As part of Schroders Q2 CIO Lens, Andy Howard, Global Head of Sustainable Investment, considers the overlap between investment opportunity and social importance in sustainability investing.

Sustainable investing is entering a new phase.

After years of rapid growth, a backlash began two to three years ago: political headwinds in the US, questions about greenwashing in Europe, and persistent concerns that incorporating sustainability considerations comes at a cost to returns.

Global sustainable fund flows turned negative in several quarters during 2024-25[1].

The critics have a point that demands an honest response. Not every social or environmental challenge translates into a compelling investment case.

For example, antimicrobial resistance costs the global economy an estimated $1 trillion to $3 trillion per decade, yet the investment returns available today to address it are low.

Air quality and weak pollution controls affect 6.7 billion people, but the investable market is small and slow-growing. Unfortunately, social urgency does not equate with investment opportunity.

A slowdown in policy action makes this distinction more important. The regulatory frameworks that convert social costs into financial signals – climate regulation, mandatory disclosure, environmental liability – have stalled or reversed in several major economies.

Without policy catalysts, many socially important themes remain financially uninvestable at the scale they need.

We expect the current stalling will prove temporary; growing environmental challenges and intensifying social tensions will inevitably demand a policy response.

However, for investors navigating this environment, clarity about where the financial case genuinely holds is both a prerequisite and an opportunity to look through headlines to the underlying fundamentals.

The good news is that the overlap between investment attractiveness and social importance is far larger than the current narrative suggests.

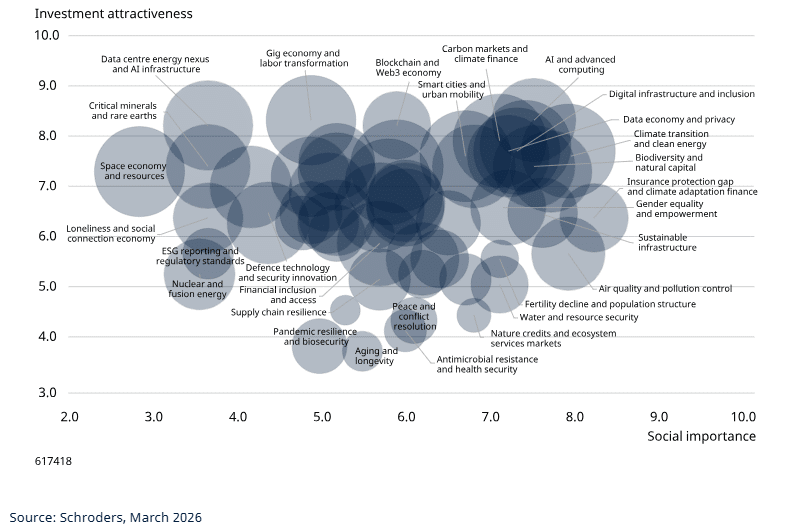

We have developed a dual-materiality framework that scores 55 global themes independently on two dimensions: investment attractiveness (based on market size, growth rate, expected returns, technology readiness and market maturity) and social importance (based on directly affected populations, the economic cost of inaction, alignment with Sustainable Development Goals, employment impact and investment scale required).

Each input measure is normalised to a 1-10 scale using a consistent methodology[2] so that themes can be compared on a like-for-like basis.

This is a blunt, top-down exercise which cannot replace thorough bottom-up analysis but demonstrates that trade-offs exist and provides a framework to identify the most attractive areas of focus.

Themes representing over 40% of the total market opportunity of the themes plotted score above the median on both dimensions, where strong financial returns and significant societal benefit coexist.

These include AI and advanced computing (the highest combined score in this dataset), the clean energy transition (a $1.8 trillion clean technology market growing at 13% annually), digital infrastructure and inclusion, biodiversity and natural capital, and carbon markets.

Collectively, these represent some of the deepest and fastest-growing capital pools in the global economy.

Other themes – collectively less than 15% of the total opportunities plotted – offer high social importance but below-median investment scores. These include water security and fertility decline.

These trends reflect unavoidable, intensifying structural trends for which their financial impacts are already being felt and will grow in the future, likely prompting the policy attention which could strengthen their financial impacts.

Across Schroders, our focus is on the themes and trends where we believe the investment consequences are strongest, now or in the future, and where we are best placed to develop insights, analysis and investment tools to support our clients. Examples include biodiversity and natural capital, as well as climate transition and clean energy.

We recognise that many investors prioritise social and environmental objectives, as well investment returns, and we have developed tools, solutions and investment strategies to support them, armed with an understanding of trade-offs and mitigants.

Our view of investment risk and opportunity underpins our firmwide commitment to sustainability. Structural trends in society, the environment, global economy, industries, and portfolios demand new perspectives and approaches.

By maintaining rigour over the investment opportunities sustainability-related themes present, we can support better investment decisions and help play a role in supporting policymakers to unlock change where it is needed.

To view Schroders full CIO Lens for Q2 2026: CIO Lens Q2 2026: Building diversified portfolios for uncertain times

[1] Source: Morningstar, “Global Sustainable Fund Flows: Q4 2025 in Review”, February 2026

[2] Log-transformed where data is heavily skewed, winsorised to prevent outlier distortion, and linearly scaled from 1 to 10

Main image: anika-huizinga-8_xZGSxk4to-unsplash