For this month’s three-year track record article Juliet Schooling Latter, research director at FundCalibre, talks to the manages of the Invesco Tactical Bond fund.

After what has been an incredibly busy and opportunistic couple of years for fixed income, I would say the current state of the asset class is dictated by two words – volatility and balance. There is no doubt we are now in a volatile macroeconomic environment and the best way to counter that is through balance.

We’ve seen central banks desperate to find a balance between stemming the rise of inflation but without cutting rates too aggressively. A good example of this was the US Federal Reserve’s recent – but protracted – 50 basis point rate cut, which reflected a shift in focus from inflation to labour market risks (I’ll discuss this a bit further on).

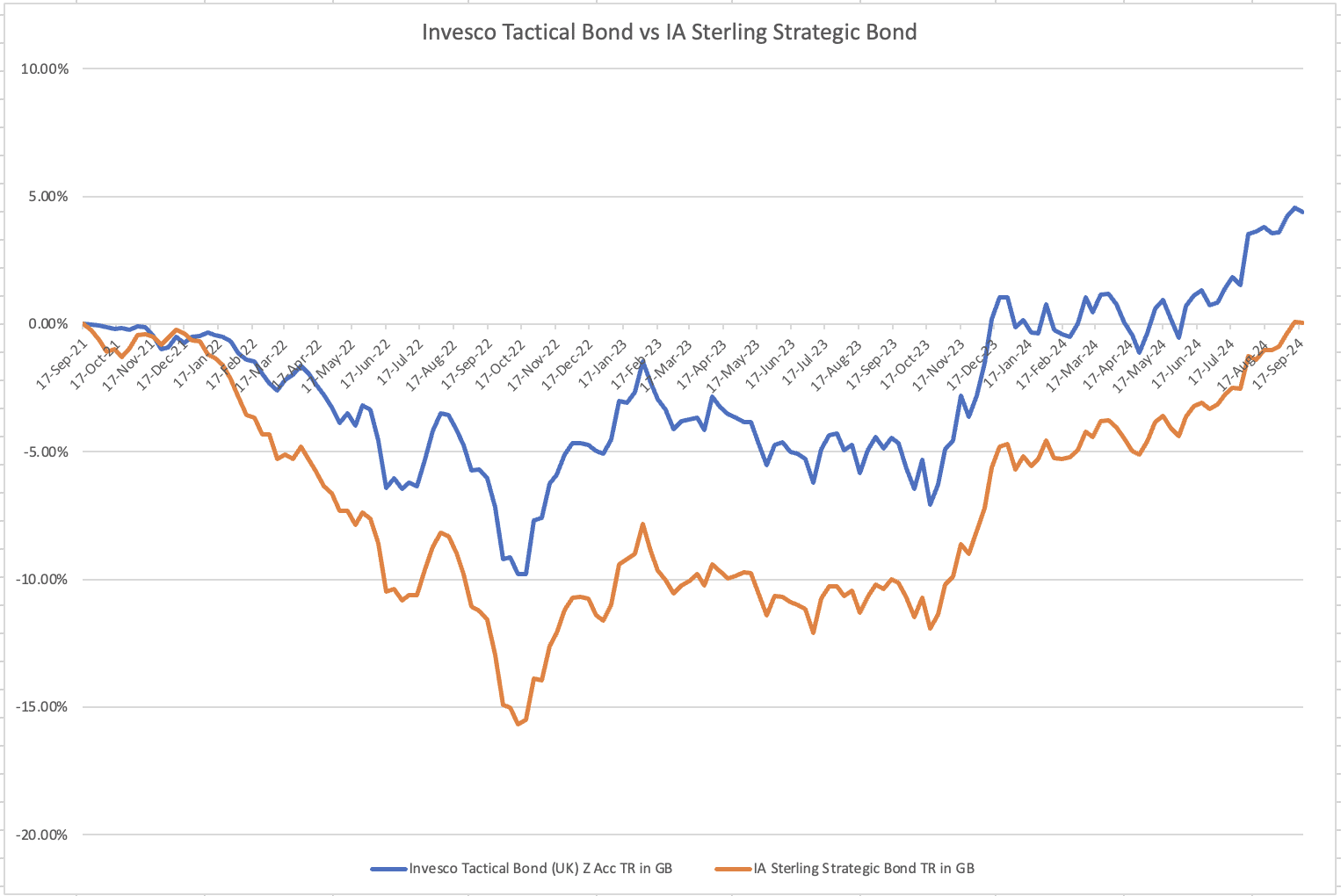

This all comes after the impact of rate hikes on fixed income in 2022 and 2023. A lot of headlines have been written about the risk-free rates available to investors in that time. The reality is that after the big jump in 2022, the yield has remained around the 4-5% mark for US Treasuries and UK Gilts. Credit has actually outperformed government bonds quite comprehensively. Take 2023 for example – gilts and treasuries returned 3.7% and 3.9% in total returns respectively; by contrast, £ IG Corporates (9.8%), € IG Corporates (12%) and USD Cocos (7.5%) have produced far stronger returns*.

