Nutshell Growth manager Mark Ellis deliver something different in a very busy sector, says Juliet Schooling Latter, research director at FundCalibre.

It’s never easy to launch a differentiated product into a proliferated market like global equities – but to do so in the aftermath of one of the fastest stock market crashes in history is especially challenging.

However, this is precisely what Nutshell Growth manager Mark Ellis did back in 2020, as the pressures of Covid had a vice-like grip on the global economy. The fund is designed to tap into his view that the traditional method of stockpicking is outdated, such as analyst reports which quickly become dated and include a number of biases.

Mark, who is both chief executive and chief investment officer at Nutshell, effectively starts with a blank piece of paper every two weeks and tries to build a portfolio that can consistently outperform by targeting factors like high returns on equity, high profit margins and momentum.

The process starts with a data extraction from 10,000 publicly-listed companies. Stocks must meet minimum hurdles for return on invested capital, profit margin and market cap. This reduces the universe to 600 stocks. The fund then scores for 30 financial and 20 non-financial metrics using its in-house factor-based model.

The result is a high-conviction portfolio of around 30 names which is unashamedly reactive. Mark and the team make around fivetrades a day, with the aim to make alpha from small trades of, say, 25 basis points. “It’s like one live relative value trade, comparing stocks across the globe to each other and their own history” he says.

Covid was a baptism of fire for the portfolio; Mark says the process is very reliant on fundamental data, which was challenging in this uncertain environment. He says the team had to manually digest the data and take a view on the mean reversion of those fundamentals in those uncertain times. What followed was an aggressive growth bear market in 2022, which also posed challenges.

He says: “We launched in a challenging period but my mantra is you never lose – you either win or learn. We’ve adapted and grown as we move into an environment where volatility and dispersion provide opportunities for us.”

