The market narrative has moved on from stagflation, but what comes next? The Fidelity Solutions & Multi Asset team takes a view.

Stagflation is the narrative that has dominated economies and markets for the last few months. However, Fidelity’s Multi Asset team believes that is about to change as attention moves from inflation to growth. But what will replace it? We estimate that there is a 40% chance of a soft landing, a 35% chance of a hard landing, a 20% chance of continued stagflation and a 5% chance of reflation.

We have based these estimates on three key factors that we are monitoring: hard data in the form of our new activity indicators, energy disruptions, and market implied signals.

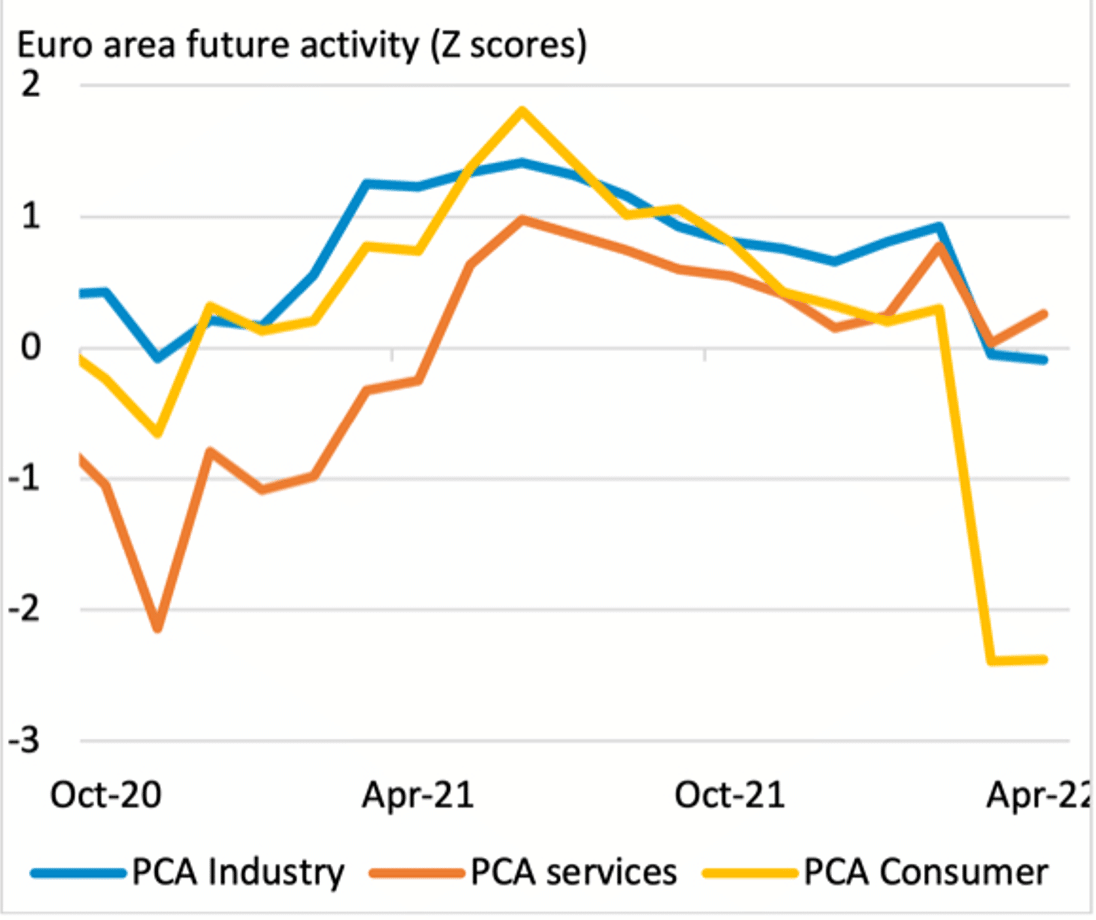

2. Our activity indicators reveal European consumer stress

Our new US and Euro area activity indicators, which include a range of data points, show a recent slowdown in future activity expectations for both the US and Europe, evidently related to the start of the war in Ukraine in late February. The euro area indicator is now around half a standard deviation below its long-run mean, compared to one standard deviation below during the 2011-2012 recession.

