Junichi Takayama, Japan Investment Director, Amova Asset Management (previously Nikko AM), looks at the changes within the equities market in Japan following the new Trump tariffs, the rising sectors and why Japan can be used as a strategic diversifier in the more volatile global landscape.

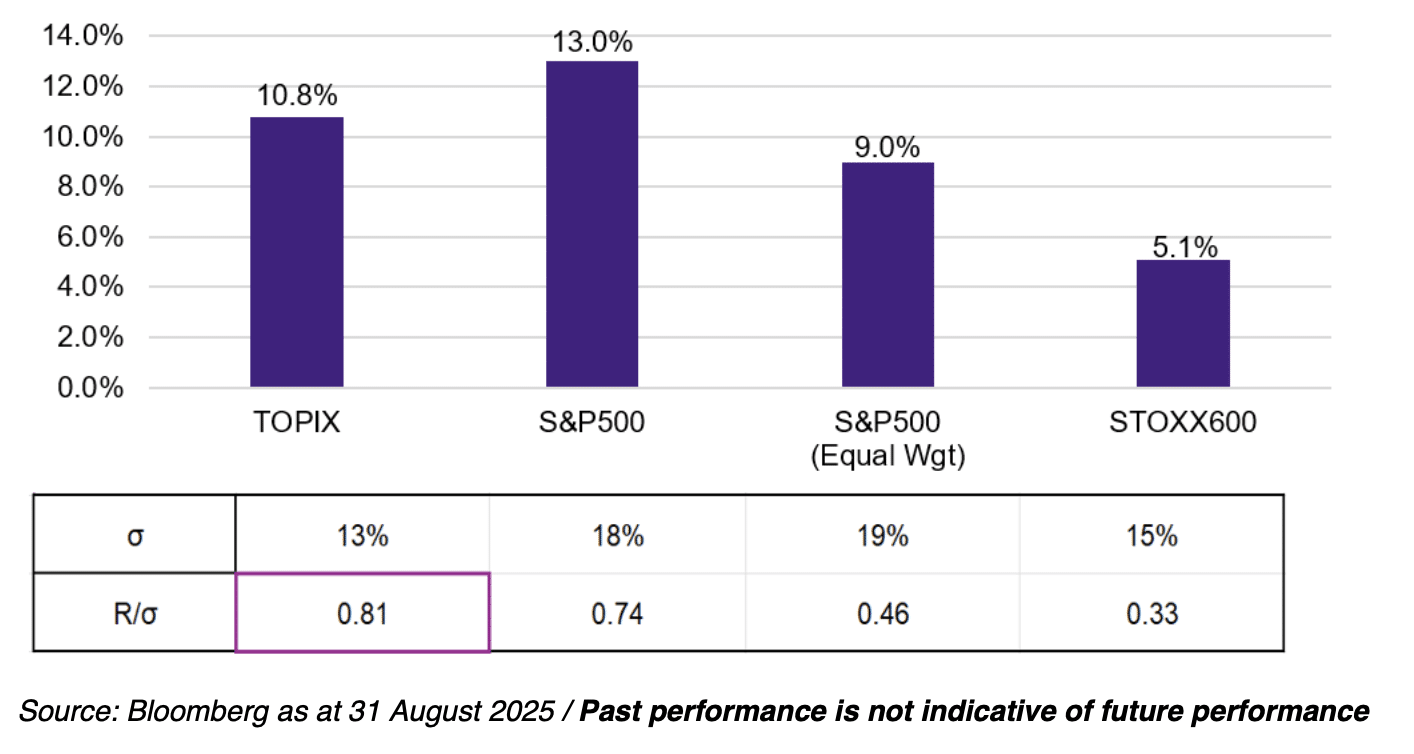

When we look back over the past five years, Japanese equity markets have done quite well, with the TOPIX index rising 79% (or 10.8% annualised) since January 2020 through August 2025. This has been a dynamic period for equities, with no shortage of catalysts driving market sentiment.

