Adam Higgs, head of Research at Protection Guru examines the free cover periods that com with m most insurance policies – when and how they apply and their limitations.

Once a protection need has been established, getting cover in force so that the client is protected is extremely important. Where the need is family protection that need might be immediate. Where cover is to protect a liability such as a mortgage then the cover should start when the clients’ liability starts.

For most cases where there are no health or other disclosures that require underwriting, this will usually be relatively simple. Where there are disclosures leading to underwriting this might be more difficult. Fortunately for life cover all insurers offer an element of free cover that can be put in place before a plan is put in force.

The free cover offered fall into two categories:

- Free cover during underwriting – provides a level of cover whilst a case is being underwritten.

- Free cover during property purchase – provides cover to mortgage clients from the date their liability starts (the exchange of contracts) until the start of the policy, which is usually upon completion.

As with most things there are significant differences in how insurers offer these types of cover. As free cover during underwriting is provided before the case has been assessed it will usually have more restrictions than the cover provided during property purchase where the case has been underwritten and terms have been offered.

Perhaps most important is the event in which it will pay out. Canada Life, Legal & General, LV= and Scottish Widows all restrict payment to accidental death only for free cover during underwriting. This means that sudden death due to disease or illness, such as a heart attack, would not be covered. On the other hand no insurer applies this restriction to free cover during mortgage completion.

In terms of exclusions, most insurers will apply a suicide exclusion to cover with many also applying a hazardous pursuits exclusions. Some insurers may only offer such cover to clients under a certain age which ranges from 49 up to the age limits within the plan itself. Where paraplanners a forming recommendations for older clients it is worth checking the chosen provider for this.

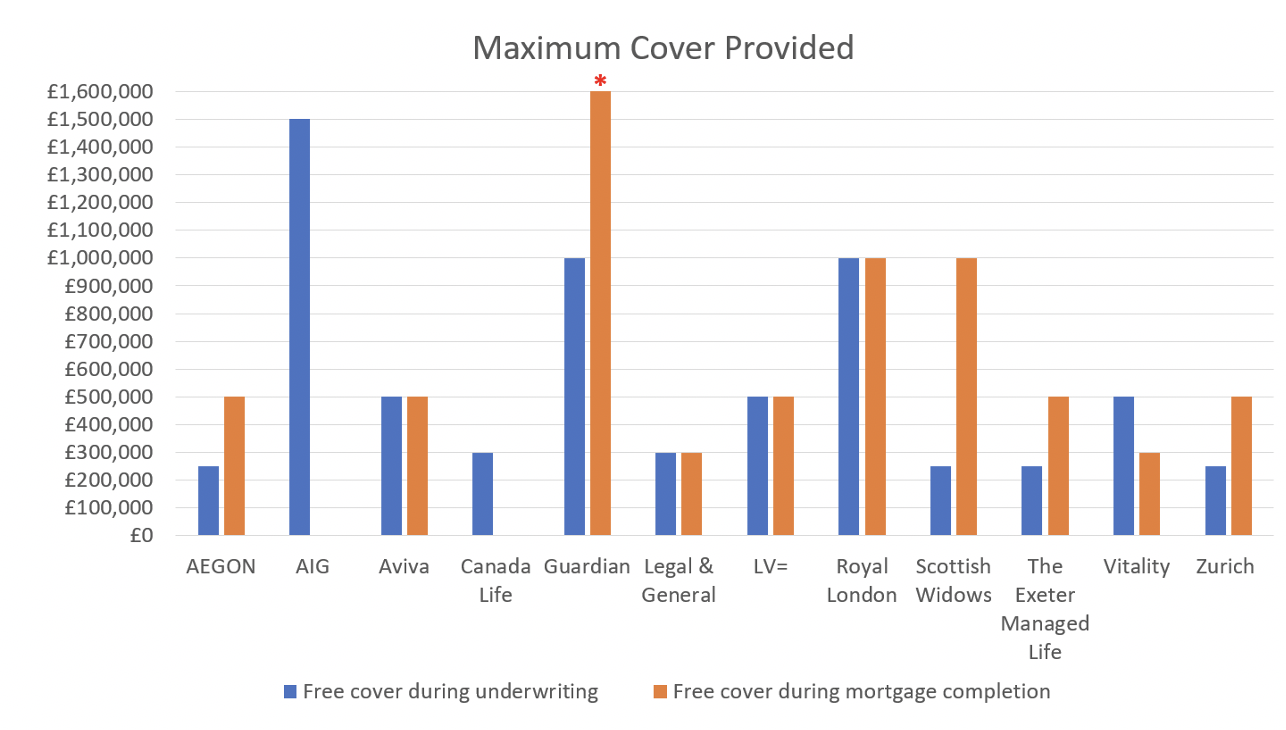

For most clients the maximum sum assured that would be covered would not make an impact as these are generally relatively high. Where a recommendation is being made to a high net worth client however, and a large sum assured is required it is worth understanding the maximum the client will be covered for before the plan is in force.

*Guardian have no limit to the sum assured on free cover during mortgage completion.

Due to underwriting or trusts it may not always be possible to put a plan in force straight away. If the worst happened during this period, then the clients’ family could be exposed to serious financial detriment. Free cover provides an element of cover in such situations which could help mitigate at least some of the risks and it is well worth highlighting these features to clients when suitable.

A longer version of this article and others is available on the Protection Guru website.