Chart 1: Consumers weigh on expected activity in Europe

Source: Fidelity International, May 2022.

In Europe, the stress is coming from consumer sentiment, while services sector expectations remain resilient for now. With global consumers squeezed by the cost-of-living crisis caused by as real incomes contracting (with the notable exceptions of China and Japan), interest rates rising and overall financial conditions tightening, risks to activity and growth from here are clearly skewed to the downside. The data points to a hard landing in the Euro area but is less conclusive about the US’s future.

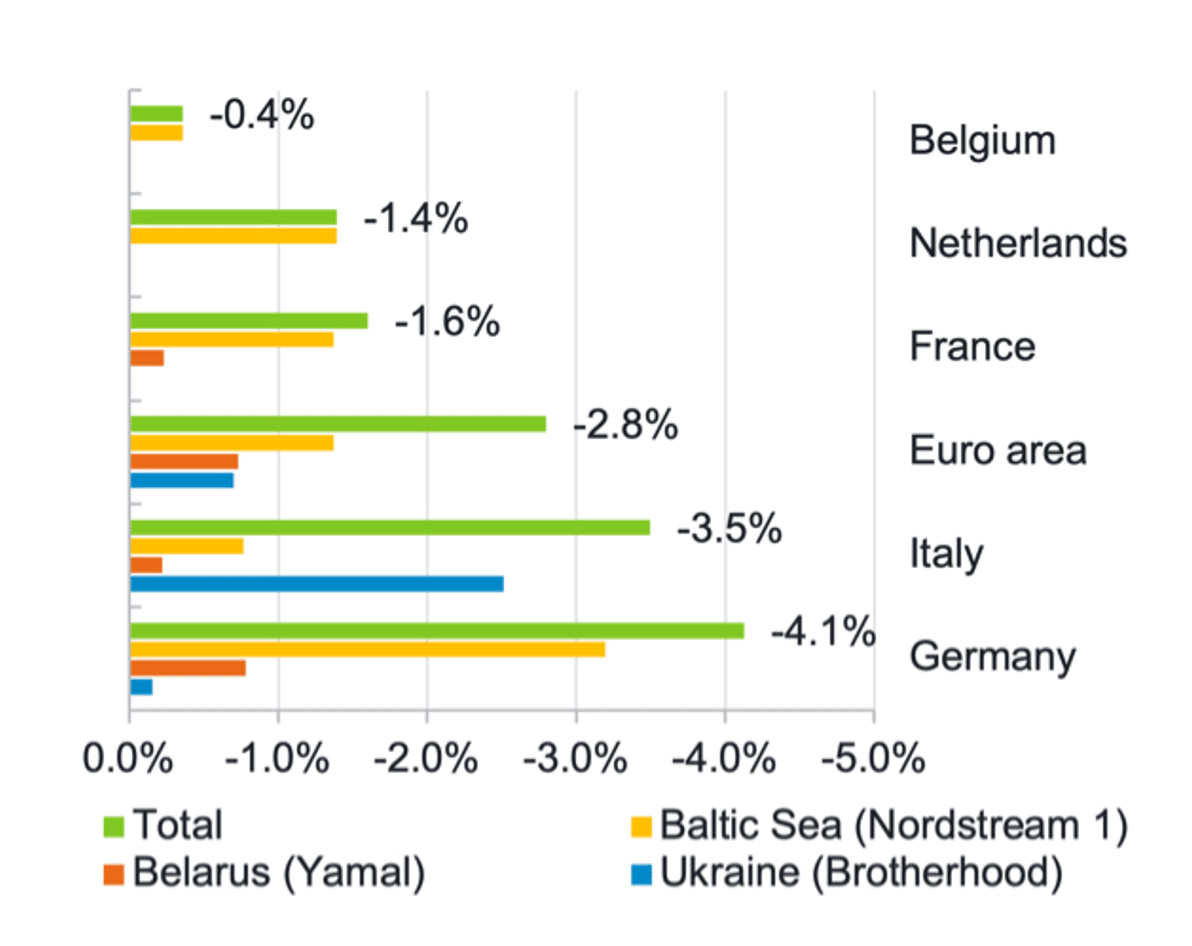

2. Europe gas inventories will indicate industrial sector damage

Energy markets are the primary macroeconomic channel via which the fallout from the Russia-Ukraine is transmitting around the globe. The likelihood of recession, especially in Europe, depends in large part on developments in energy markets. Europe is highly dependent on Russian gas, which represents around 40% of its domestic consumption. Energy prices have spiked since the war began, as countries across the globe put embargoes and sanctions on Russian commodities. However, Europe continues to import Russian energy.

Disruption to gas flows has already been significant, affecting both the households and the industrial sector, feeding into the economy in the form of higher inflation and weaker growth. Gas flows into Europe from Russia began declining in September 2021. This year, flows are almost 30% lower than last year.

Chart 2: Europe will suffer if Russia gas supply is further disrupted

Impact on GDP of supply disruption according to pipelines. Source: Fidelity International, May 2022.

The reduced supply is yet to meaningfully dent gas inventories in the EU, which are already above the equivalent 2021 level and are quickly converging towards the 5-year average. However, given the current disruption, we believe this can be attributed to weaker demand due to warmer weather and a reduction in industrial usage due to higher prices. As such, gas inventories are a key indicator to watch – if supply remains constrained, they will give an indication of the damage being done to Europe’s industrial sector.