The major market events during the period include the pandemic lockdowns, followed by the reopening trades, Warren Buffett’s significant increase in stakes in Japan’s largest trading houses, Tokyo Stock Exchange’s guidance to call for companies to improve capital efficiency and, more recently, the trade tensions initiated under US President Donald Trump’s administration.

Needless to say, the Magnificent 7 (Mag 7) stocks have done extremely well, delivering an exceptional 583% (or 40.4% annualised)* return during this period. The Mag 7’s dominance and their growing concentration coupled with the US concentration in the global equity market clearly raises concerns of diversification risks.

The broad market TOPIX Index led major markets in risk-adjusted returns over the past five years. While the S&P 500 outperformed the TOPIX, driven by Mag 7, it is worth noting that TOPIX outperformed S&P 500 (equal weighted) and STOXX 600 with a lower market volatility

Chart: Annualised index return since January 2020

Sector shifts reveal market evolution

Since “Liberation Day” in April, investors in the Japanese equity market have shifted away from exporters’ stocks, most notably auto and auto parts sectors. Eight rounds of negotiations between the US and Japan led to a trade agreement on 23 July, which alleviated market uncertainty. This resulted in exporter stocks gaining ground, driving the market higher.

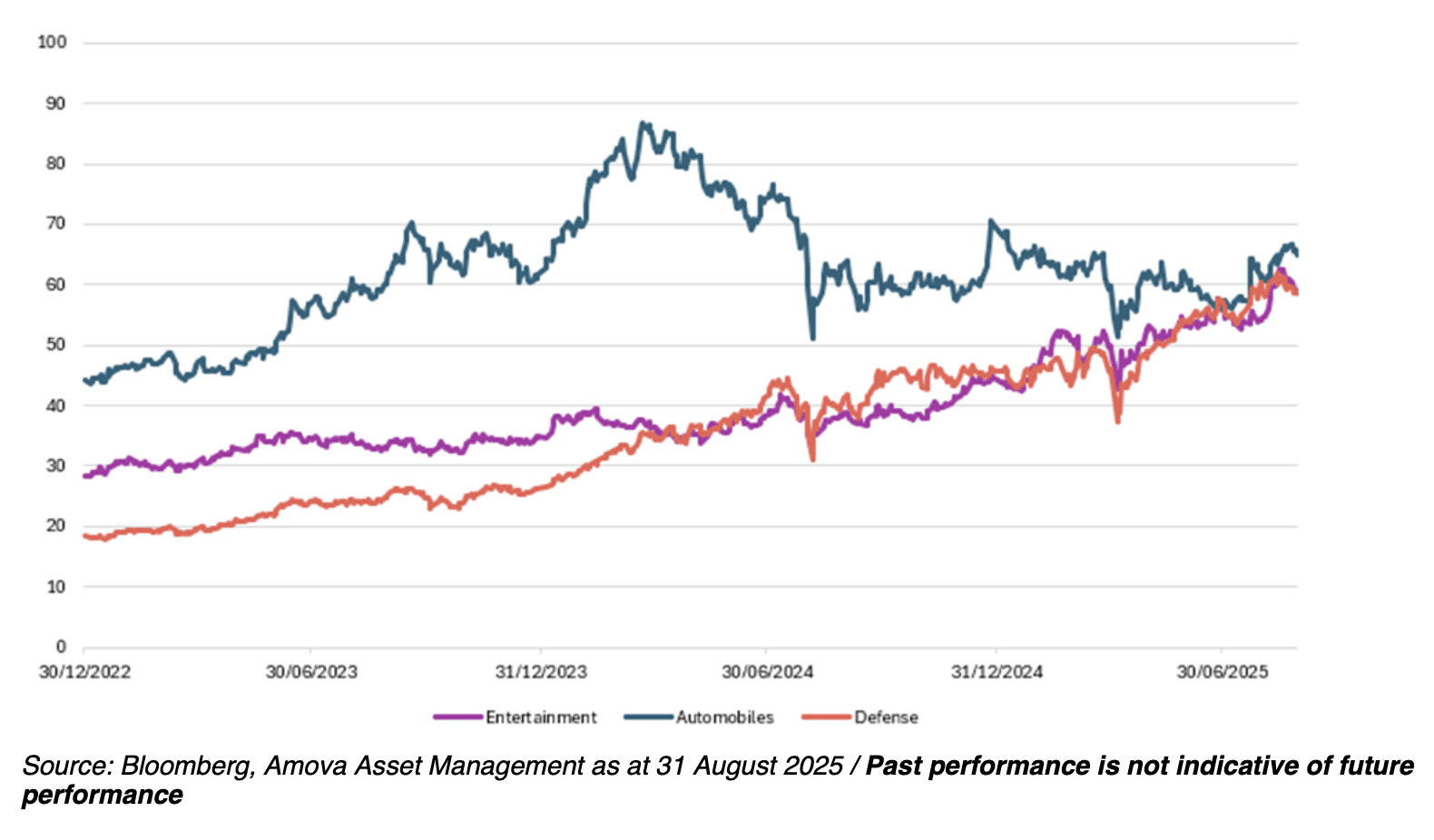

If we were to zoom out, data shows that some of the tariff-proof sectors have been consistently rising over the past few years. In one measure, defence and entertainment sectors have each caught up with the auto sector in terms of their aggregate market capitalisation (see chart and table below).

Chart: Aggregate market cap trend in three segments in JPY trillions (entertainment/auto/defence)

Table:

Companies used for above chart – defence, entertainment, and automobile sectors

Defence and entertainment sectors are not only seen as “tariff-proof” but also have secular growth stories for equity investors. Japan’s defence spending is growing at an unprecedented pace amid the rising geopolitical tensions in East Asia. Since fiscal year 2023, the government has been in the process of doubling the national defines budget to 2% of GDP, and furthermore, the 2% target could be further boosted over the medium term.

