Julia Peake, Technical Manager, Nucleus Financial explains how paraplanners can add value when asked this type of question.

A question we’re frequently faced with when clients have additional monies for investment is which tax wrapper or investment is best. The decisions and recommendations given, will be dependent on a number of, sometimes competing, factors and this is where working with financial services professionals can really add value to clients helping them achieve their investment goals.

Some of these factors are:

- What is the time horizon for investment? For short or longer term investments consideration will be required to the underlying assets, risk appetite, accessibility, reporting requirements and taxation applicable both during the investment term and when you want to draw from it.

- Taxation status of the client now and in the future? Are they likely to move up or down a tax band when they want to take benefits from their investments?

- Purpose of investment? Is this for income, tax efficient withdrawals or for growth?

- Who are the beneficiaries? Is this to pass down to future generations? Do you need access to this during your lifetime? Is this a charity investment? Is this a company investment?

- What’s the family dynamic? Can you make use of spousal exemptions or the “no gain, no loss” disposal for Capital Gains Tax purposes and equalise assets potentially increasing household income if there is a disparity in the rates of tax spouses pay?

- Single or joint investment- is there an imbalance in the attitude to risk?

- How will the investment be managed? By the client, by the financial adviser or a professional investment manager

- Allowances used? What tax allowances have been used this tax year? What is available to offset against potential taxes if we are to make recommendation to the current investments held?

- Are they restricted by what they can invest? Annual allowances, tapered annual allowance, subscription limits or minimum investment value?

This is where your skill and diligence can add value to clients. Collating all this information and making recommendations that are suited to them is a benefit not everyone fully appreciates until they need it.

Once the recommendations have been discussed and agreed, for those clients who have existing investment bonds, who have made pension contributions and ISA subscriptions, depending on their personal circumstances for this tax year, we are often asked if additional monies should be invested in their existing bond or a new one created. Again, this depends on the client circumstances but here are a few points to consider as well as a case study, to help highlight some considerations:

- Investment bonds are created by hundreds or even thousands of individual and identical policies.

- When you add money to an existing bond, you will add to existing polices rather than creating new one in most cases.

- Adding or removing a life assured after the policy has been set up, would trigger a chargeable event so consideration should be given to the set up of the bond and the basis it is written on.

- So, if you have addition monies from say a sale of a business, inheritance, savings then is it best to top up an existing policy or create a new one?

Case study:

- Rachel and her brother John have inherited monies from their deceased Aunt of £75,000 each.

- After speaking to their financial advisers, they decide that an investment bond is suitable for each of them.

- Each open an offshore investment bond on 1 August 2024 and invest the money for their similar attitudes to risk.

- 7 years later their father passes away and each of them receive cash of £75,000.

- They speak to their advisers about what they should do, each of their bonds is now worth £100,000.

- After seeking advice, Rachel add her £75,000 to her existing bond whereas John opts to open a new bond.

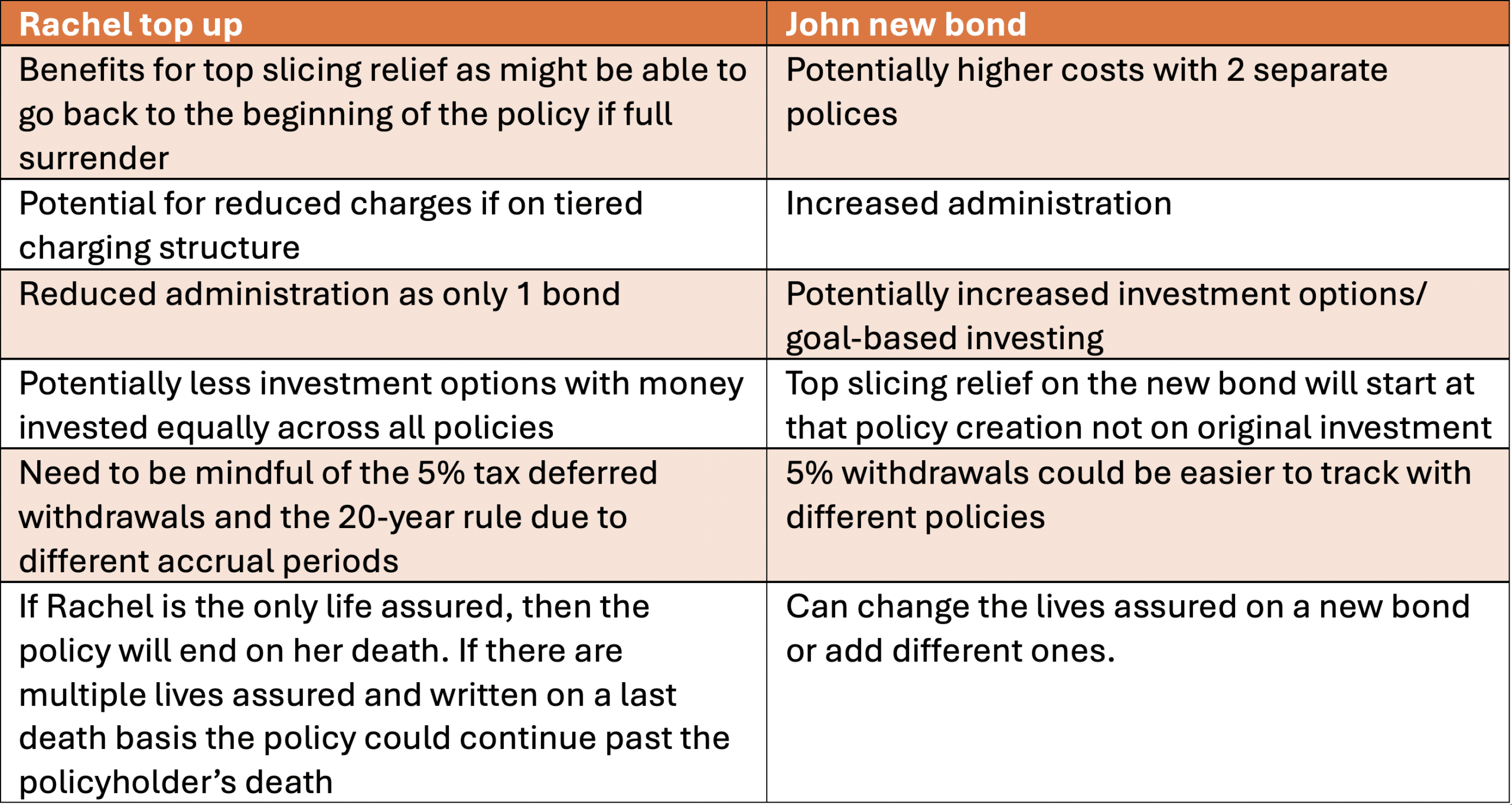

What are the considerations and differences between Rachel’s and John’s strategies?

This is for individuals. If they were considering trusts, then depending on the type of trust it could be more suitable for both to do 2 new bonds and 2 new trusts.

This is because of the effect of cumulative gifts against the nil rate band for lifetime gifts to relevant property trusts and the fact that adding to existing trusts could mean potential entry charges. Additionally, additions to trust will need to be included in the value of the trust for the 10 year principal charge calculation which could also affect exit charges on distributions to beneficiaries.

With every recommendation, considering the whole picture, discussing the pros and cons and proposing what is best for individual circumstances is where you can be a real benefit for your clients.