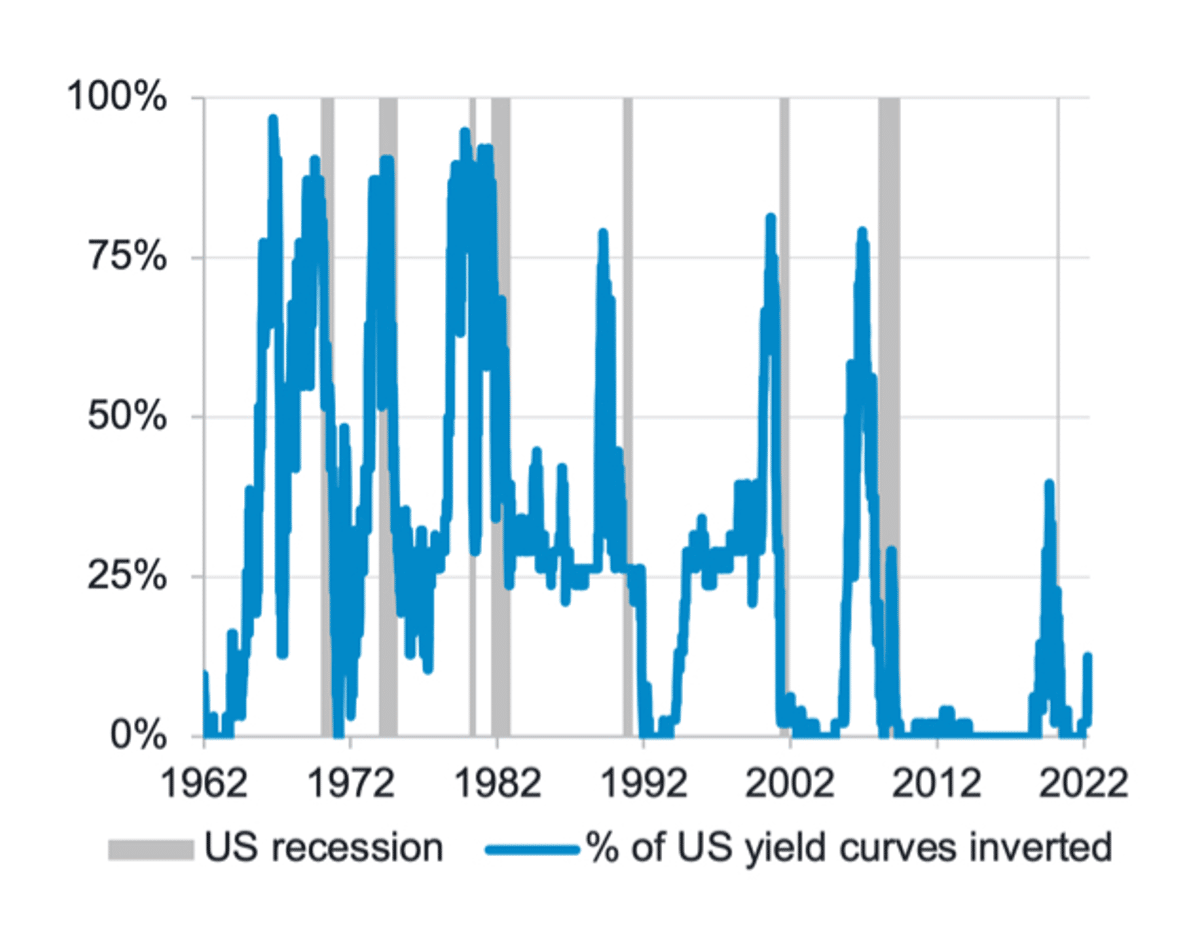

3. Yield curves not pointing to recession, but more FCI tightening needed

The inversion of part of the US yield curve garnered much attention earlier this year. However, not all parts of the curve inverted and some are sending very different signals. When looking at the entire nominal, real and risk-adjusted yield curves, the number that are inverted is only 13%, not yet a cause for concern.

Chart 3: No warnings lights flashing from aggregated yield curves

Combination of nominal, real and risk neutral curves. Source: Fidelity International, May 2022.