In addition, nearly a decade after the new principles on transfer of defence equipment and technology were announced by the Japanese government in 2014, which effectively relaxed exports of defence equipment, a joint initiative between Japan, UK and Italy to develop a next generation fighter jet was announced in 2022. More recently, on 5 August 2025, the Australian government announced that it selected frigate developed by Mitsubishi Heavy Industries through a competitive tender process. The defence industry in Japan is well positioned to not only supply within the growing market in Japan but also to increase exports of equipment to key national security allies.

Meanwhile, the entertainment industry is also gaining attention for its potential to further capitalise on its strengths—particularly its compelling content—for export to international markets. According to METI (Ministry of Economy, Trade and Industry), exports of content originated from Japan has tripled over the past ten years to JPY 5.8 trillion (approximately USD 39 billion), even surpassing exports of the semiconductor and steel industries in 2023, and now trailing behind only the automobile industry (including auto-parts and motorcycles). The entertainment industry includes gaming, animation, manga, movies/videos and music.

The market environment for the content business has undergone a noticeable shift globally over the past several years, with the increasing use of digital/streaming services. According to Visual Capitalist’s recent ranking of the world’s top media franchises by all-time revenue, Japanese franchises led the rankings for character-based media revenues, with Pokémon and Hello Kitty securing the top two positions (and five of the top 10 positions overall).

Table: The world’s top media franchises by all-time revenue

While corporate governance reforms and the automotive sector remain central to global investor discussions, Japan’s defence and entertainment industries are gaining traction, driven by improving fundamentals and rising investor expectations. As sector compositions continue to shift and market dynamics evolve, we believe Japan warrants a renewed look from investors – particularly in light of global economic headwinds and the growing imperative for portfolio diversification.

Main image: zhaoli-jin-e4I2ktXz5cA-unsplash