Japan is entering an exciting new phase in its economic cycle, with several advantages that distinguish it from other major markets according to Naomi Fink , Chief Global Strategist and Junichi Takayama, Japan Equity Investment Director at Amova Asset Management.

A mandate for political change provides greater policy latitude

Japanese Prime Minister Sanae Takaichi, who came into power after the political upheaval of last year, has consolidated her standing after her ruling party won a landslide victory at a recent snap election.

The markets may still be working through the implications of Takaichi’s strong standing, but a solid parliamentary majority means that the Takaichi administration now has leeway to implement policies with a longer time horizon.

It also reduces the pressure to focus solely on short-term measures and makes it easier to pursue policies that support the economy over the medium term.

There is clearly the potential for fiscal stimulus, which could provide near-term support for the economy.

At the same time, the bond market has already signalled some caution about Japan’s longer-term fiscal discipline, so policymakers will need to balance short term support with credible long-term responsibility.

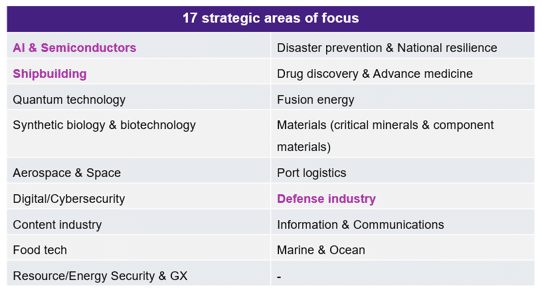

Japan’s strategic areas of focus

Takaichi has placed economic security at the centre of the country’s competitiveness strategy. Last November, the government outlined a broader growth strategy focused on 17 strategic sectors (Chart 1), including AI, semiconductors, shipbuilding and defense.

These investments are framed as both economic policy and crisis management, supporting Japan’s growth while also strengthening the resilience of supply chains.

Many of these areas build on existing strengths. In particular, Japan is home to many companies playing critical roles in the global AI supply chain.

They may not be widely known to the public, but several occupy near oligopolistic positions in specialised components and equipment, which gives them a strong strategic footing.

Chart 1: Japan’s 17 strategic areas of focus

Source: Amova Asset Management based on documents from the Cabinet Secretariat of Japan

Could physical AI become an area of dominance?

The idea of ‘physical AI’ is particularly interesting in this context. Much of the public discussion focuses on humanoid robots, but Japan’s real strength lies elsewhere.

Japan has long been dominant in industrial robotics and automation. These systems are not headline-grabbing, but they are essential components across many global supply chains, including advanced semiconductor manufacturing and packaging.

That position gives Japan control over critical parts of the industrial AI ecosystem, with relatively limited competition and strong global demand.

Physical AI may not generate the same hype as other areas of artificial intelligence, but it has the potential to play a significant role in driving productivity, both in Japan and across its trading partners.

Sector to watch: Defence

At the sector level, rising geopolitical tension is driving higher defence spending, both within East Asia and more globally, making defence a structural growth area.

Since fiscal year 2023, the Japanese government has been doubling the national defence budget to 2% of GDP, a target likely to be raised over the medium term.

Moreover, Japan’s defence industry is well positioned not only to supply the growing domestic market in Japan but also to increase exports of equipment to key national security allies.

For example, in August last year, Mitsubishi Heavy Industries won a highly competitive tender from the Australian government to supply its upgraded ‘Mogami’-class frigates, in a deal reported as being Japan’s largest-ever defence export contract in more than a decade.

In addition, there is further growth potential for some suppliers of defence technologies that have dual-use applications.

Historically, industrial policy in countries such as Japan, the US and across Europe has often produced innovations that later drive productivity gains in the wider economy.

Japan’s cash-rich companies remain “low hanging fruit”

Despite the strong performance of Japanese equities in recent years, there are still some areas of untapped value in the market.

Years of caution have left substantial cash sitting on corporate balance sheets.

As Chart 2 demonstrates, companies listed on Japan’s Prime market continue to hoard large cash reserves, and a significant share still trade below book value, leaving scope for further re-rating as governance reforms and capital discipline take hold.

Yet there remains a clear gap between how companies and investors view cash reserves.

A survey by the Life Insurance Association of Japan found 67% of companies believe their cash holdings are appropriate, while 82% of investors view them as excessive.

This suggests there is still significant room to improve capital allocation and balance sheet efficiency.

Pressure for change is already building. According to Nikkei, the number of companies disclosing detailed capital allocation policies had nearly doubled year-on-year to 309 by July 2025.

This follows guidance issued by the Tokyo Stock Exchange in March 2023 aimed at improving capital efficiency and encouraging companies trading below book value to act.

The momentum is set to continue, with the Financial Services Agency and Tokyo Stock Exchange currently working through a further revision of Japan’s Corporate Governance Code, targeted for completion around summer 2026.

Chart 2: Cash as a percentage of total assets

Source: Amova Asset Management based on Bloomberg data as of December 31, 2025

Japan’s equity market still offers plenty for investors

Japanese equities have served many global investors well over the past few years.

The market has benefited from a strong macro backdrop alongside a wave of corporate actions that have acted as catalysts for re-rating.

What is changing now is the breadth of the opportunity. We see opportunities in small and mid-cap companies, where there remains a large universe of under-researched businesses.

Many of these are niche global leaders with strong pricing power and significant market share in specialised industries, and a growing number are improving their returns on capital.

Japan is entering an exciting new phase in its economic cycle, with several advantages that distinguish it from other major markets.

There will inevitably continue to be periods of volatility as geopolitical tensions play out, but we would argue that the key point for investors is to focus on the direction of travel.

In Japan’s case, the underlying trends still appear to be upward.

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. The writer’s views are their own and do not constitute financial advice.

This information should not be relied upon by retail clients or investment professionals. Reference to any particular investment does not constitute a recommendation to buy or sell the investment.

Main image: Japan, su-san-lee-E_eWwM29wfU-unsplash