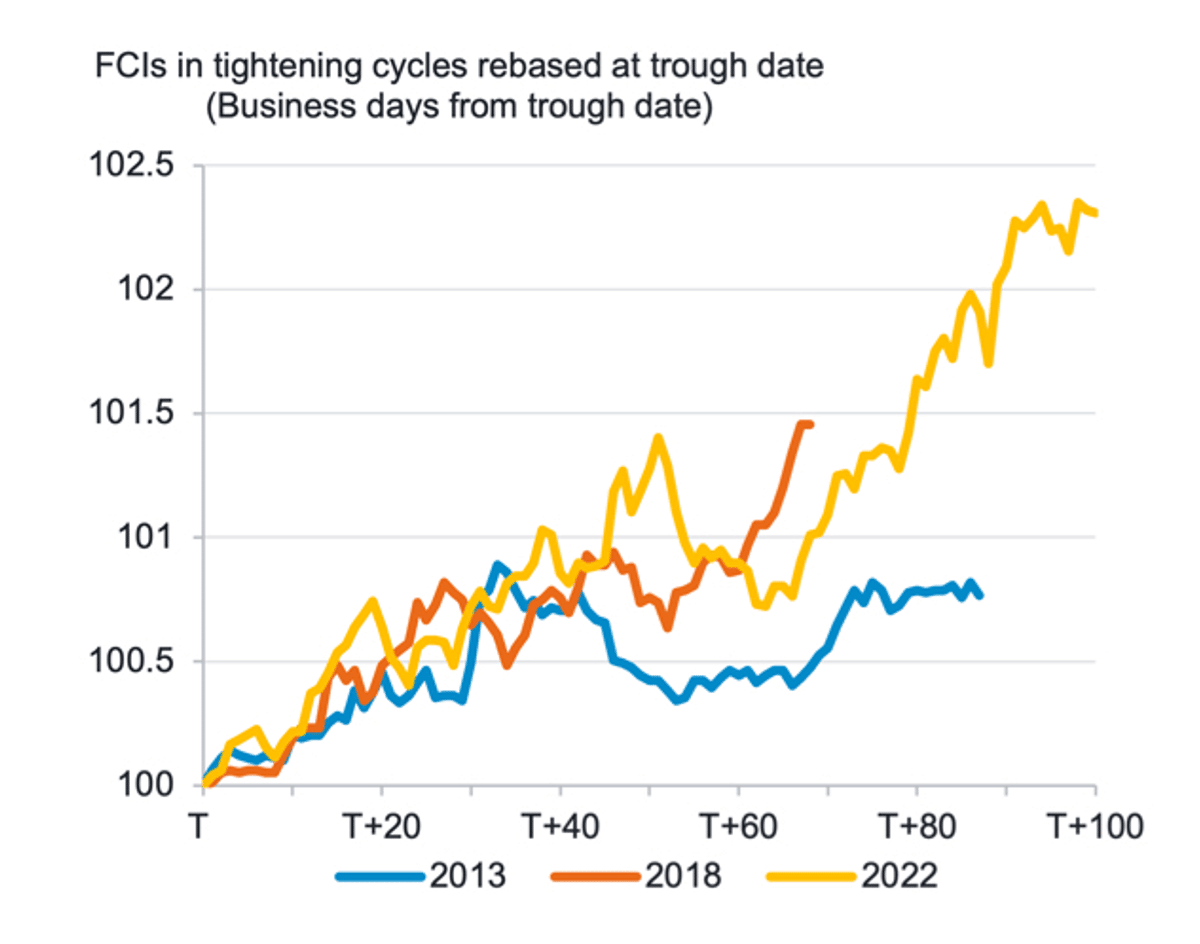

Another market implied signal is financial conditions. In the US, they have tightened by more than 200bps this year, already a larger and longer tightening cycle than those in 2013 or 2018. Given changes in the GS FCI are designed to correlated exactly to GDP growth, it is unsurprising that US growth estimates have fallen by around 180bps. The Fed is now actively targeting below trend GDP growth (approximately 1.9%) in order to bring inflation down to levels consistent with their GDP target.

Despite the material tightening so far this year, inflation is still stubbornly high and the labour market is strong. On balance, we think more tightening is necessary, implying growth estimates will need to fall further.

Chart 4: Already significant tightening, but more likely to come

Source: Bloomberg, Fidelity International, May 2022.

We also have a high conviction view that the system itself, due to substantially higher debt loads, cannot take positive real rates for any material length of time. We believe 0.5%-0.75% is likely to be the ceiling for the 5y5y forward real rate due to these systemic constraints.

