Paraplanners looking to analyse fees and make them clear to clients can have a hard job on their hands, says Peter Stewart, senior strategic account manager & associate director, Waverton.

Understanding investment management’s total cost to client is becoming increasingly complex. With performance aggregators and comparators like Mabel, Morningstar, FE and Defaqto, patraplanners are faced with a myriad of options and considerations for client recommendations, however, these can be murky waters…

Net apples and gross oranges…

The use of performance aggregators and comparators often presents challenges in terms of clarity and consistency, with some showing performance gross of fees, some net of fees, and some net of all but transaction costs. Needless to say, the lack of standardised metrics can make it difficult for paraplanners to make like-for-like comparisons and to assess the true value and cost of different investment strategies.

The allure of headline fees…

Many MPS disrupters often emphasise their low MPS charges, sometimes as low as 10 bps. Whilst obviously attractive, we would argue that it’s essential for paraplanners to look beyond headline figures and consider all associated costs, including the additional layer of third-party fund fees and transaction costs.

The need for consistency

MPS and Multi-Asset Fund (MAF) factsheets, which should provide a clear breakdown of costs and performance, often lack consistency across providers. This inconsistency makes it difficult to compare options and communicate costs effectively to clients.

To make matters more complicated, disclosure requirements for MPS and MAFs are not the same, despite the overlap in use by advisers and clients. MAFs do not need to disclose transaction costs on factsheets. While we adhere to the industry standard in this regard, Waverton disclose total costs in our ‘Technical Notes’ documents. These are available on request.

Warts & All

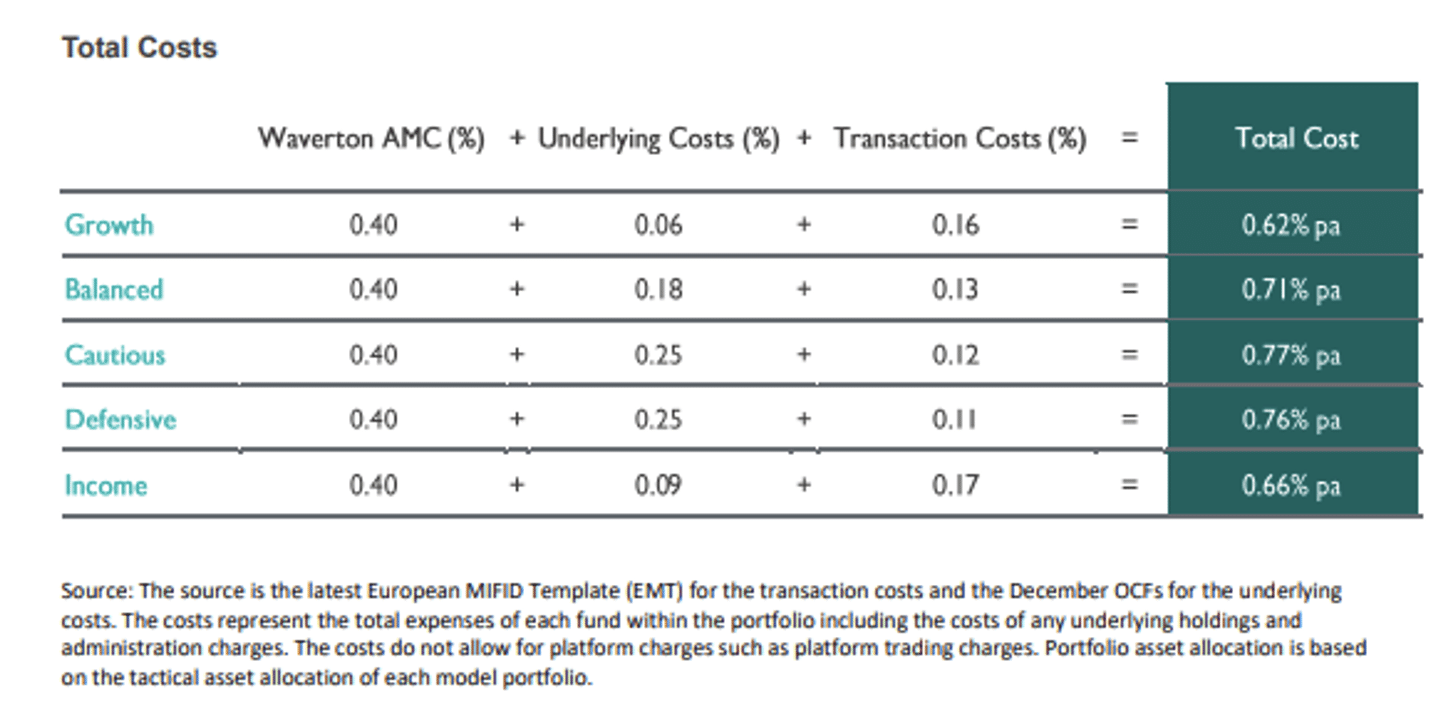

Waverton MPS factsheets disclose total costs, as broken down in the Figure 1. Waverton MAF factsheets disclose OCF, as per the industry standard.

When looking at a range of providers, Waverton’s 0.40% management charge may stand out, however, it is crucial to look at comparisons on a like-for-like basis. At Waverton we don’t charge a separate DFM fee. We also do not outsource our asset selection, using a predominantly direct approach to our underlying holdings rather than investing in third-party funds, which ensures an extremely competitive total cost for a truly active solution.

Figure 1: Waverton MPS total costs

Figure 2: Waverton Multi-Asset Funds total costs

For paraplanners, this means they only need to add their own advisory fee and the platform charge to the total client cost, simplifying the pricing structure and enhancing transparency.

Main image: patrycja-chociej-7fsBaAdaJFM-unsplash