If you’ve got clients with annual allowance tax charges it pays to be ahead of the curve, not least because your clients may have less time to play with than they think. Martin Jones, technical manager at AJ Bell, highlights the key dates to put in your calendar, in particular with regard to Scheme Pays.

Pension Saving Statements

The first date on our timeline is 6th October. This is the deadline by which providers are required to send ‘pension saving statements’ to:

- members who have paid in more than the standard annual allowance of £40,000 and;

- members who have triggered the money purchase annual allowance and paid in more than £4,000

It might be this that’s prompted your client to get in touch. You might also have clients who haven’t received one but still have a charge to settle. This could be because they’ve contributed more than the annual allowance across two or more pension schemes. Or they could be subject to a lower annual allowance thanks to the tapering rules.

Even if they haven’t received a statement, they still have a responsibility to be aware of what they’ve contributed (or accrued, if we’re talking Defined Benefit schemes) and to pay any charges.

Paying the charge

In terms of settling the charge, the client may have a choice. They can pay it via their self-assessment tax return, or they may be able to pay it from their pension scheme using Scheme Pays.

There are two types of Scheme Pays: compulsory and voluntary. Broadly speaking, if the client has paid in more than £40,000 to a pension scheme and incurred a charge of more than £2,000, they can use compulsory Scheme Pays to pay the charge from that scheme. Here, the scheme administrator becomes jointly liable for the charge.

If those conditions aren’t met – for example if they paid more than £40,000 across two schemes, or it is the tapered annual allowance or money purchase annual allowance that they have exceeded – the client remains solely liable, but they can use voluntary Scheme Pays, assuming the scheme allows it.

Either way, the client has to make a formal notification to the scheme administrator. They must also remember to include the tax charge on their tax return. The key point in terms of timing is that the two versions of Scheme Pays run on very different schedules.

Voluntary Scheme Pays

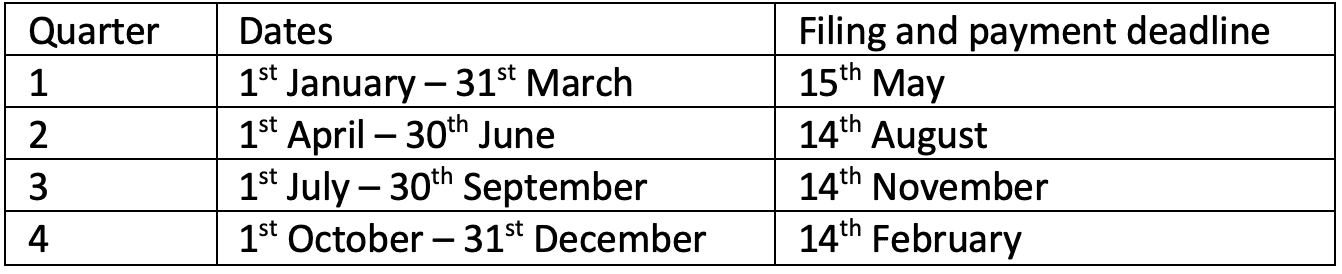

The scheme administrator reports and pays the annual allowance charge to HMRC via the Accounting for Tax (AFT) return. This is a quarterly return and runs on a specific schedule, with the filing dates as follows:

If a client is paying via voluntary Scheme Pays, they would need to submit the notification by 30th September to be fully assured of getting the tax charge paid on time. The scheme administrator would then pay it to HMRC by 14thNovember. Although note that some scheme administrators might have an earlier cut-off point.

If it’s the pension savings statement that’s prompted your client to look at this, they will already have missed this date. In which case, the next date is the Q4 end date of 31st December.

If the tax charge is included in the AFT for Q4, it has a chance of being paid by the self-assessment deadline of 31stJanuary. Again, this will depend on the administrator’s internal procedures – some might file the AFT in early January, some might file it close to the mid-February deadline.

The charge would at least be paid though, and the worst-case scenario is that the client incurs 14 days of late penalty charges (assuming HMRC wants to pursue it).

Perhaps the key point here, however, is that if a client were to submit the notification to the scheme administrator in January, it wouldn’t be unreasonable for them to think they’d got the charge settled in time.

That’s not the case given the scheme administrator has to work to the AFT timescales and the charge wouldn’t get paid potentially until 15th May. In the meantime, the client could be incurring several months of late payment charges.

Compulsory Scheme Pays

The timeline for compulsory Scheme Pays, however, is much more generous.

The client has until 31st July the following year to make the notification to the scheme. So, for a tax charge in the 2021/22 tax year, this would be 31st July 2023

Furthermore, the charge doesn’t need to be paid until the AFT return for the quarter ending 31st December. As it’s compulsory Scheme Pays, the client won’t incur any late payment penalties from HMRC.

The bottom line is that Scheme Pays is a really useful function that lots of clients benefit from. But, as with many pension processes, it pays to plan ahead.

[Main image: etienne-boulanger-mDOao83l1iU-unsplash]