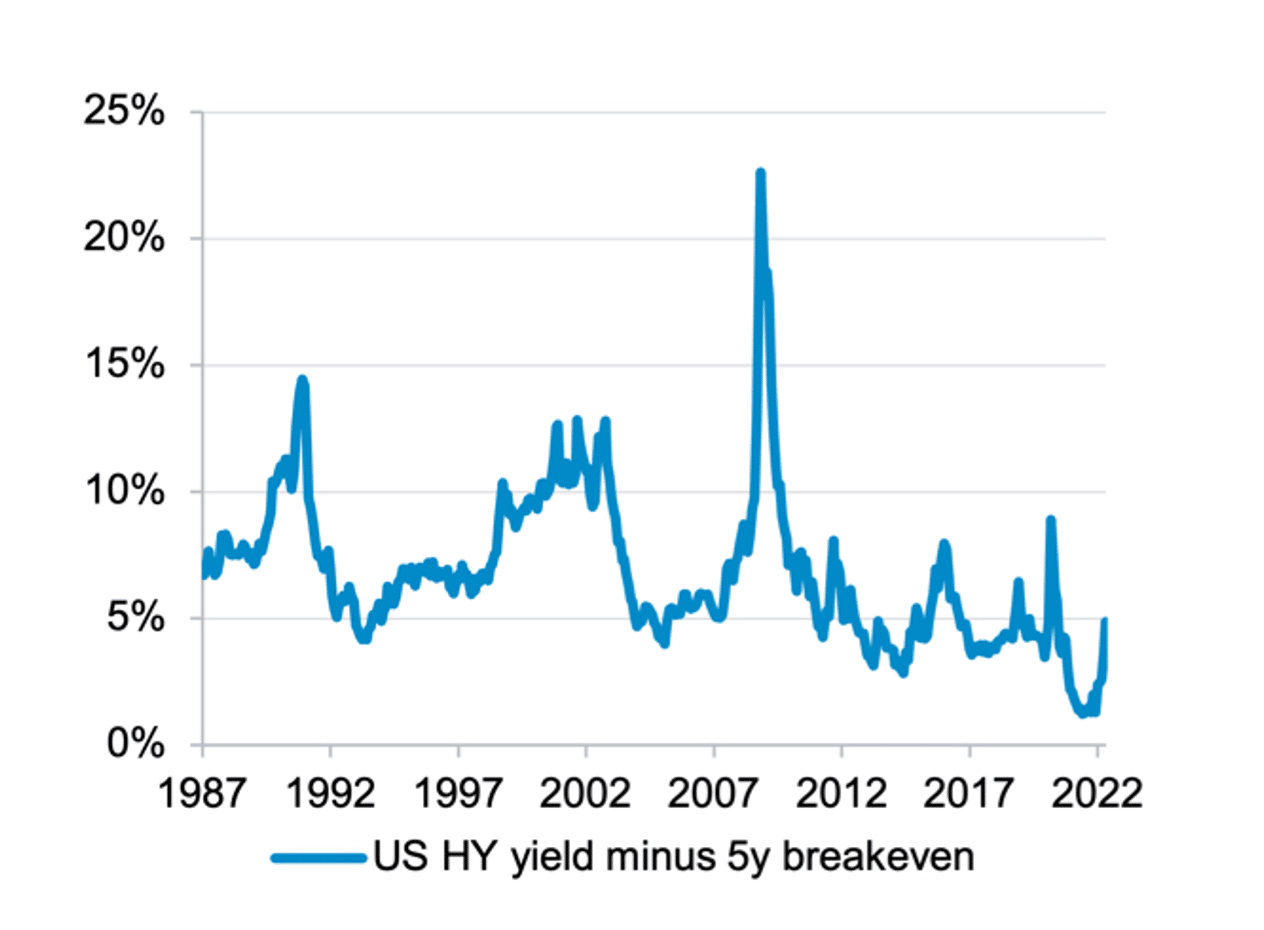

This implies that the primary driver of financial conditions tightening will switch from rates markets, which has led the tightening so far, to credit markets. High yield spreads have yet to meaningfully price in the risks to growth, while inflation-adjusted yields are still near all-time lows. We expect this to change.

Chart 5: Credit has more tightening work to do

Source: Bloomberg, Fidelity International, May 2022.

Macro research powering asset allocation

Fidelity’s Global Macro & Strategic Asset Allocation team contributes to Fidelity Multi Asset’s tactical asset allocation process by providing key macro inputs, working alongside the investment team to understand and respond to the macroeconomic drivers of markets.

Learn more about Fidelity Multi Asset

Important information

This information is for investment professionals only and should not be relied upon by private investors. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of investments in overseas markets. Investments in emerging markets may be more volatile than other more developed markets. Changes in currency exchange rates may affect the value of investments in overseas markets. The value of bonds is influenced by movements in interest rates and bond yields. If interest rates and so bond yields rise, bond prices tend to fall, and vice versa. The price of bonds with a longer lifetime until maturity is generally more sensitive to interest rate movements than those with a shorter lifetime to maturity. The risk of default is based on the issuers ability to make interest payments and to repay the loan at maturity. Default risk may therefore vary between government issuers as well as between different corporate issuers. Due to the greater possibility of default, an investment in a corporate bond is generally less secure than an investment in government bonds. Reference to specific securities should not be interpreted as a recommendation to buy or sell these securities and is only included for illustration purposes. Issued by Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM0622/370923/SSO/NA