But those aforementioned rate cuts hint at a macro environment that is shifting from high inflation to the impact of greater downside risks. The challenge is that there is no clarity on the direction from here. On one hand we still have a US yield curve inversion indicating a possible recession – despite ongoing resilience; on the other, a win for Donald Trump in November’s election could signal a more inflationary environment, which brings rate hikes back into play.

Now is definitely a time for flexibility – and that is what the Invesco Tactical Bond fund brings to the table. It is the least constrained fund in the asset manager’s fixed income suite by investing across the entire fixed income market (credits and duration). The fund has no industry sector or geographic constraints, and the investment strategy focuses on conviction, active management, and total return.

Managed by the experienced duo of Stuart Edwards and Julien Eberhardt – and backed by the strong analyst resource at Invesco – the process starts by analysing key factors that influence the government and corporate bond markets, such as inflation, growth, central bank policy, and political cycles. In the second stage, the global asset allocation group meets to discuss the macro environment and valuations across asset classes – although this group does not make decisions for Stuart and Julien, it is a forum for discussion.

Credit analysts then provide detailed analysis of corporate issuers and insights into relative value. In the fourth stage, once investment ideas have been considered, the managers decide whether to add to or change the portfolio based on the balance of risk and reward. The final stage is the continual monitoring of security prices and overall exposures. The portfolio currently has 232 holdings; turnover can vary but has been in the 25-30% range in the past year.

You only have to look back at the recent history of the fund to see these shifts in positions, with the liquidity bucket (cash, bonds maturing within a year, and governments) accounting for as little as 17.7% of the portfolio in December 2020 (vs. 41.9% in June 2024), while the credit allocation has been as high as 57.1% in 2021 (it is currently 34.3% of the portfolio)**.

De-risking and preference for duration over credit

The past couple of years have seen the team de-risk the portfolio to a reasonable degree, a reflection of the strong run in credit versus duration assets. Crucially, the team believe risks are now more prevalent.

Product director Cathal Dowling says: “Inflation is now down to a level where central banks are comfortable cutting rates. Growth is alright, but there are clearly things to worry about and the fear is whether they become bigger or whether we continue on this soft landing approach. We think that approach is reasonable but there remain things to worry about in that backdrop.”

Although rate hikes have not had as big an impact on the US as expected, there have been reasons for this and, importantly, things are changing. For example, US household savings rose markedly during Covid – offsetting the initial effect of rate rises. However, excess savings started to turn negative in 2024***

The 30-year US mortgage rate also offset the impact, but we are now seeing the effective rate of interest on outstanding mortgages start to rise. Lower income consumers are also borrowing more, while job openings are also falling in the US.

Credit spreads are no longer looking particularly attractive, standing at 116 and 96 basis points for UK and US investment grade corporates respectively****. Meanwhile, high yield has greater risk, with companies starting to renegotiate at higher interest levels.

Although duration on the portfolio has fallen from around 8 to 5.4, it remains higher than it has been historically, reflecting the positive structural view, particularly for government bonds. The managers have actively traded around duration to take advantage of market volatility, rather than sticking to a long-duration view.

This fund provides investors with a truly differentiated approach to most strategic bond funds. It benefits from investing in a very wide opportunity set, and by taking the best ideas from across Invesco’s team, which has helped drive strong, long-term performance.

*Source: Invesco, Bloomberg, 31 August 2024. Indices are ICE BofA. Return data in currency of index or as stated.

**Source: Invesco, 30 June 2024

***Source: fund presentation, September 2024

****Source: Invesco, market yields and spreads, 31 August 2024

Past performance is not a reliable guide to future returns. You may not get back the amount originally invested, and tax rules can change over time. Juliet’s views are her own and do not constitute financial advice.

Main image: richard-r-schunemann-3QsFMZLm_KU-unsplash