As we get ever closer to April 2027 and unused pension funds form part of the estate for IHT purposes, the need for effective IHT planning has never been greater. Many clients will be seeking guidance on how best to manage their wealth and legacy. Here, Quilter look at the 10% rule when it comes to bequeathing gifts to a registered charity.

A powerful yet often overlooked strategy is to include a gift to a registered charity in a will. This simple act will not only leave a positive legacy but can help to reduce the IHT burden on the client’s estate.

There are two ways in which charitable legacies can reduce IHT:

- The charitable gift is exempt from IHT – thereby reducing the taxable value of the estate

- Where 10% or more is left to charity, the rate of tax applicable to the taxable estate is reduced from 40% to 36%.

By understanding the ‘10% test’ you can help your clients ensure their legacy benefits their loved ones and charitable organisations, all whilst optimising the IHT efficiency of their estate.

The 10% test

Let’s see how the 10% test operates by sharing a couple of examples. Before we delve into the calculations, it is important to clarify some key terms that underpin inheritance tax calculations involving charitable legacies:

Survivorship component – joint assets (joint tenancy) that pass automatically to the surviving co-owner.

Settled property component – assets for which the deceased was beneficially entitled to for example the life tenant of a qualifying interest in possession trust.

General component – the rest of the estate except the survivorship and settled property components as well as any property for which a gift with reservation (GWR) exists.

Available nil-rate band – Currently £325,000, increased by any transferable nil-rate band (TNRB) but reduced by previous chargeable lifetime transfers (CLTs) in the 7 years prior to death. This does not include any residential nil-rate band or transferable residential nil-rate band that might be available on the estate.

Donated amount – the amount gifted to charity in the will.

Baseline amount – the figure used to test whether the 10% threshold has been met. It is calculated in three steps:

Step 1 – Establish the chargeable transfer for each estate component.

Step 2 – Deduct the appropriate proportion of the available nil-rate band.

Step 3 – Add back the charitable legacy deducted at step 1 to arrive at the baseline amount.

Examples:

1. Straightforward estate that qualifies

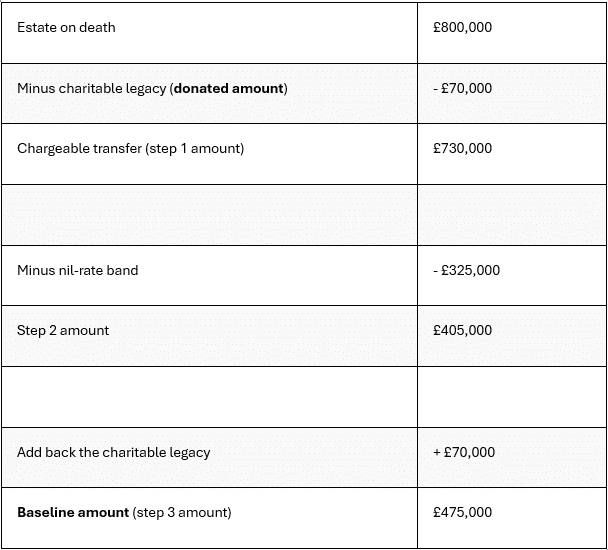

Sarah died on 17 June 2024, leaving an estate valued at £800,000 after liabilities. She left a legacy of £70,000 to the National Trust.

The donated amount of £70,000 comfortably exceeds 10% of the baseline amount of £475,000 (£47,500), which means the estate qualifies.

Sarah’s estate therefore pays £145,800 (36% of £405,000) in tax rather than £162,000 at full rate (40% of £405,000) – a saving of £16,200.

2. When previous gifts change the outcome

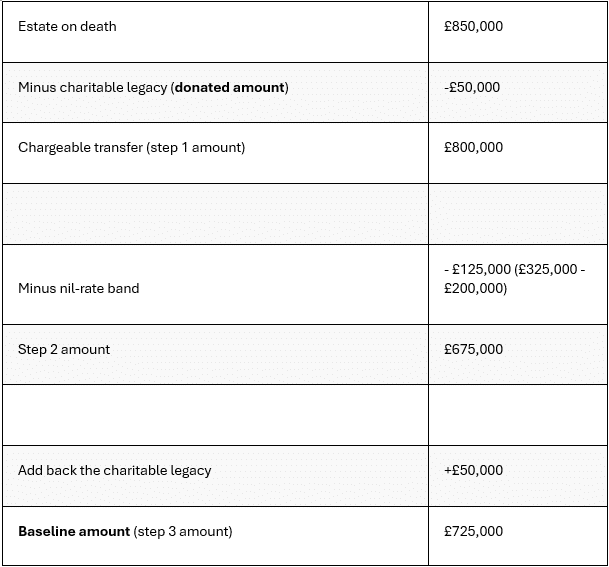

David died on 17 July 2024 leaving an estate valued at £850,000 after liabilities. He left a legacy of £50,000 to Cancer Research UK. However, his earlier £200,000 gift to his daughter 4 years before he died reduces the available nil rate band, changing the calculation:

In this case, 10% of the baseline amount is £72,500, so the £50,000 gift falls short, and the estate does not qualify for the reduced rate.

However, the beneficiaries of the estate could correct this by increasing the charitable gift through executing a deed of variation, so that the 10% test is met.

In this example, increasing the gift by £22,500 would still leave the beneficiaries better off due to the tax on the estate reducing by £35,100.

Summary

Estate planning can be complex, and some estates will benefit more than others by leaving a gift to charity in a will. Advice is clearly critical to ensure the requirements are met and avoid the need for post-death variations.

Regularly updating and reviewing a will is a vital part of good financial housekeeping and should be a routine topic with clients. As interest in IHT planning grows, understanding how charitable giving can reduce tax rates will become increasingly more valuable.

Main image: alvaro-serrano-hjwKMkehBco-unsplash