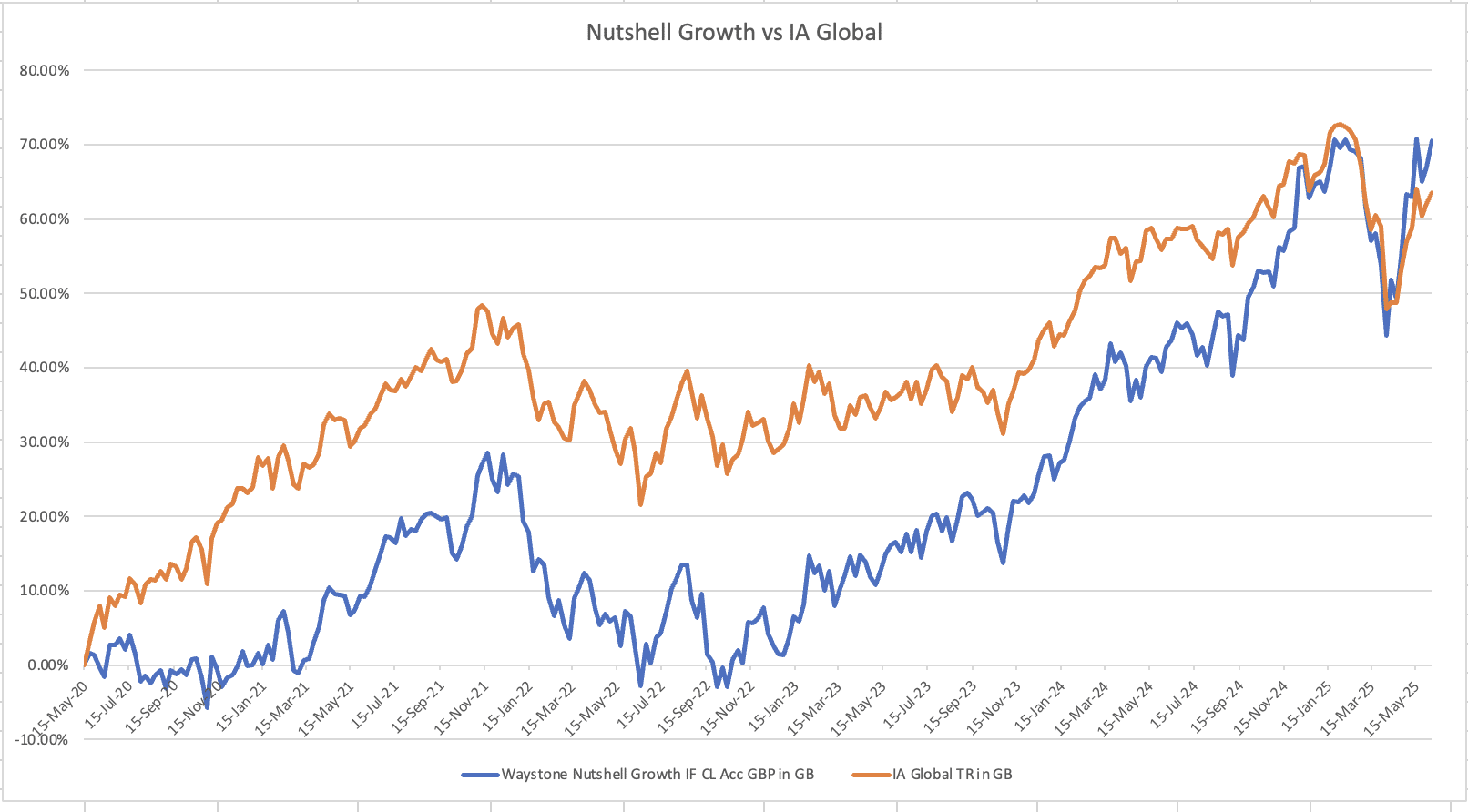

By contrast, the current environment should see the fund continue the strong performance seen in 2023 and 2024 (it has risen by more than 25% in both years)*. Mark says he tries to recalibrate the portfolio when volatility is high as dispersion creates fear, which opens up the door for greater alpha generation.

“Lots of alpha from small trades”

To be clear, while the fund does do a lot of trading, roughly three quarters of the names held are largely unchanged. The allocations to these companies fluctuate as pricing opportunities appear.

Take Swedish firm Fortnox as an example – it is a flexible cloud-based business solutions platform for accountancy, bookkeeping, payroll and invoicing. Mark says it is one of the highest-quality stocks on the planet when you consider the stability/growth of earnings and return on invested capital. However, there has been a lot of takeover noise around the stock. The fund took advantage of the noise to sell a small position (0.25%) on May 30 (Friday), only to add the same position back in on Monday (June 2) by which point the stock had fallen 3.5%. It remains a top 10 holding in the portfolio.

One of the edges the team feel they have is that they go like-for-like across the globe to find these exceptional companies without being pigeonholed to one investment style.

By contrast to Fortnox, which was on a PE of around 60x, the team also held the likes of US wire producer Encore Wire. It was added to the portfolio on a 3x PE before being bought out on a 15x multiple in 2024.

“You can overpay for a stock by doing nothing”

Mark says they are constantly in and out of the likes of NVIDIA and Arista Networks – the high beta names who move around a lot – creating opportunities. Another way to look at it is to consider the top five contributors to the portfolio since launch (Arista Networks, Autozone, Novo Nordisk, Fortinet and Microsoft). They are mainstays in the portfolio because the quality and growth factors are stable (Novo Nordisk dropped out last year when it got too expensive in Mark’s view before being added back when the price fell).

“Unlike our peers who do nothing, we trade positions as their expected returns change to pick up alpha opportunities. The idea of ‘don’t overpay and do nothing’ to my mind is a contradiction – by doing nothing and holding a stock you are overpaying for it,” Mark adds.

With volatility on the rise in 2025, the fund has been making changes, notably increasing its allocation to US equities from 54% to almost 70%; meanwhile technology stocks now represent over half of the underlying holdings. Mark says earnings season has been compelling for most of the Magnificent Seven, with the team adding to NVIDIA off the back of it.

Mark argues the S&P 500 is not expensive relative to history, given it was previously dominated by low-quality growth companies with noisy earnings, such as financials and resources. By contrast, the Magnificent Seven represent some of the best quality companies on the planet.

He says: “They have earnings growth year-after-year, stability of earnings, profit margins and returns on invested capital. They also have unprecedented access to billions of customers.”

This is a different fund in a very busy sector. Mark has a trading background and performance indicates he has used it to good effect since the product was launched by building a portfolio with higher-quality characteristics at a cheaper price. You only have to look under the bonnet of the 27% return in 2024 – with 16 stocks contributing 1% or more to the portfolio. It is a solid consideration for exposure to global equities.

*Source: FE Analytics

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. Juliet’s views are her own and do not constitute financial advice.

Main image: jacqueline-o-gara-cn4aQjHA_Nw-unsplash