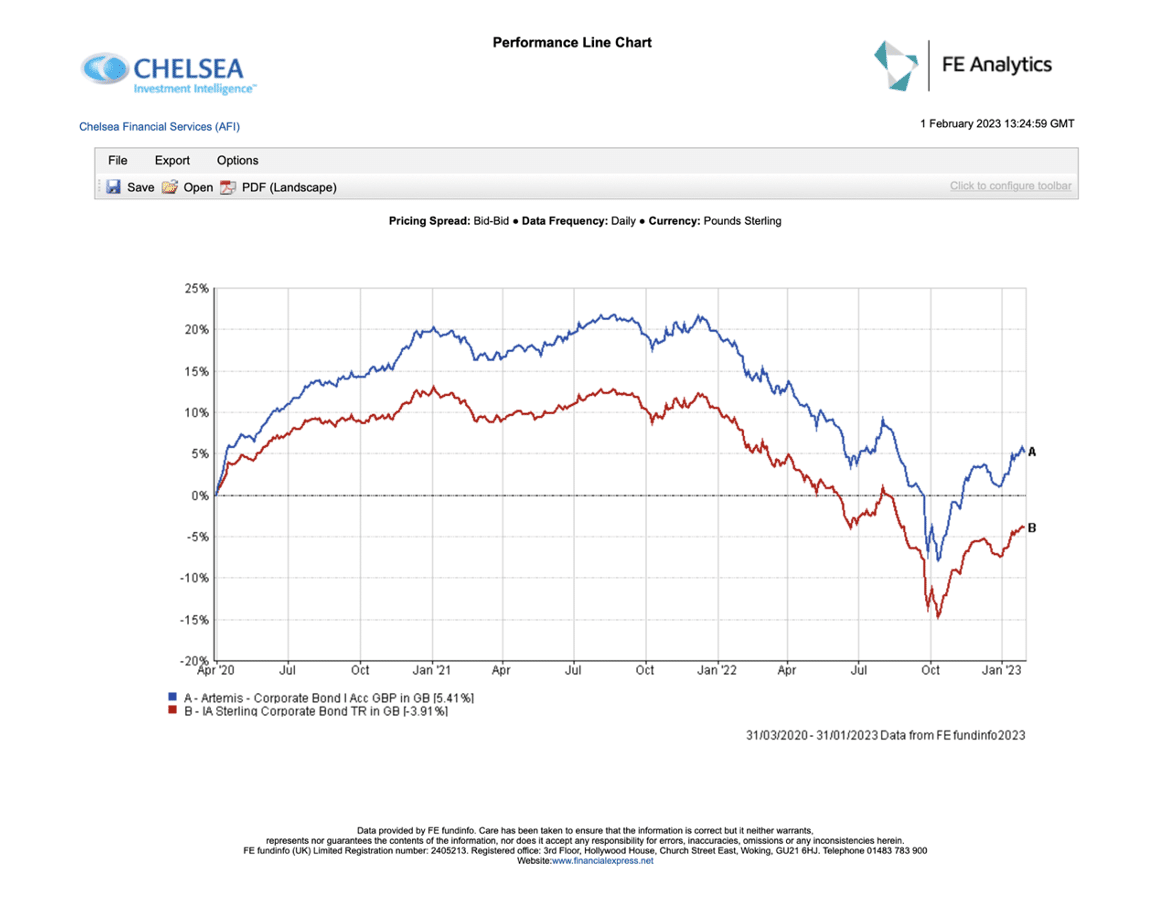

The final portfolio is around 75-150 holdings – to put this into context the average for their peers is 300^. This strong active approach has helped the fund. It has outperformed the index by 11.2 percentage points^^ – outperforming in 31 of 38 months since launch***.

A good example of this was during Covid, when Grace says we saw a strange sell-off in stable credits like utilities and telcos.

She says: “The volatility and market inefficiency allowed us to sell riskier investments – and buy housing associations, utilities, and pharmaceuticals without giving up yield – as some of these areas sold off the most. This is because they are all components of the passive index, so when lots of money comes out, passives sell a bit of everything – even stable companies.***”

In hindsight, she says the fund launched at the worst possible time, but while the team could not predict the likes of Covid, war in Europe and rapidly rising inflation, they are able to make active decisions to take advantage of those changes. Looking to the future, she says: “While I can’t tell you how bad inflation or recession will be, we will be able to be active and take advantage of those moves in the market.***”

The managers have shown themselves to be excellent stock pickers – combining this with a long-term strategic and thematic view of where to tilt the fund, while also capitalising on short-term opportunities. The combination of macroeconomic analysis and fundamental due diligence ably prepares them to manage any economic climate.

*Source: Bloomberg, returns for Sterling collateralised and corporate returns, 31 December 2022

**Source: Artemis: Fixed Income: 2023 could be very attractive for bond investors

***Source: Artemis webcast: Why not could be a great time to invest in corporate bonds – January 2023

****Source: Artemis Corporate Bond fund update – 20 January 2023

^Source: Source: Morningstar, 31 December 2022. All funds classified as ‘GBP Corporate Bond Fund’ excluding tracker funds

^^Source: Artemis Corporate Bond presentation, 30 October 2019 to 31 December 2022

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. Juliet’s views are her own and do not constitute financial advice.